Only 5% of Sellers Sell Without an Agent

Wednesday, June 24, 2026

Add Comment

Displaying blog entries 1-10 of 1996

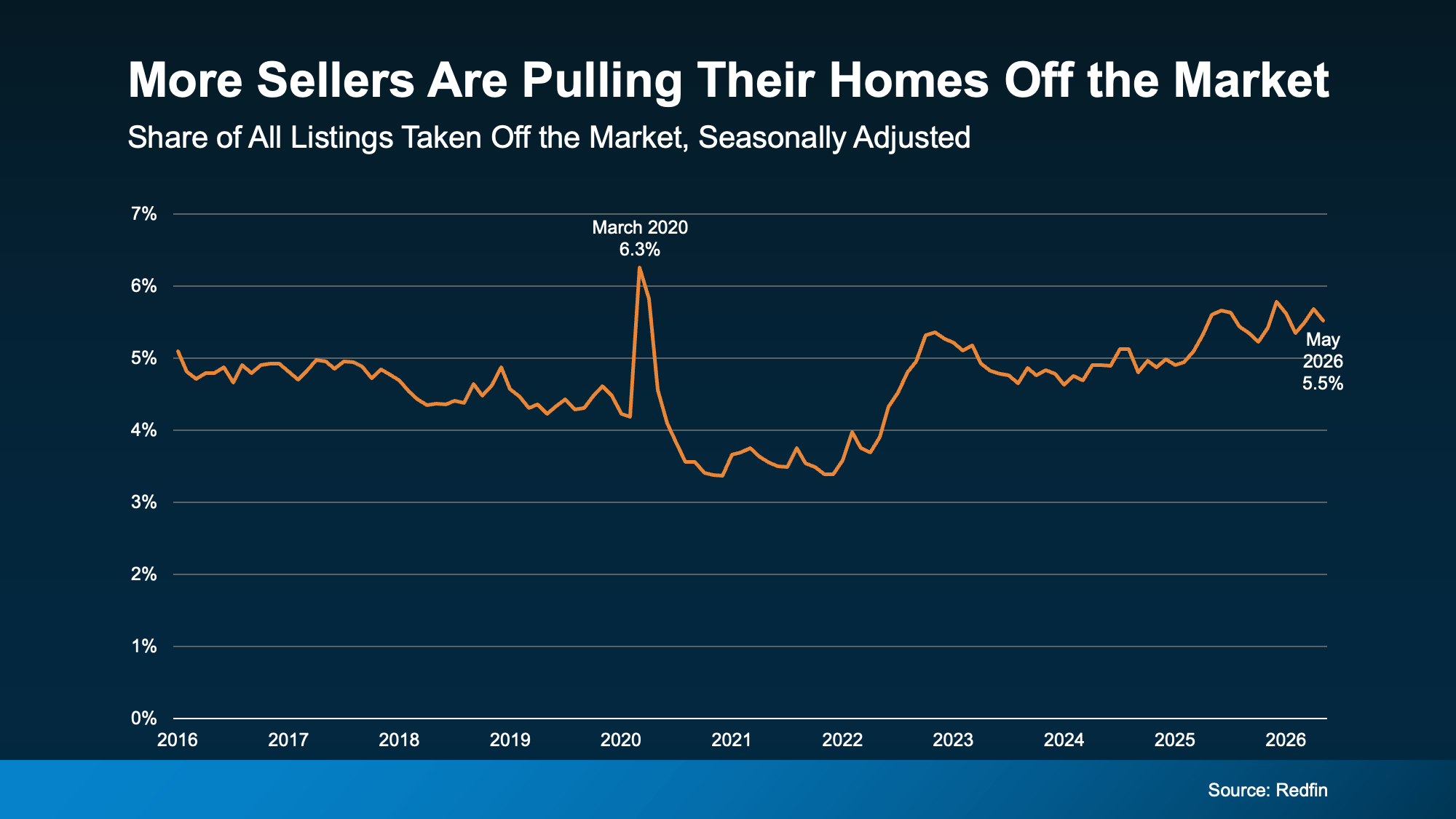

You may be hearing that a near-record number of homeowners are pulling their houses off the market. And if that headline has you thinking, “Wait… is something bad about to happen?” You’re not alone.

Because when people start stepping to the sidelines, it sounds like a warning sign that something’s coming – or that they realize something you don’t know.

Here’s the thing. This trend gets spun like it means the market is about to crash. But the data tells a more practical story.

According to the latest data from Redfin, 5.5% of all listings were taken off the market in May. And it’s true that’s almost the highest it’s been since back in March 2020 (see graph below):

That can sound scary. But a lot of the fear comes from how this story gets told. “A near record number of sellers are pulling their listings” makes a great clickbait headline – and that sort of thing spreads fast, especially online. But sellers pull a house off the market for plenty of reasons that have nothing to do with a crash.

Redfin points to four main forces driving this trend:

Homes are taking longer to sell. When the pace slows down, some sellers get frustrated and decide to hold off.

The number of homes for sale is rising faster than demand. That means buyers have more options. And sellers who don’t price or prep right may not get many eyes on their house.

Some sellers still have pandemic-era price expectations. A price that would’ve worked a couple years ago may not match what today’s buyers will pay.

Economic uncertainty is making both buyers and sellers cautious. Buyers pause. Sellers second-guess. And that has an impact on overall sales volume and pace.

Notice what’s missing from that list? There isn’t a single mention of an impending market crash or price collapse.

This is about a shifting pace, more competition, and sellers deciding how they want to respond.

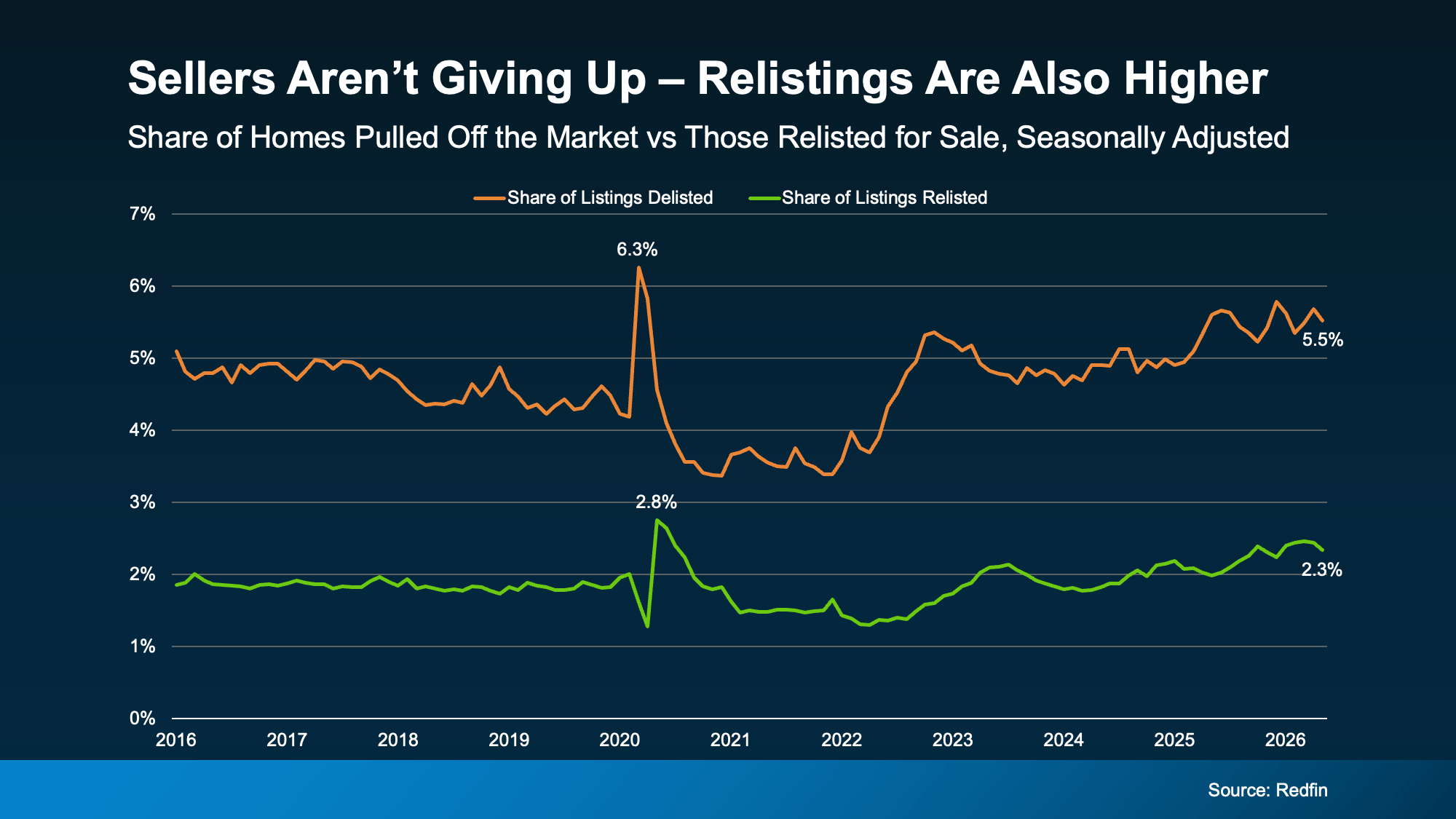

Want more peace of mind that this isn’t a crash? This next stat delivers. Yes, more sellers are taking their homes off the market. But Redfin also shows something you're not going to see in social posts...

The number of re-listings is growing too.

While more sellers are pulling their listings, more are also deciding to give selling a second shot too. This is pretty much the highest re-listings have been since the pandemic hit.

While 5.5% got pulled in May, 2.3% were also put back on the market (see graph below):

That’s a signal sellers aren’t giving up or running away in large numbers.

Some are simply stepping away briefly before deciding to try again. That tells you this often isn’t a permanent decision. In many cases, it’s a pause – and the seller comes back with a different approach.

A lot of the time that change in the overall strategy is all that’s needed to finally get a house sold.

And just in case you need more proof this isn’t a reason to worry, check this out. Buyer activity may be starting to pick back up – and that could bring more sellers back in or, at least, prevent some sellers from pulling back.

The National Association of Realtors (NAR) reports existing home sales increased 3.2% in May. That’s the biggest increase since December. As the Wall Street Journal puts it:

“Home sales in May posted the biggest rise this year, a sign that the housing market’s crucial spring selling season may be showing signs of life after a sluggish start.”

That doesn’t sound like a market in trouble.

If you’re seeing headlines about how a record number of sellers are taking their homes off the market, don’t panic. It’s not a warning of an impending crash. It’s a market adjusting.

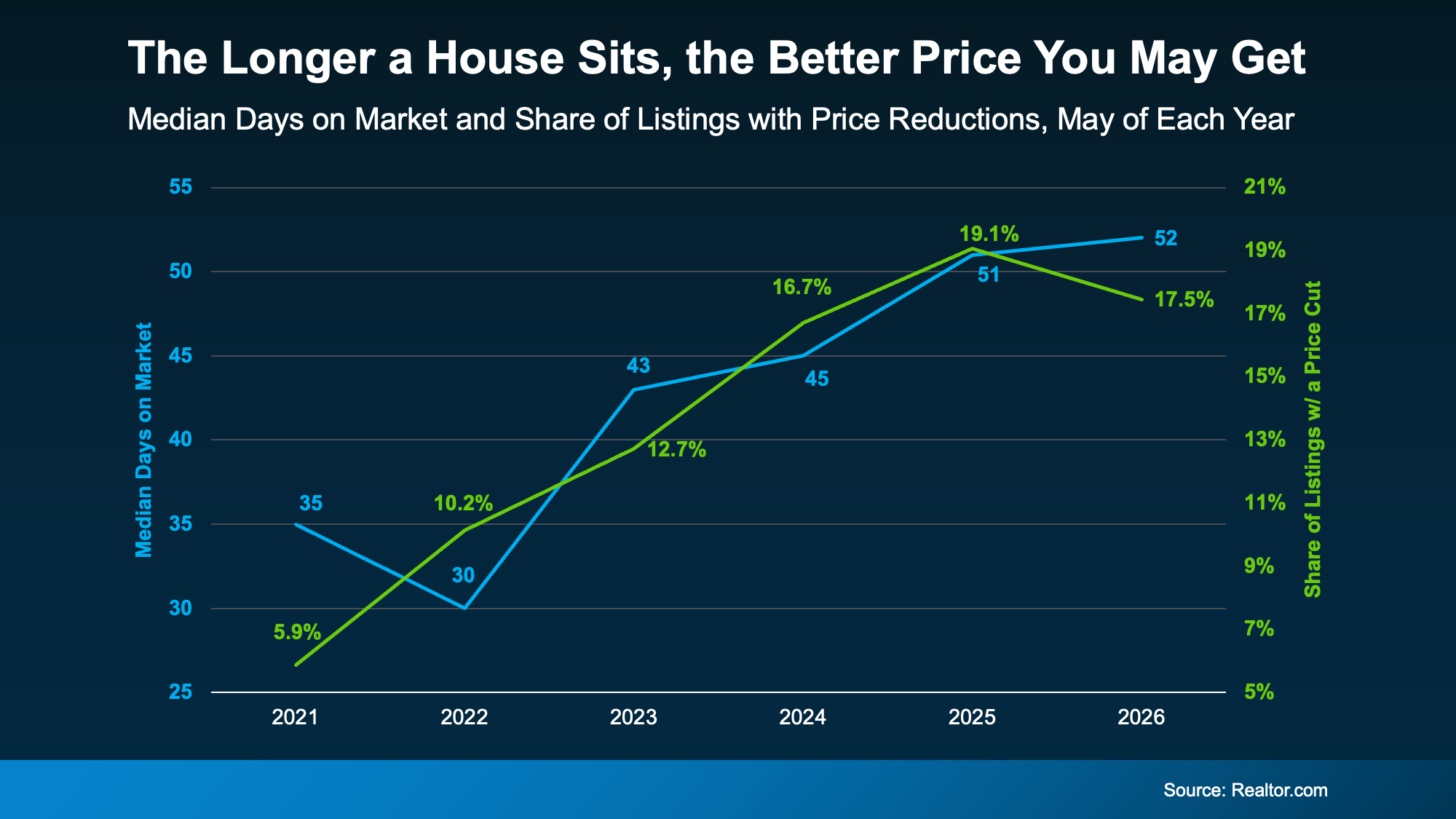

Open up a home search and you'll see them. Listings that have been on the market for two months. Three. Some longer.

Most buyers scroll right past them, assuming something’s wrong with the house. But that instinct could be costing you, since the longer a home sits, the more motivated the seller usually gets.

If affordability has been your #1 hurdle to buying, here’s a surprisingly simple strategy that could help you finally get your foot in the door. Start with the homes that have been sitting the longest. That’s often where the best deals are.

Here’s why. Data from Realtor.com shows there’s a connection between longer time on the market and lower sales prices. Basically, the longer a house sits, the more likely it is that the seller will reduce the price (see graph below):

The blue line tracks how long homes stay on the market, while the green line tracks the share of homes getting a price reduction. As one climbs, so does the other.

And if you focus on these homes that are just sitting and waiting, the opportunity for you is bigger than you may think right now.

Redfin data shows there’s $347 billion worth of stale listings on the market right now – more than ever before for this time of year. So, ask your agent to filter listings for you from oldest to newest. The home that fits your budget might already be there. Just further down the list than you thought.

Let’s say you do that and something catches your eye. Still, you might be questioning why the home has been sitting in the first place. Just remember, sometimes it has nothing to do with the home itself.

According to Redfin, common causes are:

The asking price was set too high to start

The home didn’t show well online

There are a lot of homes for sale in the area, so it just got buried

So, nothing that’s necessarily a dealbreaker, or even anything that’s wrong with the home itself. If there’s a real issue, a thorough inspection will surface it. And that’s information you can use to negotiate. Not a reason to assume it’s a house worth skipping over.

So how do you capitalize on a lingering listing? According to USA Today, you have two main levers to pull.

The first is price. Work with your agent to study what comparable homes recently sold for, then build an offer around that. Coming in below asking price is fair game when a home has been sitting.

The second is concessions. If a seller won’t budge much on price, they may still help in other ways, like covering some closing costs, repair credits, or even a mortgage rate buydown that lowers your monthly payment.

A local agent has the context to tell which homes are the real opportunities and which are skippable.

A house sitting on the market isn’t always a glaring red flag. In today’s market, it may be your best opportunity yet.

For help deciding which lingering listings are actually worth a second look, let’s connect.

.jpeg)

Remember a few years back when sellers held all the power and buyers were stuck offering way over asking or waiving inspections just to get a chance at the house? In many markets, those days are behind us.

While it’s going to vary by area, more metros are slowly shifting to favor buyers, and the market is starting to look a lot more like a two-way street again.

And that balance is something we haven’t had in a while.

Whether you're buying or selling, here's what you need to know about what's changing and what it means for your move.

The national data tells an interesting story right now. According to Realtor.com:

"The national housing market is balanced but gradually loosening as the cycle moves in a more buyer-friendly direction . . ."

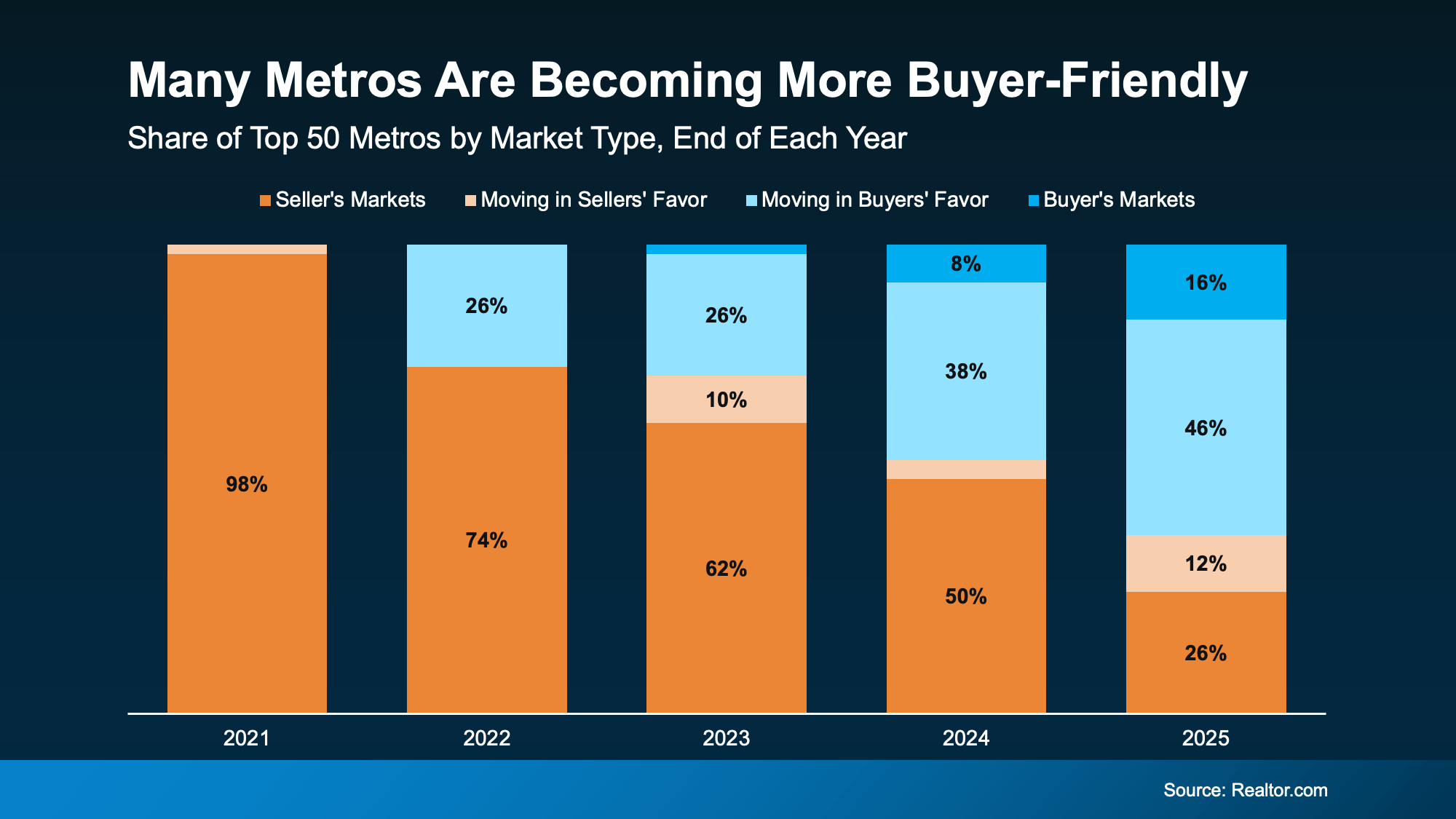

That’s because, over the past few years, more and more metros have been flipping back to more buyer-friendly terms as inventory’s grown. And when you zoom in on the latest Realtor.com data for the top 50 metro markets over time, the trend becomes really clear (see graph below).

Back in 2021, almost all major metros were seller's markets. By the end of 2025, only 1 in 3 still favored sellers. That's an obvious shift.

And that changes how the market is going to feel for everyone. Sellers shouldn’t still expect 2021 conditions, but neither should buyers. At least, not generally speaking.

That said, who has the power ultimately depends on where you live. While more metros are leaning buyer-friendly lately, there are still plenty of strong seller's markets right now, too.

It really comes down to how much housing supply and demand there is in your area. And that varies enormously by region.

Sun Belt cities like Austin, Tampa, and San Antonio saw major building booms in recent years, giving buyers more options and more negotiating room. Meanwhile, cities in the Northeast and Midwest – think Rochester, Hartford, and Buffalo – didn't see that same wave, so inventory stayed tight and competition stayed fierce. As Jeff Ostrowski, Housing Analyst at Bankrate, explains:

“The formerly hot Sun Belt markets have cooled, while the Northeast and Midwest have stayed hot. The big driver here is construction activity. The softest markets now [have] experienced big booms that spurred new building, and that has led to a large supply of new and existing homes on the market in those places.”

To find out who has the power in your local market, talk to an agent. Because knowing what’s happening locally is going to be the key to setting the right strategy for your move.

If the market is working in your favor, great. Lean in and use it to your benefit. But if it’s not, all hope isn’t lost. Your agent can help you figure out how to approach any market.

Here's some practical advice if there’s a mismatch between your goal and local market conditions.

If you're buying in a seller's market:

Get pre-approved before you start shopping. It shows sellers you're serious.

Be ready to act fast when the right home hits the market.

Consider offering a quick closing date or flexible terms.

Work closely with your agent to craft a competitive offer.

If you're selling in a buyer's market:

Price it right from day one. Overpricing will cost you time and money.

Focus on curb appeal and staging to stand out in areas with more inventory.

Be open to offering incentives, like covering closing costs or a home warranty.

Expect buyers to negotiate and be ready to be flexible.

Right now, local markets are moving in very different directions. And your strategy as a buyer or seller should reflect your market.

Want to know which way our local market is leaning and what that means for your move? Let's connect.

Public Hearing on STR program this Thursday

Last week, the Board of County Commissioners heard a presentation from county staff about the future of the short-term rental (STR) program:

On that webpage, you can review the presentation to the Board, and the adjoining packet of materials. This coming Thursday, June 11, the Board will hold a public hearing at 10 a.m. on the STR County Code updates:

This public hearing – the first of two – is an opportunity for any members of the public to comment on the changes to the STR program. Any resident can attend and give testimony either in-person or via Zoom (Zoom info here). Learn how to provide effective testimony.

Share This Email

Share This Email

Share This Email

Clackamas County | 2051 Kaen Rd | Oregon City, OR 97045 US

Whether you're dreaming about buying your first home or wondering if it’s time to move on from the one you're in, affordability is probably weighing on your mind. Home prices are still high in many markets, and even though things have improved a bit over the past year, making the numbers work can still feel like a stretch.

But the people finding ways to move right now usually have one thing in common. They didn't wait for affordability to come to them. They went looking for it.

According to PODS, 61% of people across all generations say affordability is the biggest factor when deciding where to move. And it's led a growing number of people to do one thing – broaden their search to include more affordable areas they hadn't seriously considered before. As PODS, put it:

". . . moving is increasingly driven by affordability, connection, and quality of life. As economic pressures persist, Americans are taking a more intentional, values-driven approach to where they choose to live.”

Here's where it gets really interesting. When people talk about moving for affordability, they're not just talking about finding a cheaper house. They're thinking about the full picture. What does it actually cost to live somewhere?

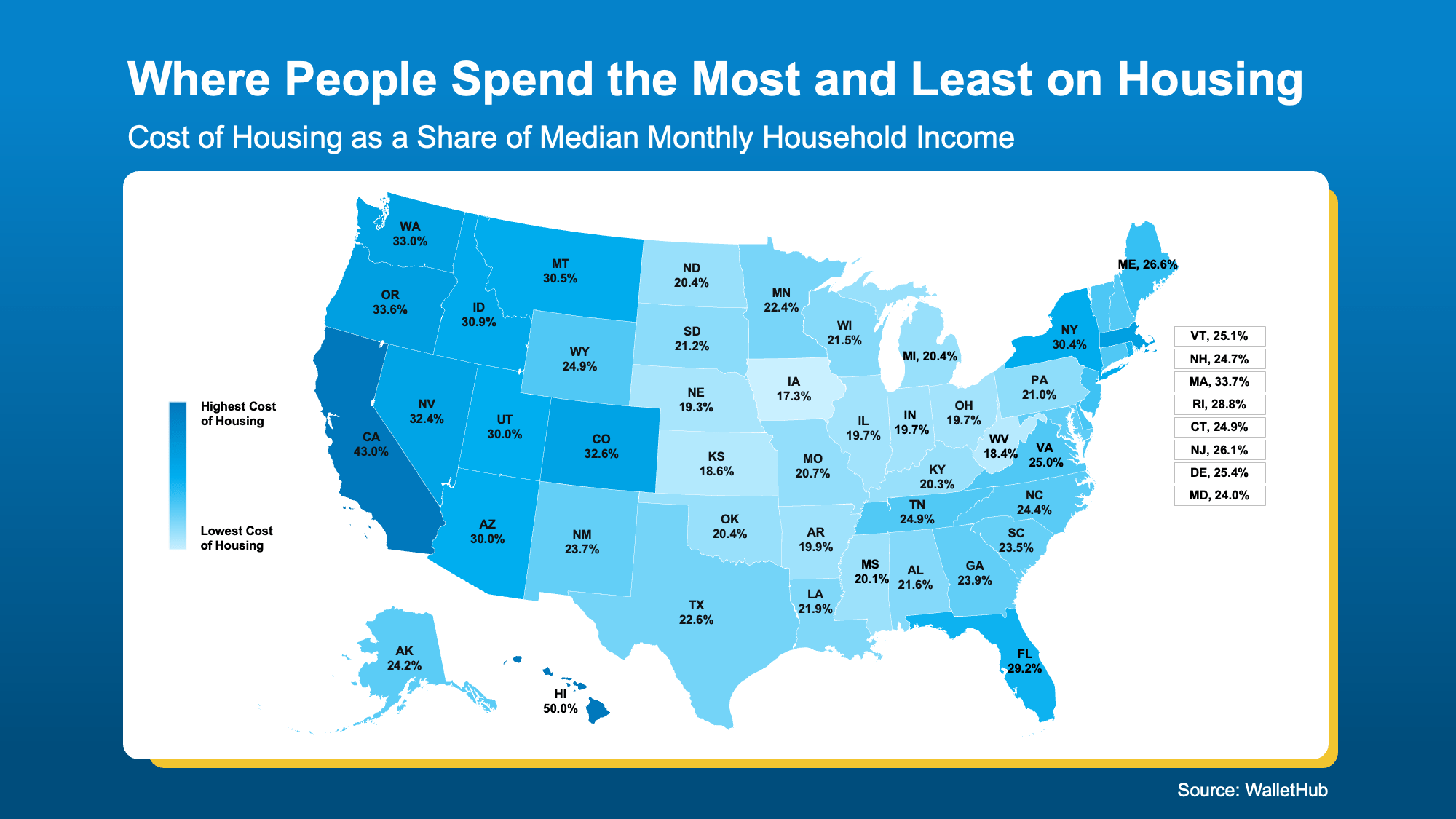

WalletHub looked at exactly this, measuring housing costs as a share of median monthly household income across every state (see map below).

Take a look at where you live on that map. The lighter the blue, the more affordable it generally is to live there. The darker the blue? Just the opposite.

If your state is showing up on the darker blue end of the scale, the cost of living may be putting a real pinch on your wallet, and it may be worth exploring what a lighter-blue area could mean for your finances.

Because if you're less financially stretched, imagine how that could change things. Less stress. Less worry. More freedom and peace of mind.

But finding more affordable homeownership doesn't have to mean a cross-country move. It doesn't even have to mean leaving your state, your family, or your favorite coffee shop behind.

Every market has more affordable pockets that most buyers never think to explore – neighborhoods, towns, and communities where home prices are lower, property taxes are more manageable, and the overall cost of living just works better.

A great local real estate agent knows exactly where those places are.

And if you work remotely, or have any flexibility in where you're based, your options open up even further. Remote work has already changed the way millions of people think about where to live, and that trend isn't going away.

When location stops being tied to a daily commute, a more affordable area that's a bit farther out suddenly becomes a very real option.

Affordability is a real challenge, but it's not an unsolvable one. The key is being open to places you might not have considered before. A local real estate agent can help you find them.

Ready to find out which areas have the best affordability right now? Reach out today.

If the housing market feels confusing right now, you’re not alone.

Mortgage rates have risen. Home sales haven't picked up like expected. And many buyers and sellers are wondering when things are going to feel easier or be more affordable.

The truth is: a lot changed over the first half of this year.

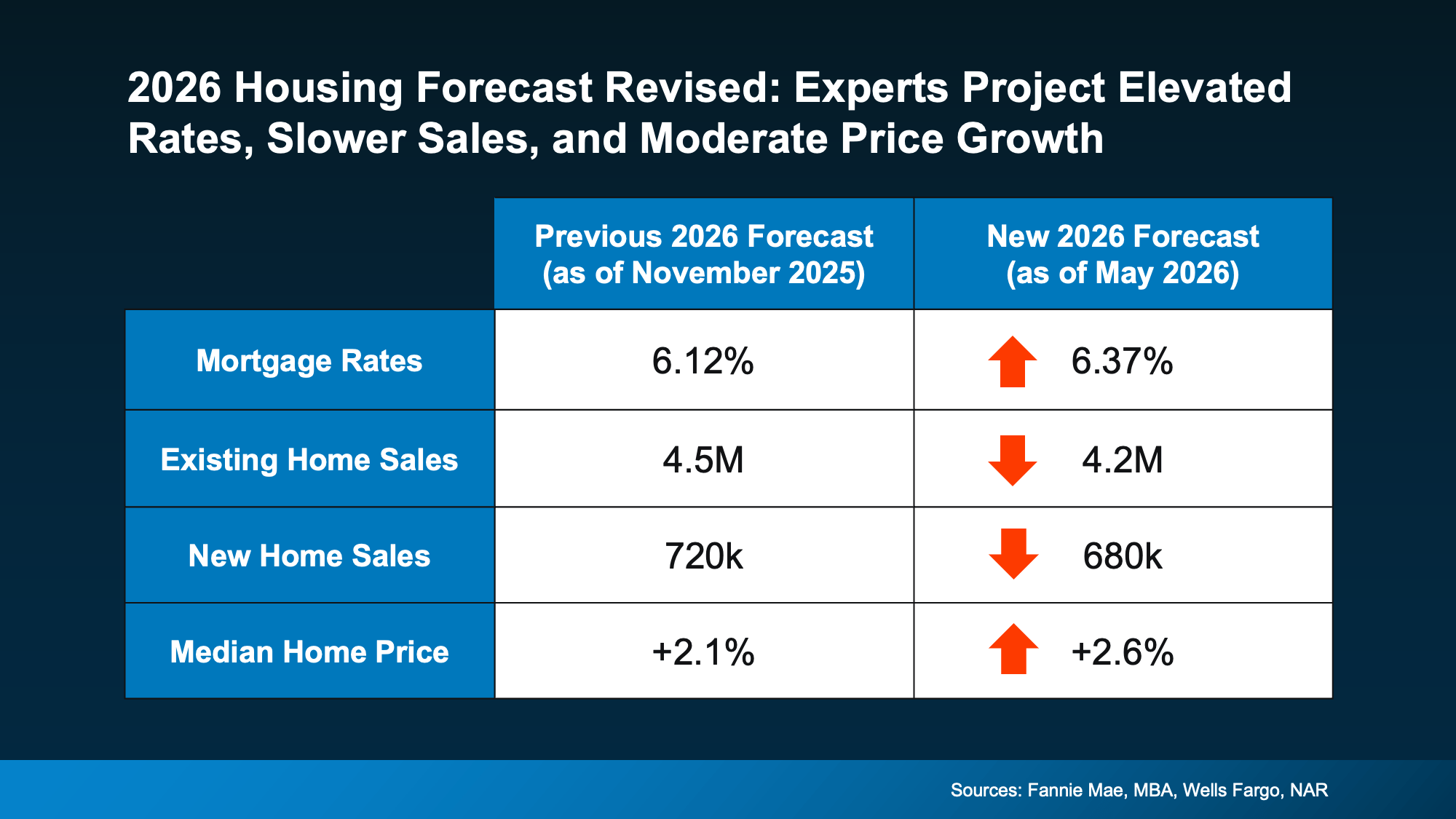

Back at the end of 2025, economists were forecasting a much stronger housing market for 2026. They expected mortgage rates to come down, affordability to improve more dramatically, and home sales to rebound.

But lingering inflation, economic uncertainty, and growing geopolitical tensions overseas pushed mortgage rates higher than expected. And because rates stayed elevated for longer, many buyers continued to hold off.

That’s why experts recently revised their housing forecasts for the rest of the year (see graph below):

So, what does this actually mean for you? Let’s break it down.

While just about everyone wants mortgage rates to go back to the uppers 5s or low 6s we saw at the start of the year, as of right now, the experts don’t think that’s likely to happen this year.

Instead, forecasts have been updated from the low 6s they originally projected. Many industry organizations are saying rates will stay in roughly the mid 6s this year. The good news is, that’s still lower than rates were a year ago.

Of course, this is based on what we know today. If the conflict overseas comes to an end or inflation drops, this could change. But if you’re waiting for lower rates, it may not pay off in the way you expect.

Back in late 2025, experts expected we’d sell an average of 4.5 million homes this year. Now? That’s dropped down a bit to 4.2 million.

That tells us something important: buyers are still hesitant because affordability remains challenging.

Higher mortgage rates have made monthly payments harder to manage, especially for first-time buyers. And that’s slowed the pace of the market compared to what was originally expected. But even though the forecast was revised down, we’re still expected to sell more homes than last year.

Once geopolitical tensions resolve and rates begin to settle down, many experts believe that group of buyers will be ready to jump back in. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

There has already been a few glimmers of renewed hope lately. In recent months, pending homes sale have been improving month-over-month despite higher rates.

So, if you’re able to afford a home at today’s rates, it could still make sense to buy now. Because otherwise, if you wait, you’ll have more competition (and potentially fewer homes to choose from) when those others buyers jump back in.

Builders also expected to have a stronger year. Earlier forecasts projected new home sales would top 700k in 2026. Now, economists expect we'll be just shy of that number.

Again, mortgage rates are a major reason why.

But the upside for buyers is that builders may be even more motivated to sell. That means builder incentives, negotiation opportunities, and pricing flexibility may continue in many markets. So, if you live somewhere where there’s more new construction, this may actually be a bright spot for you.

Builders could be more ready to negotiate, and that gives you more leverage to get a better deal.

This is one of the most important takeaways from the entire forecast. Even though sales activity is slower, on average, experts did not revise their home price forecast downward.

They still expect prices to rise nationally this year.

Why? Because while buyer demand has softened, the number of homes for sale is still relatively limited overall. That imbalance is helping support prices, even in a slower market.

Of course, conditions vary depending on where you live. Some markets are cooling more than others. But nationally, experts are still projecting steady price growth — not a major decline. And that should be a comfort whether you’re buying or selling.

Because sellers don’t want a major drop in prices. And while buyers may think they do, generally you feel better about a big purchase when it doesn’t depreciate right away.

The housing market hasn’t rebounded as quickly as experts originally hoped. But that doesn’t mean it’s stalled.

Higher inflation and lingering economic uncertainty caused economists to revise their forecasts for this year. But importantly, when those two things settle down, many experts believe the market will regain its momentum.

So don’t see this revision in forecasts as a sign of trouble. See it as a temporary reaction to overall conditions and uncertainty.

If you want to know what’s happening in our local market, and what it could mean for your plans for the rest of this year, let’s connect.

Let's be real with each other for a second about affordability. Because you deserve someone who will be honest and transparent about what’s going on, especially if you’ve got a move on your mind.

Here’s the full picture of what’s happening and why. The good – and the bad. So, you know what it truly means for your move. Because while rates are certainly a big part of affordability, they’re not the only factor at play.

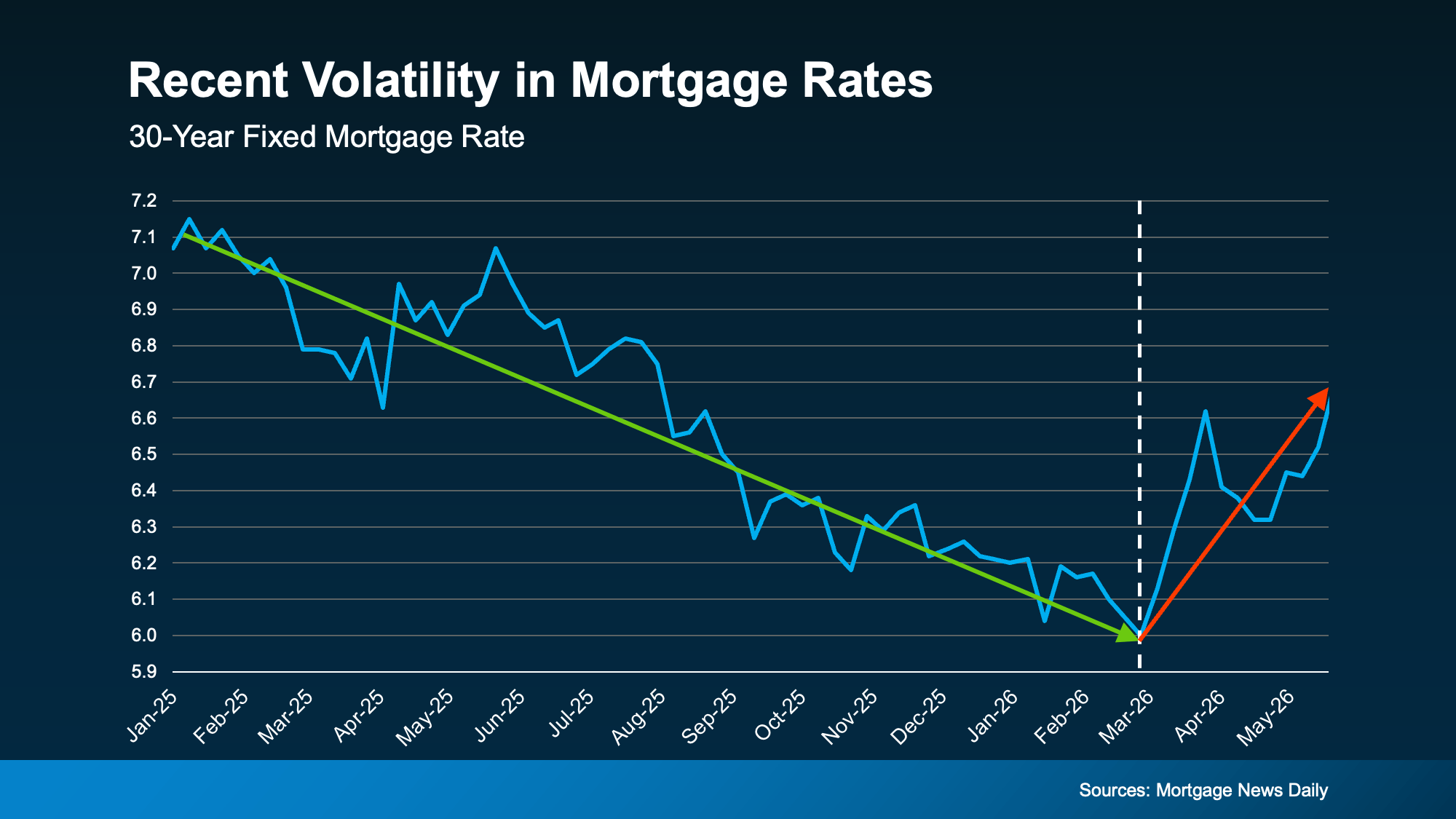

After a year or more of rates trending down, they’ve started to climb again. And, if you’re looking to buy, that’s not what you want to see. But it has happened. And here’s why.

Uncertainty is the enemy of mortgage rates.

And with lingering global uncertainty, ongoing tensions in the Middle East, and inflation refusing to fully cool off, there’s a lot that’s having an effect on rates. Colin Robertson, Founder of The Truth About Mortgage, put it plainly:

"You can't have $100 a barrel oil and not expect inflation to rise, which translates to higher bond yields and mortgage rates."

Take a look at the graph below. It uses data from Mortgage News Daily to show just how much all of those factors have had an impact:

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it's probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It’s a pretty sharp contrast from where we’ve been, in a relatively short window. And it's probably making you wonder: Should I just wait this out? Will rates fall when the uncertainty eases?

It's possible. But it all depends on how the ongoing geopolitical conflict plays out and whether inflation continues to run hot afterwards – and for how long.

Rates probably aren't heading down until both of those things improve. And even when that does happen, experts agree rates likely won’t be dramatically lower – maybe in the low to mid-6s. That's the reality, and it's worth knowing.

So, should you wait for lower rates? The general consensus is, if you can afford to buy and you find a home you like, it’s still worth it. Because no one knows for sure when rates will start to come back down – and how long do you really want to put your life on hold?

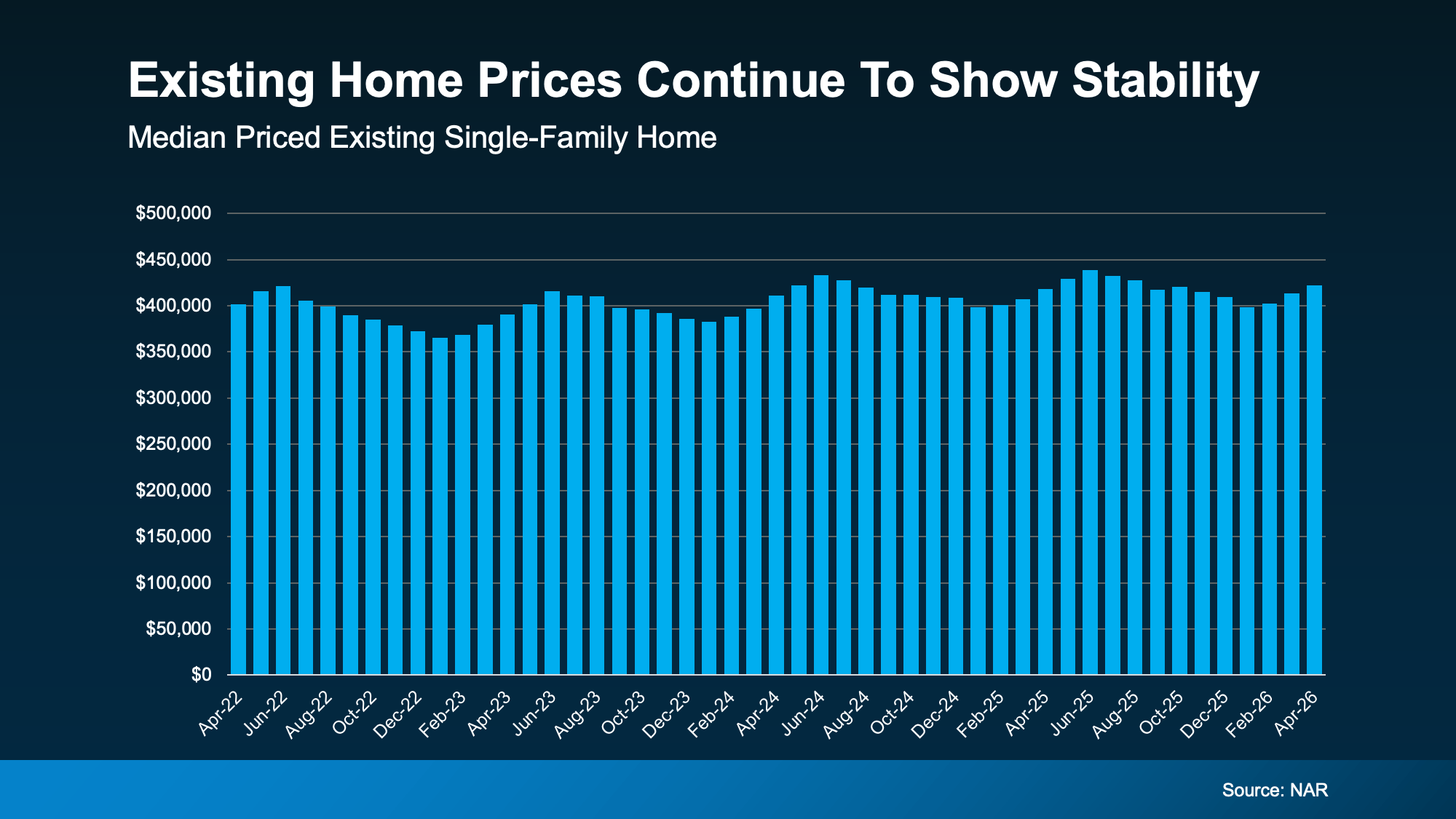

You've probably heard that inflation is making everything more expensive, and there's no shortage of headlines about the cost-of-living outpacing paychecks. It's a legitimate concern. And maybe you’re feeling the pinch yourself. But here's what doesn't make the headlines. It's not all bad news.

Data from the Federal Reserve Bank of Atlanta and Redfin shows wages have actually been growing faster than home prices.

Recently, wages have been increasing at around 4% year-over-year.

And home price growth is closer to 2% year-over-year.

As a buyer, you want your income to rise faster than prices because that helps make your purchase more manageable financially, and it quietly chips away at the affordability challenge over time. That’s exactly what we’re seeing lately. And every little bit is going to help.

A big reason wages have been gaining ground on home prices? Home prices have actually stayed pretty steady.

Check out the graph below. It shows home price data from the National Association of Realtors (NAR) over the past 4 years. Notice anything? There's been no dramatic runup, and no crash either. Just relative stability and slow growth:

Part of what's keeping prices this stable is that buyers finally have more choices. That means less competition, more negotiating power, and more time to find the home that actually fits your life, not just the one you had to grab before someone else did.

And that gives you a chance to hopefully find something that works for your budget, even with today’s rates. At the same time, you're not losing ground pricewise while you take time to make a careful decision.

Yes, rates have been volatile, and global instability is keeping them from settling down anytime soon. There’s no sugar coating that. But the full picture of affordability is more nuanced than the headlines suggest.

Want to run the real numbers for your situation? Let's talk. Reach out and let's set up a quick, no-pressure conversation.

You may be telling yourself you’re going to wait to move – maybe you’re hoping mortgage rates will come down, prices will fall, or the market will feel a little easier.

And honestly? A lot of people feel that way right now. But here’s what some are starting to realize.

Waiting doesn’t usually fix the thing that made you want to move in the first place.

Your family still desperately needs more room. Your empty nest still feels too...empty.

Your parents or grandparents still need you to live closer.

You just got married... or divorced.

Your vision of retirement has you living somewhere else.

Eventually, life can reach a point where waiting feels harder than moving.

That’s why some people are still deciding to buy right now, even in today’s market. Not because conditions are perfect. But because the life changes behind their move never really went away.

And maybe that’s exactly where you are too. If so, you’re certainly not alone.

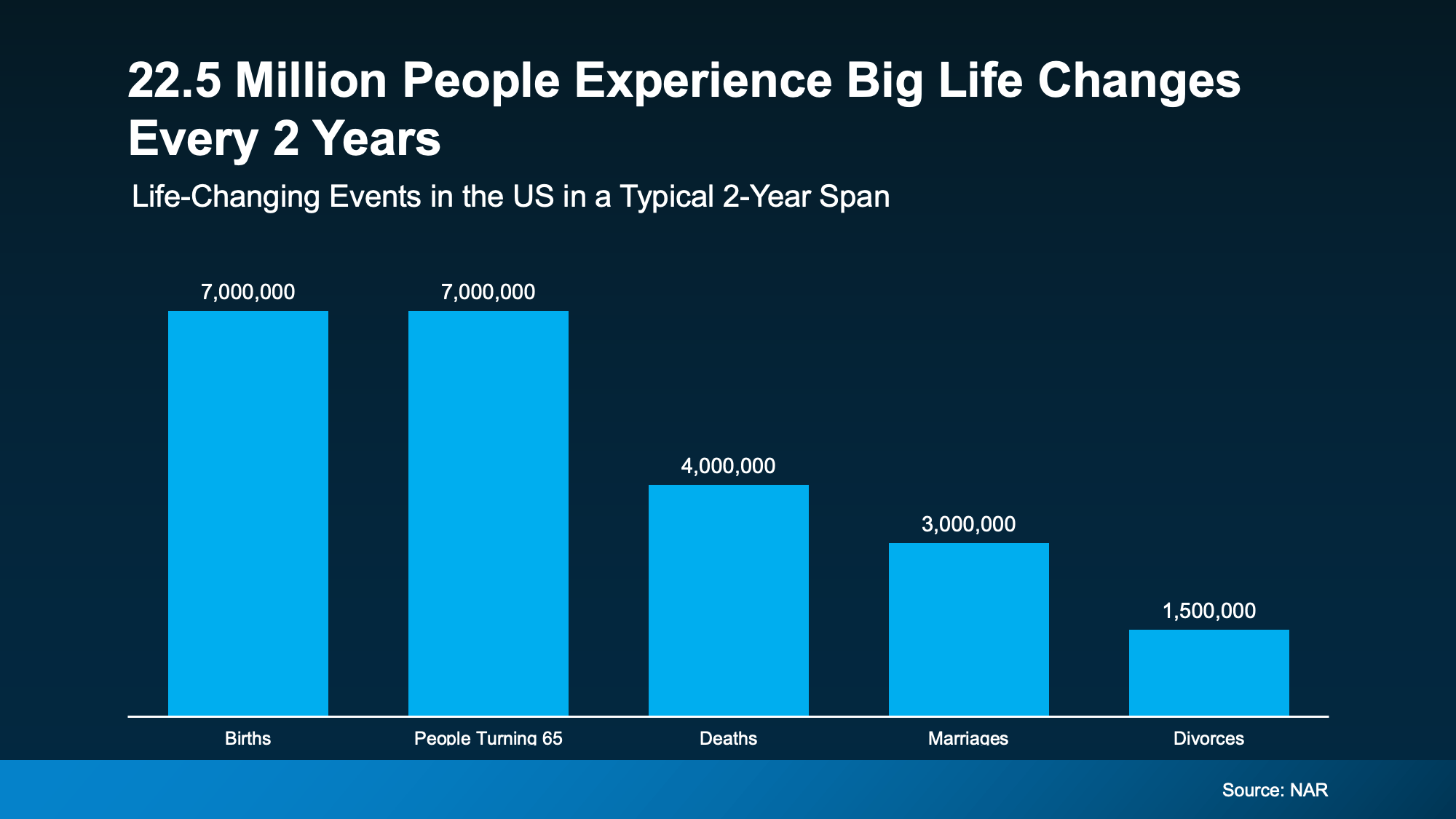

Data from the National Association of Realtors (NAR) shows 1 in 5 buyers last year said they felt like they had to purchase a home at that time, no matter the market.

That's an important reminder right now. Sure, the dollars and cents of your move have to make sense for you. But big life changes happen whether mortgage rates and home prices are high, low, or somewhere in between.

And those big life events happen more than you may think. NAR says roughly 22.5 million people experience major life changes in a typical two-year span (see graph below):

These are exactly the kinds of things that can change how much space you need, where you want to live, or what kind of lifestyle makes sense now. Chen Zhao, Head of Economics Research at Redfin, explains:

“Life doesn’t stand still—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood.”

And that’s what makes waiting so hard. Every month you spend hoping the market changes is another month living in a house that no longer works for your life. It’s stressful to feel stuck. And that feeling usually doesn’t disappear.

But while affordability is still a challenge, there may still be a way for you to make your move.

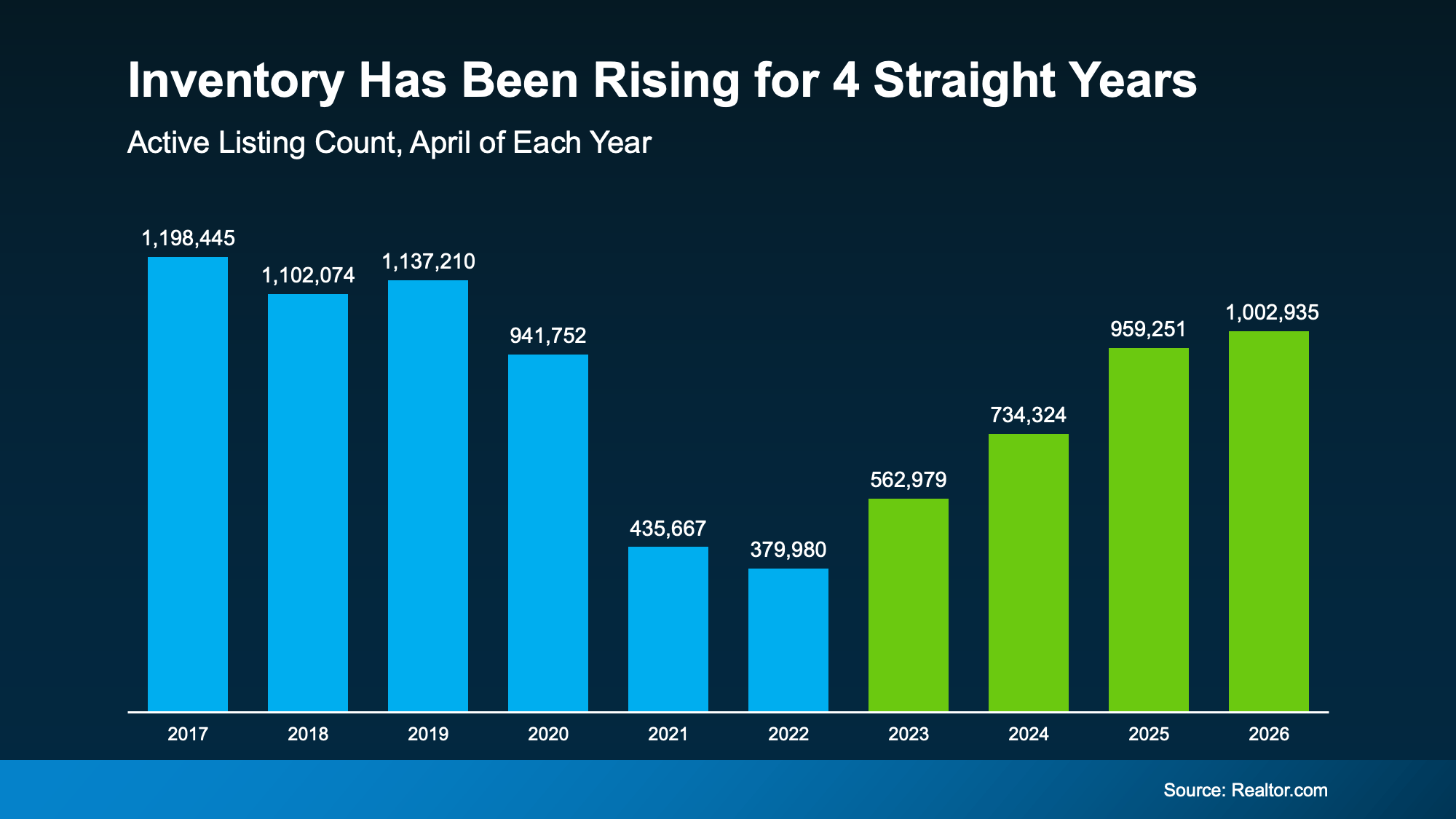

The number of homes for sale has been growing for 4 straight years (see graph below). That means more homes to choose from and, in some markets, more room to negotiate than buyers had just a few years ago.

That doesn’t mean moving is suddenly easy. But it does mean some buyers are finding ways to make a move work. So, if you’ve been putting your plans on hold, maybe the question isn’t just:

“What’s the market doing?” or “When will it get better?”

Maybe ask yourself this, too: “Can I still live where I'm at right now and make it work?”

If the answer to that second question is “no,” it may be worth having a conversation about what your options look like today – despite where rates or prices are. You could find your move is still possible after all. With more homes for sale, there’s a better chance to find one that fits your life (and your budget) right now.

Life changes. Priorities shift. Families grow. Kids move out. Careers evolve. And eventually, the house you’re in may stop fitting the life you’re living.

If that’s been weighing on you lately, let’s talk through what your options could realistically look like today, no matter where rates or prices are.

Life can’t always wait for perfect market conditions. Maybe you don’t have to either.

The highly anticipated Timberline Gondola was officially cancelled today. The Forest Service project page confirms the cancelation.

After a low snow winter and escalating insurance premiums, Timberline can't catch a break! The mountain will be closing for summer skiing around mid July cutting things short by weeks. Many ski camps didn't come this year for lack of snow pack.

The local mountain economy is and will be suffering with all of this news. Please support our local businesses.

Displaying blog entries 1-10 of 1996