The Truth About Affordability Today on Mt. Hood

The Truth About Affordability Today

Let's be real with each other for a second about affordability. Because you deserve someone who will be honest and transparent about what’s going on, especially if you’ve got a move on your mind.

Here’s the full picture of what’s happening and why. The good – and the bad. So, you know what it truly means for your move. Because while rates are certainly a big part of affordability, they’re not the only factor at play.

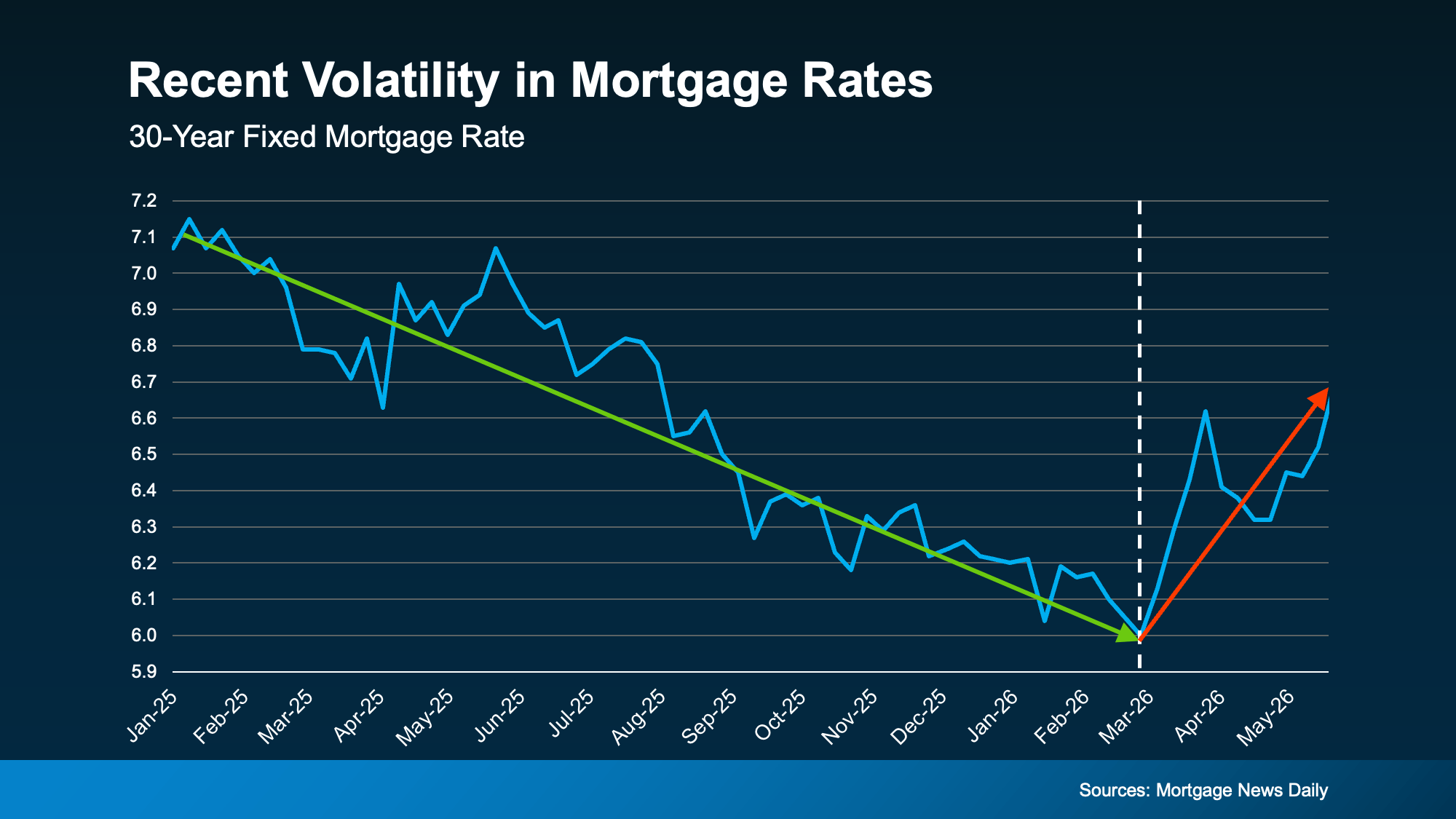

Mortgage Rates Have Been Rising

After a year or more of rates trending down, they’ve started to climb again. And, if you’re looking to buy, that’s not what you want to see. But it has happened. And here’s why.

Uncertainty is the enemy of mortgage rates.

And with lingering global uncertainty, ongoing tensions in the Middle East, and inflation refusing to fully cool off, there’s a lot that’s having an effect on rates. Colin Robertson, Founder of The Truth About Mortgage, put it plainly:

"You can't have $100 a barrel oil and not expect inflation to rise, which translates to higher bond yields and mortgage rates."

Take a look at the graph below. It uses data from Mortgage News Daily to show just how much all of those factors have had an impact:

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it's probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it's probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It's possible. But it all depends on how the ongoing geopolitical conflict plays out and whether inflation continues to run hot afterwards – and for how long.

Rates probably aren't heading down until both of those things improve. And even when that does happen, experts agree rates likely won’t be dramatically lower – maybe in the low to mid-6s. That's the reality, and it's worth knowing.

So, should you wait for lower rates? The general consensus is, if you can afford to buy and you find a home you like, it’s still worth it. Because no one knows for sure when rates will start to come back down – and how long do you really want to put your life on hold?

Wages Are Outpacing Home Prices

You've probably heard that inflation is making everything more expensive, and there's no shortage of headlines about the cost-of-living outpacing paychecks. It's a legitimate concern. And maybe you’re feeling the pinch yourself. But here's what doesn't make the headlines. It's not all bad news.

Data from the Federal Reserve Bank of Atlanta and Redfin shows wages have actually been growing faster than home prices.

-

Recently, wages have been increasing at around 4% year-over-year.

-

And home price growth is closer to 2% year-over-year.

As a buyer, you want your income to rise faster than prices because that helps make your purchase more manageable financially, and it quietly chips away at the affordability challenge over time. That’s exactly what we’re seeing lately. And every little bit is going to help.

A big reason wages have been gaining ground on home prices? Home prices have actually stayed pretty steady.

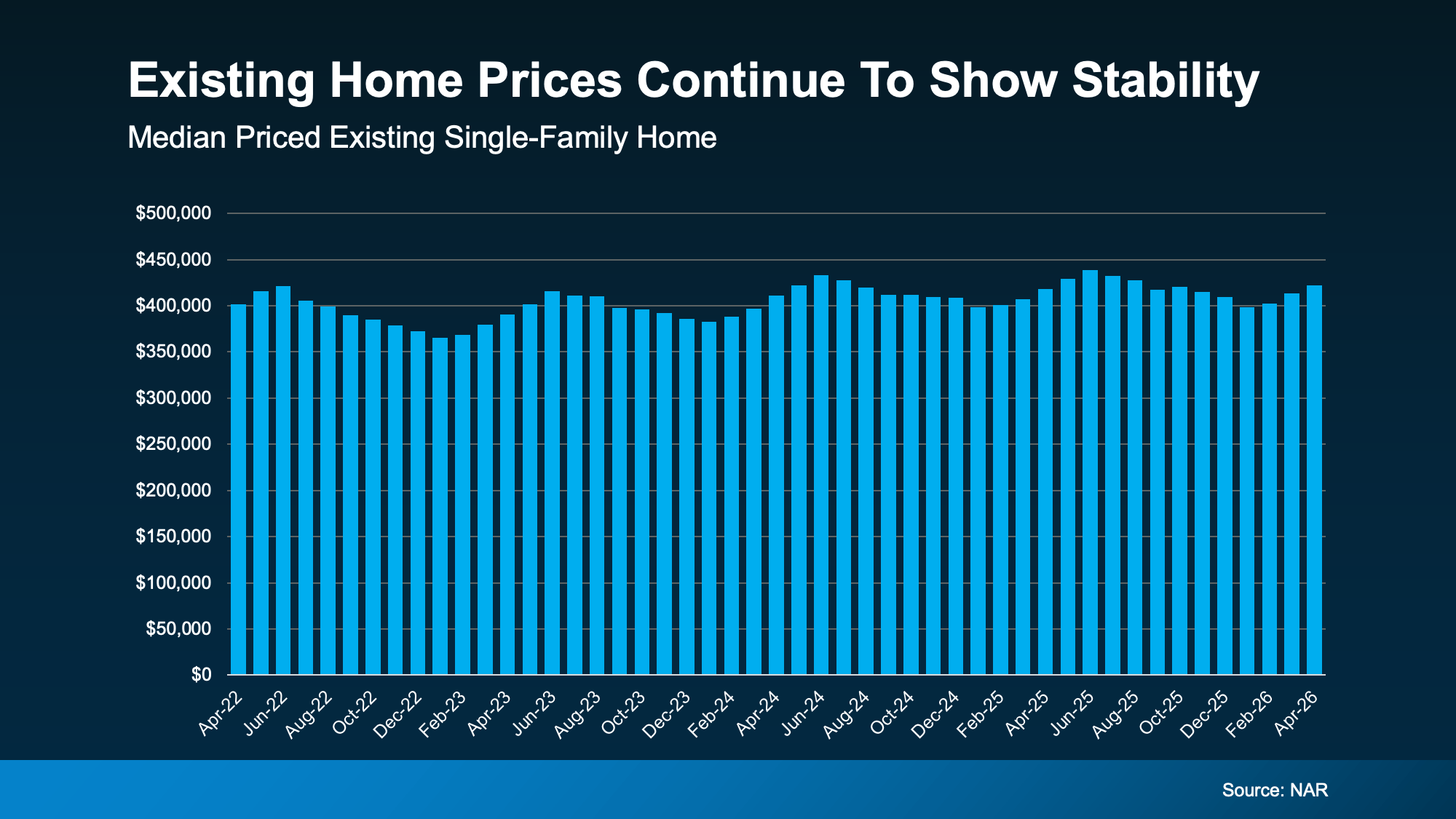

Existing Home Prices Have Held Steady

Check out the graph below. It shows home price data from the National Association of Realtors (NAR) over the past 4 years. Notice anything? There's been no dramatic runup, and no crash either. Just relative stability and slow growth:

Part of what's keeping prices this stable is that buyers finally have more choices. That means less competition, more negotiating power, and more time to find the home that actually fits your life, not just the one you had to grab before someone else did.

And that gives you a chance to hopefully find something that works for your budget, even with today’s rates. At the same time, you're not losing ground pricewise while you take time to make a careful decision.

Bottom Line

Yes, rates have been volatile, and global instability is keeping them from settling down anytime soon. There’s no sugar coating that. But the full picture of affordability is more nuanced than the headlines suggest.

Want to run the real numbers for your situation? Let's talk. Reach out and let's set up a quick, no-pressure conversation.