Five Reasons to Sell Your Mt. Hood Home or Cabin This Winter

Thursday, December 1, 2022

Add Comment

Displaying blog entries 331-340 of 1996

If you’re thinking about buying a home, you’re likely trying to juggle your needs, current mortgage rates, home prices, your schedule, and more to try to decide if you want to jump into the market.

If this sounds like you, here’s one key factor that could help you with your decision: there are more homes for sale today than there were at this time last year. According to Calculated Risk, for the week ending in November 18th, there were 47.7% more homes available for sale than there were at the same time in 2021. And having more options for your home search may be exactly what you need to feel confident about making a move.

Here’s a look at where the increased housing supply is coming from so you can get a better sense of what’s happening in the market today and what it means for you.

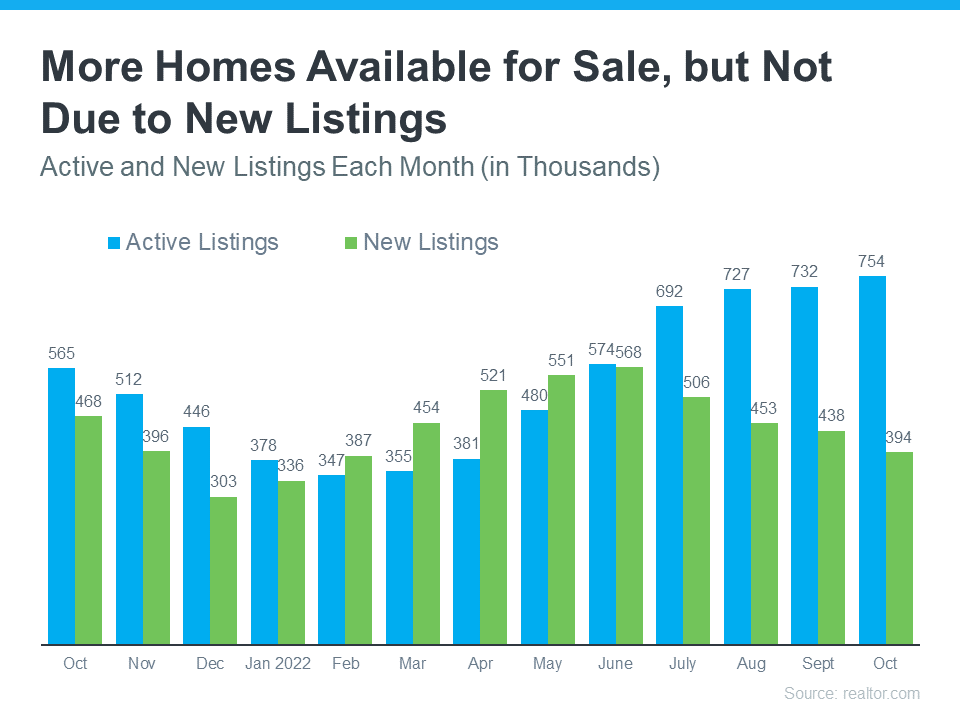

The increase we’ve seen in housing supply this year isn’t from the source you think it is. Rather than an influx of recent homeowners listing their houses for sale (known as new listings), the primary reason the supply has grown is because homes are staying on the market a bit longer (known as active listings).

That’s happening because higher mortgage rates and home prices have helped moderate the peak frenzy of buyer demand, which has slowed down the pace of sales. And, as the pace of sales has eased, inventory has grown as a result.

The graph below uses data from realtor.com to show that it’s active listings, not new listings, that have driven the growth we’ve seen over the past few months:

And while overall inventory gains may slow down this winter due to typical housing market seasonality, you still have a chance to capitalize on the current supply.

Regardless of the source, the increase in available housing supply is good for buyers. More homes available for sale means you have more options to choose from as you search for your next home, and you may even have more time to consider them.

So, if you tried to buy a home last year and lost out in a bidding war or just couldn’t find something you liked, this may be the news you’ve been waiting for. If you start your search today, those additional options should make it less difficult to find a home you love, especially as some other buyers pause their search this holiday season.

Just remember, housing supply is still low overall, so it won’t suddenly be easy – it’ll just be less challenging than it was at this time last year. As a recent article from realtor.com says:

“Despite this improvement in the number of homes actively for sale, active listings still lag their pre-pandemic levels.”

The increase in housing supply helps put you in a great position to kick off the new year in your dream home. And who better to help you find it than a trusted, local real estate professional?

If you’re ready to jump into the housing market and see what’s available in our local area, let’s connect.

From our good friends in the Mt. Hood National Forest

|

||||||||||||||||||||||

![Should You Update Your House Before You Sell? Ask a Real Estate Professional. [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/11/16134552/Should-You-Update-Your-House-Before-You-Sell-Ask-A-Real-Estate-Professional-MEM-1046x2648.png)

There’s no denying the housing market is undergoing a shift this season, and that may leave you with some questions about whether it still makes sense to sell your house. Here are three of the top questions you may be asking – and the data that helps answer them – so you can make a confident decision.

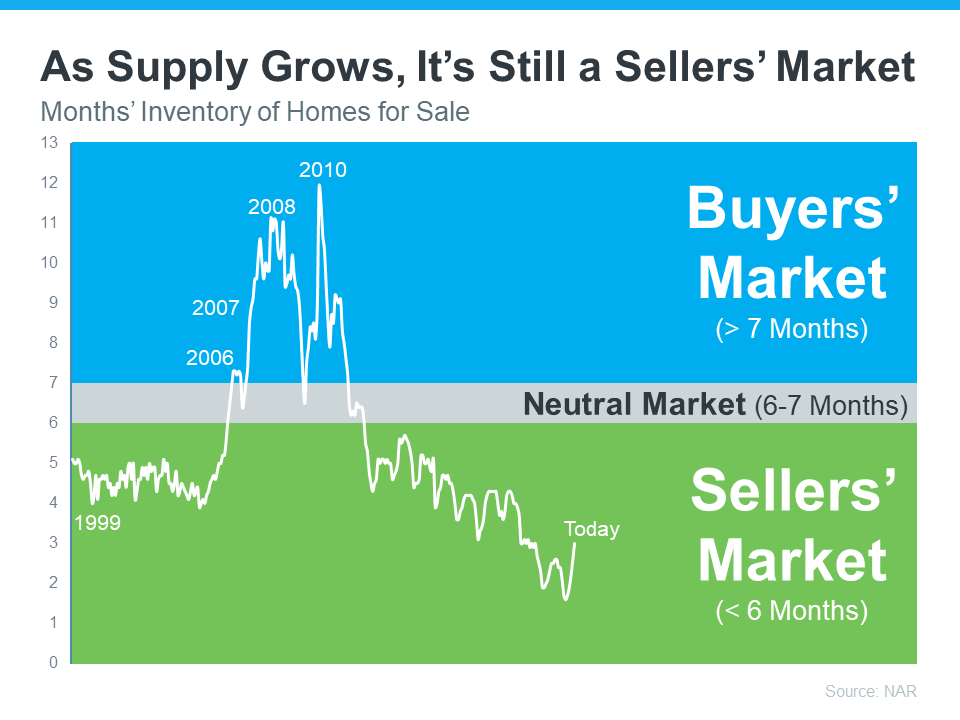

Even though the supply of homes for sale has increased in 2022, inventory is still low overall. That means it’s still a sellers’ market. The graph below helps put the inventory growth into perspective. Using data from the National Association of Realtors (NAR), it shows just how far off we are from flipping to a buyers’ market:

While buyers have regained some negotiation power as inventory has grown, you haven’t missed your window to sell. Your house could still stand out since inventory is low, especially if you list now while other sellers hold off until after the holiday rush and the start of the new year.

Check out local numbers for Mt. Hood! Only twenty eight properties currently for sale and a two month supply of inventory. It's a great time to have your property for sale on Mt. Hood.

If you’re thinking of selling your house but are hesitant because you’re worried buyer demand has disappeared in the face of higher mortgage rates, know that isn’t the case for everyone. While demand has eased this year, millennials are still looking for homes. As an article in Forbes explains:

“At about 80 million strong, millennials currently make up the largest share of homebuyers (43%) in the U.S., according to a recent National Association of Realtors (NAR) report. Simply due to their numbers and eagerness to become homeowners, this cohort is quite literally shaping the next frontier of the homebuying process. Once known as the ‘rent generation,’ millennials have proven to be savvy buyers who are quite nimble in their quest to own real estate. In fact, I don’t think it’s a stretch to say they are the key to the overall health and stability of the current housing industry.”

While the millennial generation has been dubbed the renter generation, that namesake may not be appropriate anymore. Millennials, the largest generation, are actually a significant driving force for buyer demand in the housing market today. If you’re wondering if buyers are still out there, know that there are still people who are searching for a home to buy today. And your house may be exactly what they’re looking for.

If current market conditions have you worried about how you’ll afford your next move, consider this: you may have more equity in your current home than you realize.

Homeowners have gained significant equity over the past few years and that equity can make a big difference in the affordability equation, especially with mortgage rates higher now than they were last year. According to Mark Fleming, Chief Economist at First American:

“. . . homeowners, in aggregate, have historically high levels of home equity. For some of those equity-rich homeowners, that means moving and taking on a higher mortgage rate isn’t a huge deal—especially if they are moving to a more affordable city.”

If you’re thinking about selling your house this season, let’s connect so you have the expert insights you need to make the best possible move today.

Experts agree there’s no chance of a large-scale foreclosure crisis like we saw back in 2008, and that’s good news for the housing market. As Mark Fleming, Chief Economist at First American, says:

“. . . don’t expect a housing bust like the mid-2000s, as lending standards in this housing cycle have been much tighter and homeowners have historically high levels of home equity, so there likely won’t be a surge in foreclosures.”

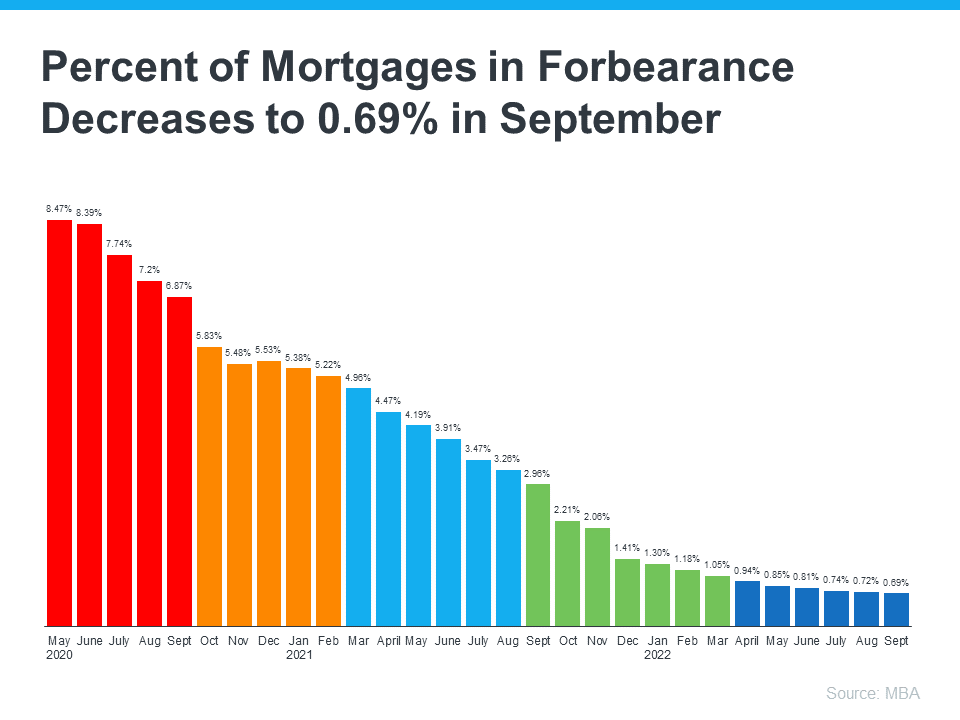

Data from the Mortgage Bankers Association (MBA) helps tell this story. It shows the overall percentage of homeowners at risk is decreasing significantly with time (see graph below):

But even though the volume of homeowners at risk is very low, there is still a small percentage of homeowners who may be coming face to face with foreclosure as a possibility today. If you’re facing difficulties yourself, it can help to understand your options. It starts with knowing what foreclosure is. Investopedia defines it like this:

But even though the volume of homeowners at risk is very low, there is still a small percentage of homeowners who may be coming face to face with foreclosure as a possibility today. If you’re facing difficulties yourself, it can help to understand your options. It starts with knowing what foreclosure is. Investopedia defines it like this:

“Typically, default is triggered when a borrower misses a specific number of monthly payments . . . Foreclosure is the legal process by which a lender attempts to recover the amount owed on a defaulted loan by taking ownership of and selling the mortgaged property.”

The good news is there are alternatives available to help you avoid going through the foreclosure process, including:

But before you go down any of those paths, it’s worth seeing if you have enough equity in your home to sell it and protect your investment.

Equity is the difference between what you owe on the home and its market value based on factors like price appreciation.

In today’s real estate market, many homeowners have far more equity in their homes than they realize due to the home price appreciation we’ve seen over the past few years. According to CoreLogic:

“The total average equity per borrower has now reached almost $300,000, the highest in the data series.”

So, what does that mean for you? If you’ve lived in your house for at least a few years or more, chances are your home’s value, and your equity, has risen dramatically. In addition, the mortgage payments you’ve made during that time chipped away at the balance of your loan. If your home’s current value is higher than what you still owe on your loan, you may be able to use that increase to your advantage.

Rick Sharga, Executive VP of Market Intelligence at ATTOM Data, explains how equity can help:

“Very few of the properties entering the foreclosure process have reverted to the lender at the end of the foreclosure. . . We believe that this may be an indication that borrowers are leveraging their equity and selling their homes rather than risking the loss of their equity in a foreclosure auction.”

To find out how much equity you have, work with a local real estate professional. They can give you an estimate of what your house could sell for based on recent sales of similar homes in your area. You may be able to sell your house to avoid foreclosure.

If you find out you have to pursue other options, your agent can help with that too. They’ll be able to connect you with other professionals in the industry, like housing counselors, who can look into your unique situation and offer advice on next steps if selling isn’t your best alternative.

If you’re a homeowner facing hardship, let’s connect so you have an expert on your side to explore your options and see if you can sell your house to avoid foreclosure.

Now that the end of 2022 is within sight, you may be wondering what’s going to happen in the housing market next year and what that may mean if you’re thinking about buying a home. Here’s a look at the latest expert insights on both mortgage rates and home prices so you can make your best move possible.

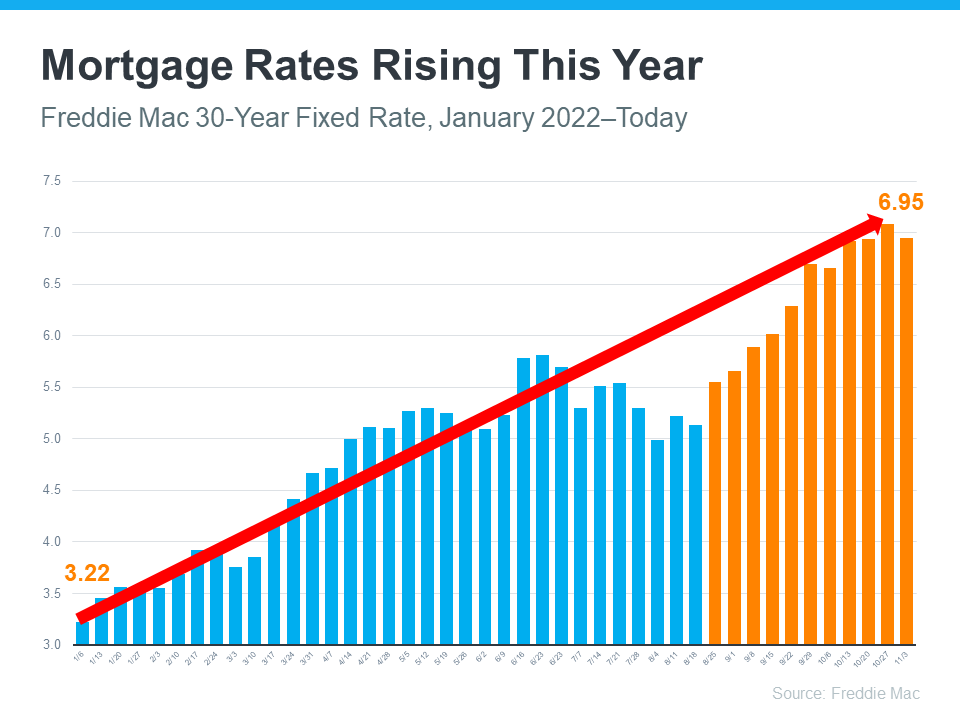

There’s no doubt mortgage rates have skyrocketed this year as the market responded to high inflation. The increases we’ve seen were fast and dramatic, and the average 30-year fixed mortgage rate even surpassed 7% at the end of last month. In fact, it’s the first time they’ve risen this high in over 20 years (see graph below):

In their latest quarterly report, Freddie Mac explains just how fast the climb in rates has been:

“Just one year ago, rates were under 3%. This means that while mortgage rates are not as high as they were in the 80’s, they have more than doubled in the past year. Mortgage rates have never doubled in a year before.”

Because we’re in unprecedented territory, it’s hard to say with certainty where mortgage rates will go from here. Projecting the future of mortgage rates is far from an exact science, but experts do agree that, moving forward, mortgage rates will continue to respond to inflation. If inflation stays high, mortgage rates likely will too.

As buyer demand has eased this year in response to those higher mortgage rates, home prices have moderated in many markets too. In terms of the forecast for next year, expert projections are mixed. The general consensus is home price appreciation will vary by local market, with more significant changes happening in overheated areas. As Mark Fleming, Chief Economist at First American, says:

“House price appreciation has slowed in all 50 markets we track, but the deceleration is generally more dramatic in areas that experienced the strongest peak appreciation rates.”

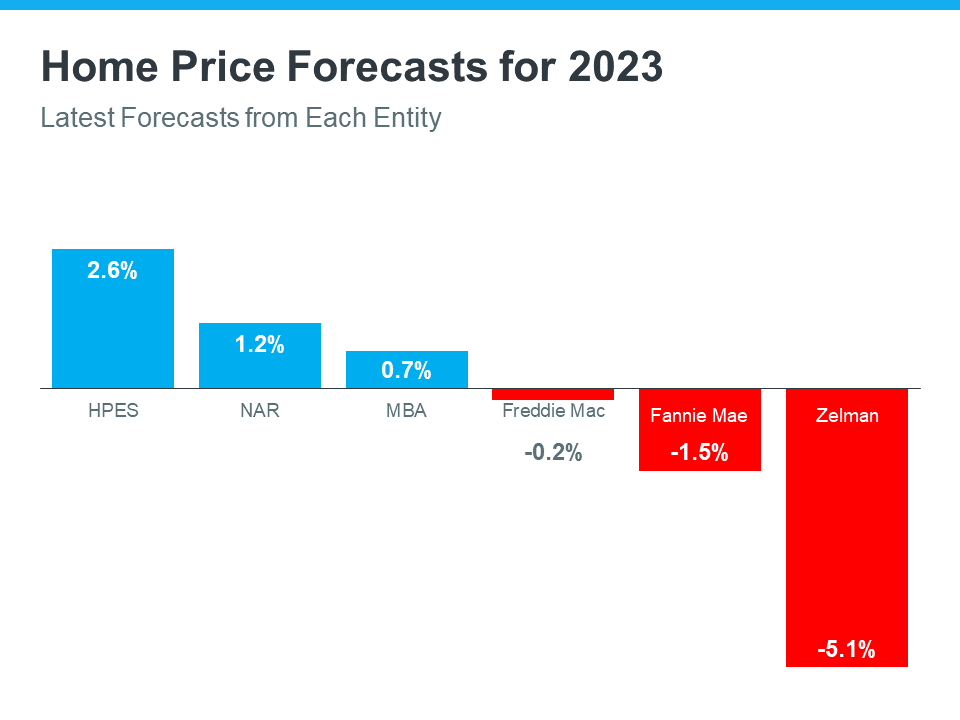

Basically, some areas may still see slight price growth while others may see slight price declines. It all depends on other factors at play in that local market, like the balance between supply and demand. This may be why experts are divided on their latest national forecasts (see graph below):

If you want to know what’s happening with home prices or mortgage rates, let’s connect so you have the latest on what experts are saying and what that means for our area.

As you look ahead to the winter season, you’re likely making plans and thinking about what you want to achieve before the year ends. One of those key decision points could be whether or not you want to move this year. If the location or size of your current home no longer meets your needs, finding a house that better suits your lifestyle may be a top priority for you. But with today’s cooling housing market, is it really a good time to sell your house, or should you wait?

If you’re ready to make your decision, here are three reasons you may want to consider selling before the holidays.

Typically, in the residential real estate market, homeowners are less likely to list their houses toward the end of the year. That’s because people get busy around the holidays and de-prioritize selling their house until the start of the new year when their schedules and social calendars calm down.

Selling now, while other homeowners may hold off until after the holidays, can help your house stand out. Start the process with a real estate professional today so you can get your house on the market and get ahead of your competition.

Even though housing supply has increased this year as buyer demand has moderated, it’s still low overall. That means there aren’t enough homes on the market today, especially as the millennial generation reaches their peak home buying years. As Mark Fleming, Chief Economist at First American, says:

“While not the frenzy of 2021, the largest living generation, the Millennials, will continue to age into their prime home-buying years, creating a demographic tailwind for the housing market.”

Serious buyers will still be looking this winter and your house may be exactly what they’re searching for. If you work with an agent to list your house now, you’ll be able to get in front of the eager buyers who are hoping to make a move before the year ends.

Don’t forget, today’s homeowners have record amounts of equity. According to CoreLogic, the average amount of equity per mortgage holder has climbed to almost $300,000. That’s an all-time high. That means the equity you have in your house right now could cover some, if not all, of a down payment on the home of your dreams.

And as you weigh the reasons to sell before winter, don’t lose sight of why you’re thinking about moving in the first place. Maybe it’s time to buy a house that’s in a better location for you, has the space you and your loved ones have been craving, or simply gives you that sense of home. A trusted real estate advisor can help you determine how much home equity you have and how you can use it to achieve your goal of making a move.

Mt. Hood inventory is LOW! We only have 32 properties for sale and seven are over a million dollars and six of them are in Mt. Hood Village. Mt. Hood Village is a park with mobile homes with park rent running $700 per month on up. That doesn't leave very many properties to choose from for today's buyers!

If you’re thinking about selling your house so you can find a home that better suits your needs, don’t delay your plans. Let’s connect so you can accomplish your goals before winter.

Displaying blog entries 331-340 of 1996