Whats Your New Year Resolution on Mt. Hood

Monday, January 10, 2022

Liz Warren

Displaying blog entries 291-300 of 1849

Many homeowners who plan to sell in 2022 may think the wise thing to do is to wait for the spring buying market since historically about 40 percent of home sales occur between April and July. However, this year’s expected to be much different than the norm. Here are five reasons to list your house now rather than waiting until the spring.

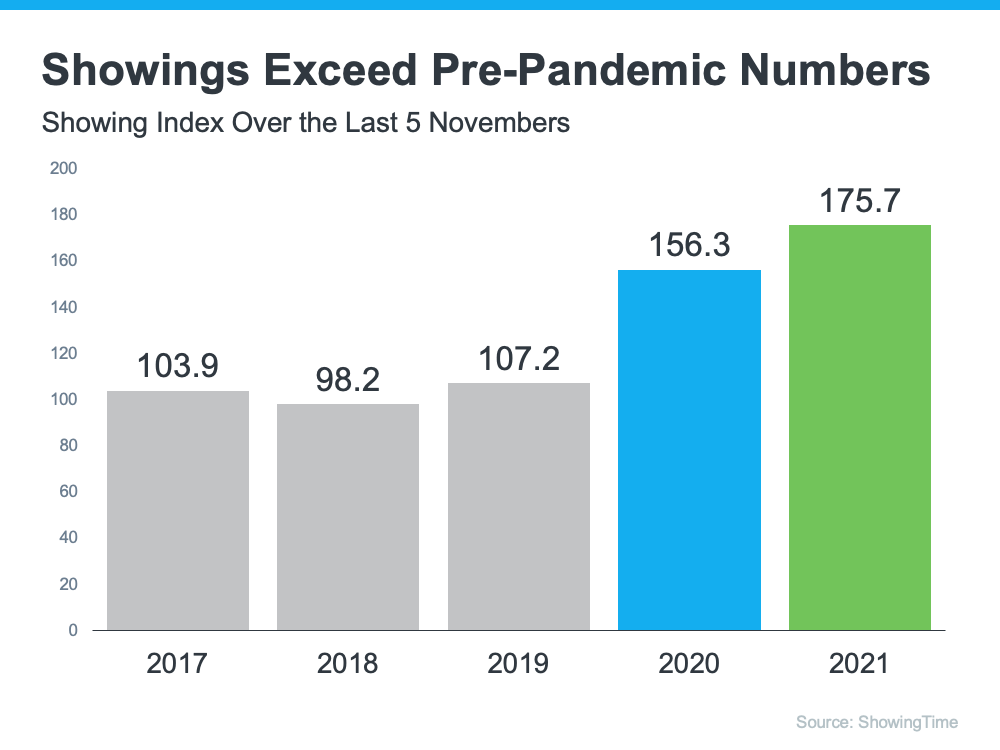

The ShowingTime Showing Index reports data from more than six million property showings scheduled across the country each month. In other words, it’s a gauge of how many buyers are out looking at homes at the current time.

The latest index, which covers November showings, reveals that buyers are still very active in the market. Comparing this November’s numbers to previous years, this graph shows that the index is higher than last year and much higher than the three years prior to the pandemic. Clearly, there’s an influx of buyers searching for your home.

Also, at this time of year, only those purchasers who are serious about buying a home will be in the market. You and your loved ones won’t be inconvenienced by casual searchers. Freddie Mac addresses this in a recent blog:

“The buyers who are willing to house hunt in a winter market, when there are fewer options, are typically more serious. Plus, year-end bonuses and overtime payouts give people more purchasing power.”

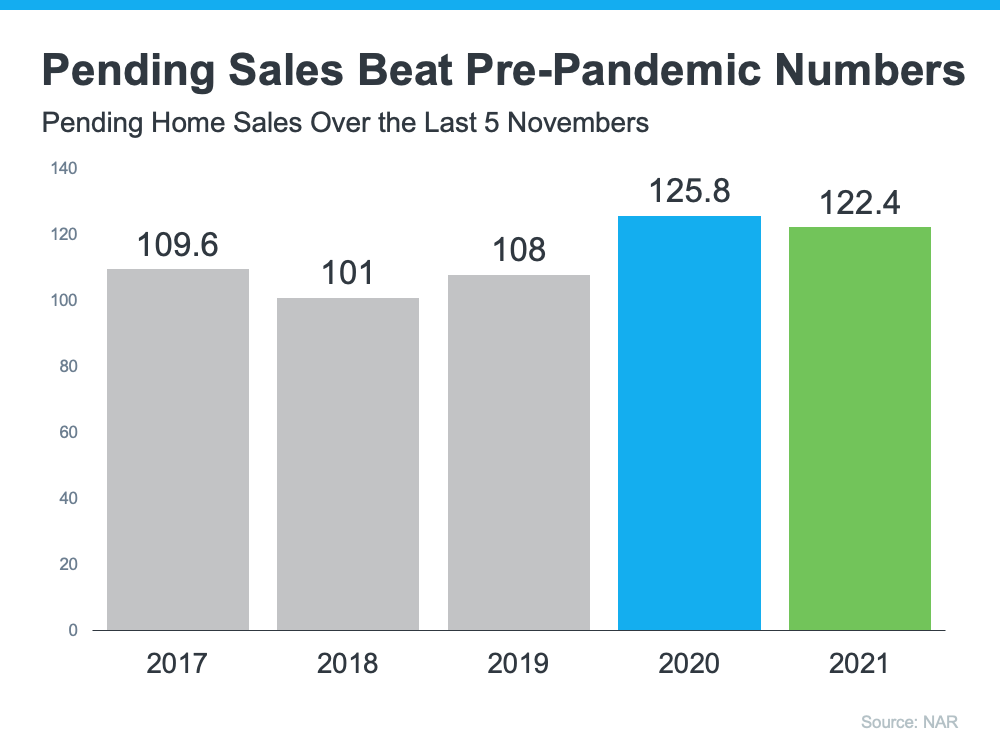

And that theory is proving to be true right now based on the number of buyers who have put a home under contract to purchase. The National Association of Realtors (NAR) publishes a monthly Pending Home Sales Index which measures housing contract activity. It’s based on signed real estate contracts for existing single-family homes, condos, and co-ops. The latest index shows:

“…housing demand continues to be high. . . . Homes placed on the market for sale go from ‘listed status’ to ‘under contract’ in approximately 18 days.”

Comparing the index to previous Novembers, while it’s slightly below November 2020 (when sales were pushed to later in the year because of the pandemic), it’s well above the previous three years.

The takeaway for you: There are purchasers in the market, and they’re ready and willing to buy.

Mt. Hood real estate inventory sits at a total of six properties currently for sale! Three of these properties are over a million dollars. What better time to get top price and multiple offers for your property!

The law of supply and demand tells us that if you want the best price possible and to negotiate your ideal contract terms, put your house on the market when there’s strong demand and less competition.

A recent study by realtor.com reveals that, unlike in previous years, sellers plan to list their homes this winter instead of waiting until spring or summer. The study shows that 65% of sellers who plan to sell in 2022 have either already listed their home (19%) or are planning to put it on the market this winter.

Again, if you’re looking for the best price and the ability to best negotiate the other terms of the sale of your house, listing before this competition hits the market makes sense.

In 2020, there were over 979,000 new single-family housing units authorized by building permits. Many of those homes have yet to be built because of labor shortages and supply chain bottlenecks brought on by the pandemic. They will, however, be completed in 2022. That will create additional competition when you sell your house. Beating these newly constructed homes to the market is something you should consider to ensure your house gets as much attention from interested buyers as possible.

If you’re moving into a larger, more expensive home, consider doing it now. Prices are projected to appreciate by approximately 5% over the next 12 months. That means it will cost you more (both in down payment and mortgage payment) if you wait. You can also lock in your 30-year housing expense with a mortgage rate in the low 3’s right now. If you’re thinking of selling in 2022, you may want to do it now instead of waiting, as mortgage rates are forecast to rise throughout the year.

Consider why you’re thinking of selling in the first place and determine whether it’s worth waiting. Is waiting more important than being closer to your loved ones now? Is waiting more important than your health? Is waiting more important than having the space you truly need?

Only you know the answers to those questions. Take time to think about your goals and priorities as we move into 2022 and consider what’s most important to act on now.

If you’ve been debating whether or not to sell your house and are curious about market conditions in your area, let’s connect so you have expert advice on the best time to put your house on the market.

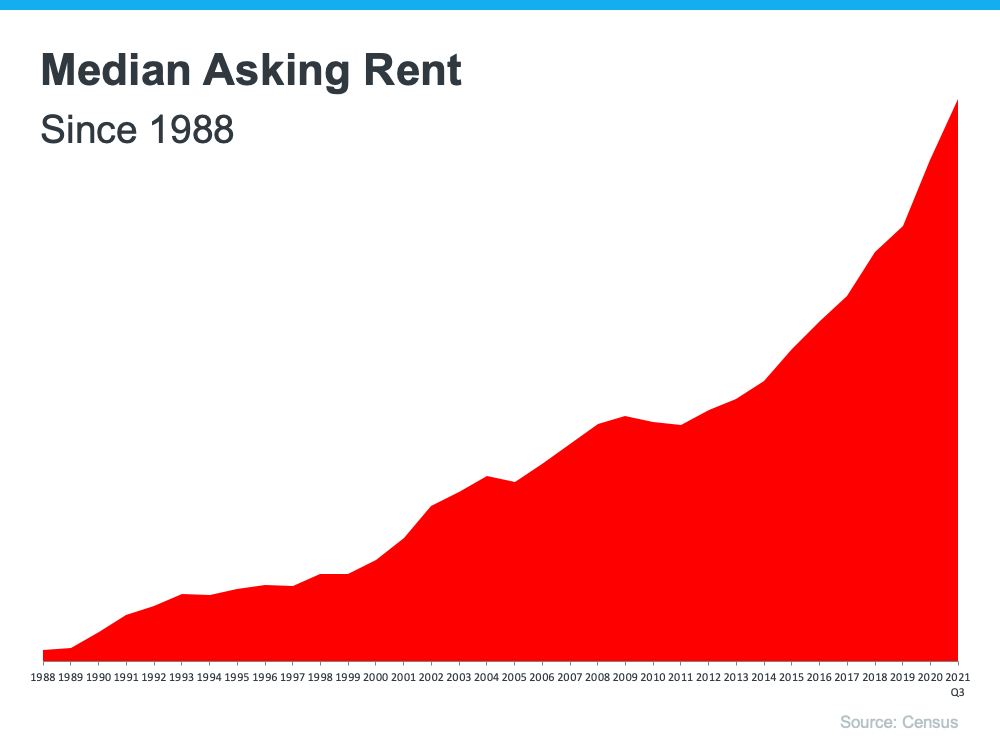

Are you one of the many renters thinking about where you’ll live the next time your lease is up? Before you decide whether to look for a new house or another apartment, it’s important to understand the true costs of renting in 2022.

As a renter, you should know rents have been rising since 1988 (see graph below):

In 2021, rents grew dramatically. According to ApartmentList.com, since January 2021:

“. . . the national median rent has increased by a staggering 17.8 percent. To put that in context, rent growth from January to November averaged just 2.6 percent in the pre-pandemic years from 2017-2019.”

That increase in 2021 was far greater than the typical rent increases we’ve seen in recent years. In other words – rents are rising fast. And the 2022 National Housing Forecast from realtor.com projects prices for vacant units will continue to increase this year:

“In 2022, we expect this trend will continue and fuel rent growth. At a national level, we forecast rent growth of 7.1% in the next 12 months, somewhat ahead of home price growth . . .”

That means, if you’re planning to move into a different rental this year, you’ll likely pay far more than you have in years past.

If you’re a renter facing rising rental costs, you might wonder what alternatives you have. If so, consider homeownership. One of the many benefits of homeownership is it provides a stable monthly cost you can lock in for the duration of your loan.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“. . . fast-rising rents and increasing consumer prices, may have some prospective buyers seeking the protection of a fixed, consistent mortgage payment.”

If you’re planning to make a move this year, locking in your monthly housing costs for 15-30 years can be a major benefit. You’ll avoid wondering if you’ll need to adjust your budget to account for annual increases.

Homeowners also enjoy the added benefit of home equity, which has grown substantially right now. In fact, the latest Homeowner Equity Insight report from CoreLogic shows the average homeowner gained $56,700 in equity over the last 12 months. As a renter, your rent payment only covers the cost of your dwelling. When you pay your mortgage, you grow your wealth through the forced savings that is your home equity.

If you’re thinking of renting this year, it’s important to keep in mind the true costs you’ll face. Let’s connect so you can see how you can begin your journey to homeownership today.

In case you missed this:

HAPPY NEW YEAR!

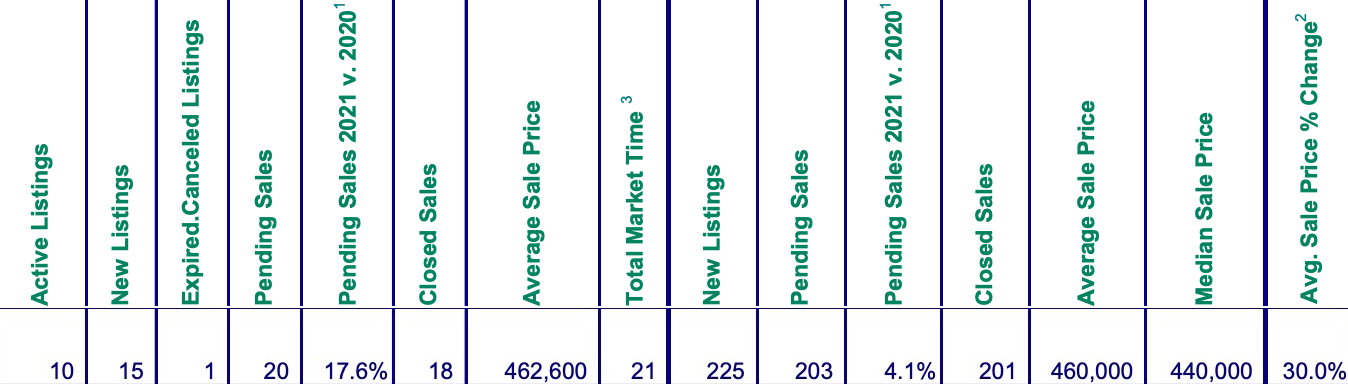

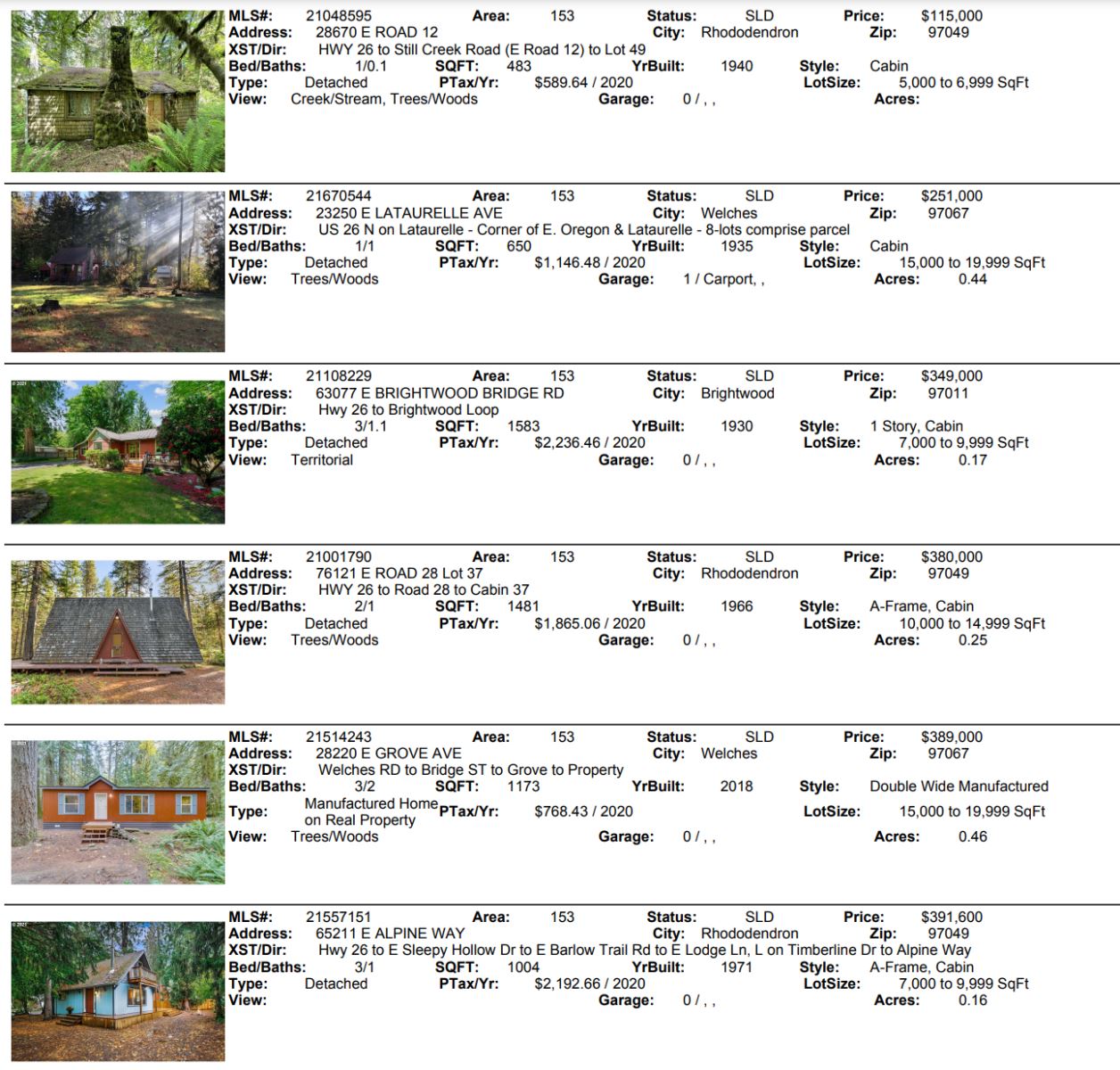

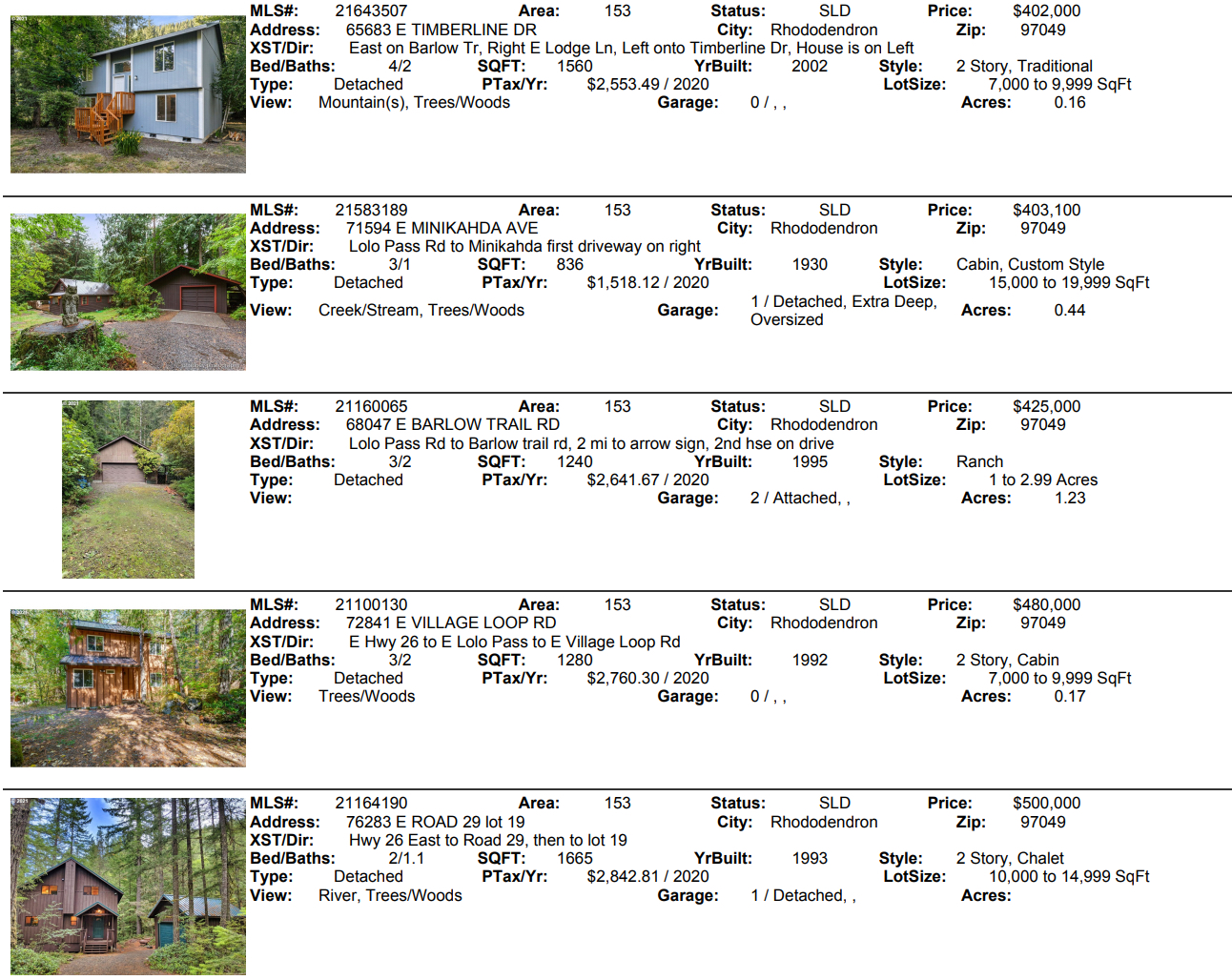

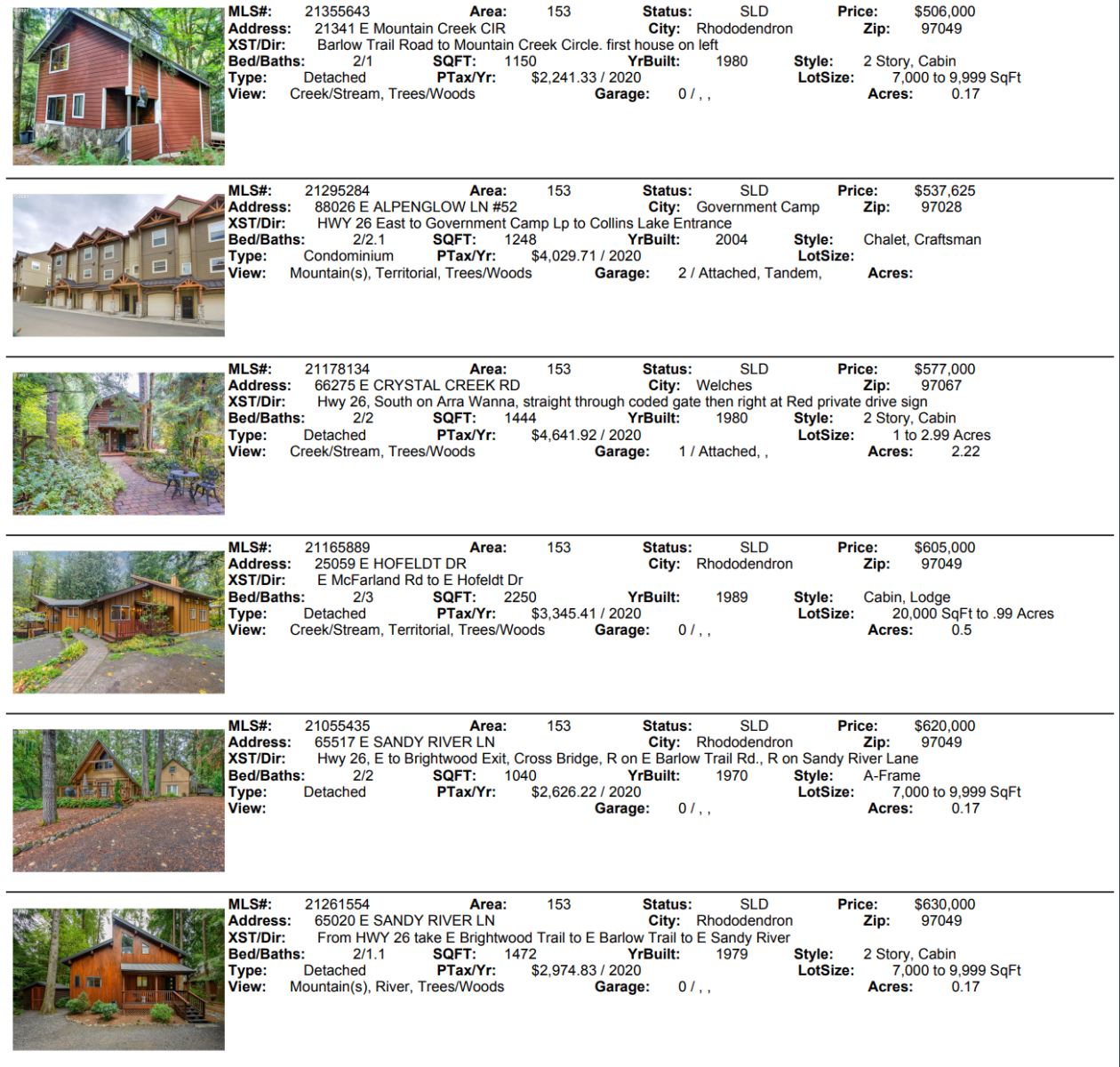

These are interesting times for Mt. Hood real estate as we head into 2022. After reviewing Novembers final sales we see a total of 18 closing with six sales under $400,000. Timberline Rim, one of the mountains most affordable subdivisions, saw five sales with three over a half a million dollars! November also produced the first $500,000 forest service cabin sale! More "off the chart" record breaking numbers were in Collins Lake at Government Camp. Three units have sold since July for $537,000, $557.000 and one at $606,000.

Needless to say, nearly every property that hits the market has five or more offers on the table making this the most amazing sellers market in Mt. Hood history. Two thousand twenty two will be very interesting if we don't get more inventory soon. Currently there are seven properties for sale and three are over a million dollars.

Recent snows may have slowed buyers down a little bit but the bottom line is once the current eleven pending sales close we will be down to nearly zero properties. Who knows what next year will look like at this point. This year we had a 30% increase in prices which was probably the greatest of all the areas tracked in our multiple listing. No doubt about it, Mt. Hood is the place to be!

Listed below are Novembers closed sales in Brightwood, Welches, Rhododendron and Government Camp.

December National News

U.S. Real Estate Overview

Note: November 2021 data below are the most recent released by the National Association of Realtors.

Existing-home sales rose in November, denoting three consecutive months of increases, according to the National Association of Realtors®. Three of the four major U.S. regions reported growth in monthly sales, while the fourth region held steady in November. From a year-over-year perspective, only one region experienced a rise in sales as the three others saw home sales decline.

Total existing-home sales (transactions that include single-family homes, townhomes, condominiums and co-ops) grew 1.9% from October to a seasonally adjusted annual rate of 6.46 million in November. Sales fell 2.0% from a year ago (6.59 million in November 2020).

Total housing inventory at the end of November amounted to 1.11 million units, down 9.8% from October and down 13.3% from one year ago (1.28 million). Unsold inventory sits at a 2.1-month supply at the current sales pace, a decline from both the prior month and from one year ago.

The median existing-home price for all housing types in November was $353,900, up 13.9% from November 2020 ($310,800), as prices increased in each region, with the highest pace of appreciation in the South region. This marks 117 straight months of year-over-year increases, the longest-running streak on record.

Properties typically remained on the market for 18 days in November, equal to October and down from 21 days in November 2020. Eighty-three percent of homes sold in November 2021 were on the market for less than a month.

In October, first-time buyers were responsible for 26% of sales in November, down from 29% in October and from 32% in November 2020. NAR's 2021 Profile of Home Buyers and Sellers – released earlier this month – reported that the annual share of first-time buyers was 34%.

Investing in Real Estate

Today's low interest rates and rising home prices have created some great investment opportunities!

Today's low interest rates and rising home prices have created some great investment opportunities!

Investing in real estate has unique advantages over other types of investments. Let's take a look at some of the reasons why real estate investment should be on the "short list" for many investors:

Many investors are taking advantage of these great market conditions. Have questions? Give us a call. We are happy to help!

Are bi-weekly payments right for you?

Many people ask about bi-weekly payment plans designed to reduce the interest paid out over the course of your loan. These programs help the borrower budget an extra payment a year, and over time this can knock years off the repayment schedule.

Many people ask about bi-weekly payment plans designed to reduce the interest paid out over the course of your loan. These programs help the borrower budget an extra payment a year, and over time this can knock years off the repayment schedule.

Many people are surprised to learn that they can do this themselves without any special programs, simply by submitting an extra principal payment as they are able. By submitting an extra payment, you get the advantages of an early payout, without the extra contractual obligation. Want more information on other mortgage options?

Contact us today for our list of preferred local mortgage experts who can help you position yourself for a great year in 2020!

It's Now Much Easier to Buy A Home

Since the pandemic began, Americans have reevaluated the meaning of the word home. That’s led some renters to realize the many benefits of homeownership, including the feelings of security and stability and the financial benefits that come with rising home equity. At the same time, many current homeowners have decided their house no longer meets their needs, so they moved into homes with more space inside and out, including a home office for remote work.

However, not every purchaser has been able to fulfill their desire for a new home. Here are two obstacles some homebuyers are facing:

This past week, both of those challenges have been mitigated to some degree for many purchasers. The FHFA (which handles mortgages by Freddie Mac, Fannie Mae, and the Federal Housing Administration) is raising its loan limit for prospective purchasers in 2022. The term used to describe the maximum loan amount they will entertain is the Conforming Loan Limit.

Investopedia explains the difference in a recent post:

“Conforming loans are the only loans that meet the requirements to be acquired by Fannie Mae and Freddie Mac. Jumbo loans, which exceed the conforming limit, are the most common type of nonconforming loan.”

A Forbes article earlier this year explains the benefits of a conforming loan and why they exist:

“Since lenders can’t sell non-conforming loans to Fannie Mae or Freddie Mac to free up their cash, they’re a bit riskier for the lender. This is especially true for jumbo loans, which aren’t backed by any government guarantees. If you default on a jumbo loan, it’s a huge blow to the lender.

Thus, lenders generally charge higher interest rates to compensate, and they can have even more requirements. For example, lenders who give out jumbo loans often require that you make a down payment of at least 20% and show that you have at least six months’ worth of cash in reserve, if not more.”

The FHFA has significantly increased its Conforming Loan Limits for 2022. Sandra L. Thompson, FHFA Acting Director, explains in the press release that:

“Compared to previous years, the 2022 Conforming Loan Limits represent a significant increase due to the historic house price appreciation over the last year. While 95 percent of U.S. counties will be subject to the new baseline limit of $647,200, approximately 100 counties will have conforming loan limits approaching $1 million.”

This means that more homes now qualify for a conforming loan with lower down payment requirements and easier lending standards – the two challenges holding many buyers back over the last year.

The Federal Housing Administration (FHA) also increased its Conforming Loan Limits for 2022. That could also mean an easier path to homeownership for many prospective buyers. As the Forbes article explains:

“FHA loans can be very beneficial if you don’t have as much savings, or if your credit score could use some work.”

Buying your first or your next home may have just gotten much easier (less stringent qualifying standards) and less expensive (possibly lower mortgage rate). Let’s connect to discuss how these changes may impact you.

As we move into 2022, both buyers and sellers are wondering, what’s next? Will there be more homes available to buy? Will prices keep climbing? How high will mortgage rates go? For the answer to those questions and more, we turn to the experts. Here’s a look at what they say we can expect in 2022.

“Consensus forecasts put rates at about 3.7% by the end of next year. So, that's still historically low, but certainly higher than they are today.”

“Affordability will increasingly be a challenge as interest rates and prices rise, but remote work may expand search areas and enable younger buyers to find their first homes sooner than they might have otherwise. And with more than 45 million millennials within the prime first-time buying ages of 26-35 heading into 2022, we expect the market to remain competitive.”

“With more housing inventory to hit the market, the intense multiple offers will start to ease. Home prices will continue to rise but at a slower pace.”

“We also expect a growing number of homeowners to bring properties to market, taking some pressure off high prices and offering buyers more options.”

“Strong demographic demand will continue to act as the wind in the housing market’s sails.”

Hope is on the horizon for 2022. You should see your options grow as more homes are listed and some of the peak intensity of buyer competition starts to ease. Just remember, rising rates and prices are a great motivator for you to find the home of your dreams sooner rather than later so you can buy while today’s affordability is still in your favor.

Make no mistake – this sellers’ market will remain in 2022 as home prices are projected to continue climbing, just at a more moderate pace. Selling your house while buyer demand is so high will truly put you in the driver’s seat. But don’t wait too long. With more listings projected to become available, your ideal window of opportunity to stand out from the crowd won’t last forever. Work with an agent who knows your local market and current inventory conditions to ensure you have the support you need to make an educated and informed decision about selling in the coming year.

If you’re thinking of buying or selling, 2022 may be your year. Let’s connect to discuss your goals and the unique opportunities you have in today’s housing market.

Once you’ve found your dream home and applied for a mortgage, there are some key things to keep in mind before you close. It’s exciting to start thinking about moving in and decorating your new place, but before you make any large purchases, move your money around, or make any major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.

Here’s a list of things you shouldn’t do after applying for a mortgage. They’re all important to know – or simply just good reminders – for the process.

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

New debt comes with new monthly obligations. New obligations create new qualifications. People with new debt have higher debt-to-income ratios. Since higher ratios make for riskier loans, qualified borrowers may end up no longer qualifying for their mortgage.

When you co-sign, you’re obligated. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

Remember, lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be impacted. Lower credit scores can determine your interest rate and possibly even your eligibility for approval.

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants of your score.

Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. The best plan is to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

![2022 Housing Market Forecast [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/12/15133953/20211217-MEM-1046x2117.png)

Displaying blog entries 291-300 of 1849