Firewood Season is Now Open on Mt. Hood National Forest

Firewood season now open on Mt. Hood National Forest

Free personal use permit required to collect up to six cords

SANDY, Ore. — Personal use firewood permits are now available for the season on Mt. Hood National Forest.

All woodcutters must obtain a firewood permit to cut and haul firewood from the Forest. Permits are available at a district office or by submitting a firewood permit application. Each household may collect a maximum of six cords annually with a free firewood permit for personal use only. Permits are valid through November 30.

Woodcutters who need more than six cords of firewood or intend to collect firewood for resale must purchase a commercial firewood permit, which is available upon request pending availability.

All woodcutters must carry their permit, firewood load tags, firewood map, and a current information sheet while harvesting. Woodcutters may only collect and cut downed wood. Felling standing trees, dead or alive, is illegal. Firewood cutting areas are described on the required firewood maps and information sheets, which are updated regularly and reflect the current Industrial Fire Precaution Level of each area.

More firewood information is available online: www.fs.usda.gov/r06/mthood/permits/firewood

Conditions across Mt. Hood National Forest vary and may change rapidly. Some Forest Service roads may be snow-covered, icy, or muddy. Several roads remain impassable due to downed trees, landslides, culvert blockages, and other damage caused by December’s significant storms. Vehicle access to some areas may be limited due to wildfire closures. Always know before you go: www.fs.usda.gov/r06/mthood/alerts

Contact a district office for information on current conditions: www.fs.usda.gov/r06/mthood/offices

Some community members who rely on firewood to heat their home may struggle to harvest firewood due to age or physical disabilities. Learn more about Mt. Hood National Forest’s firewood assistance program and how to apply: www.fs.usda.gov/media/158825

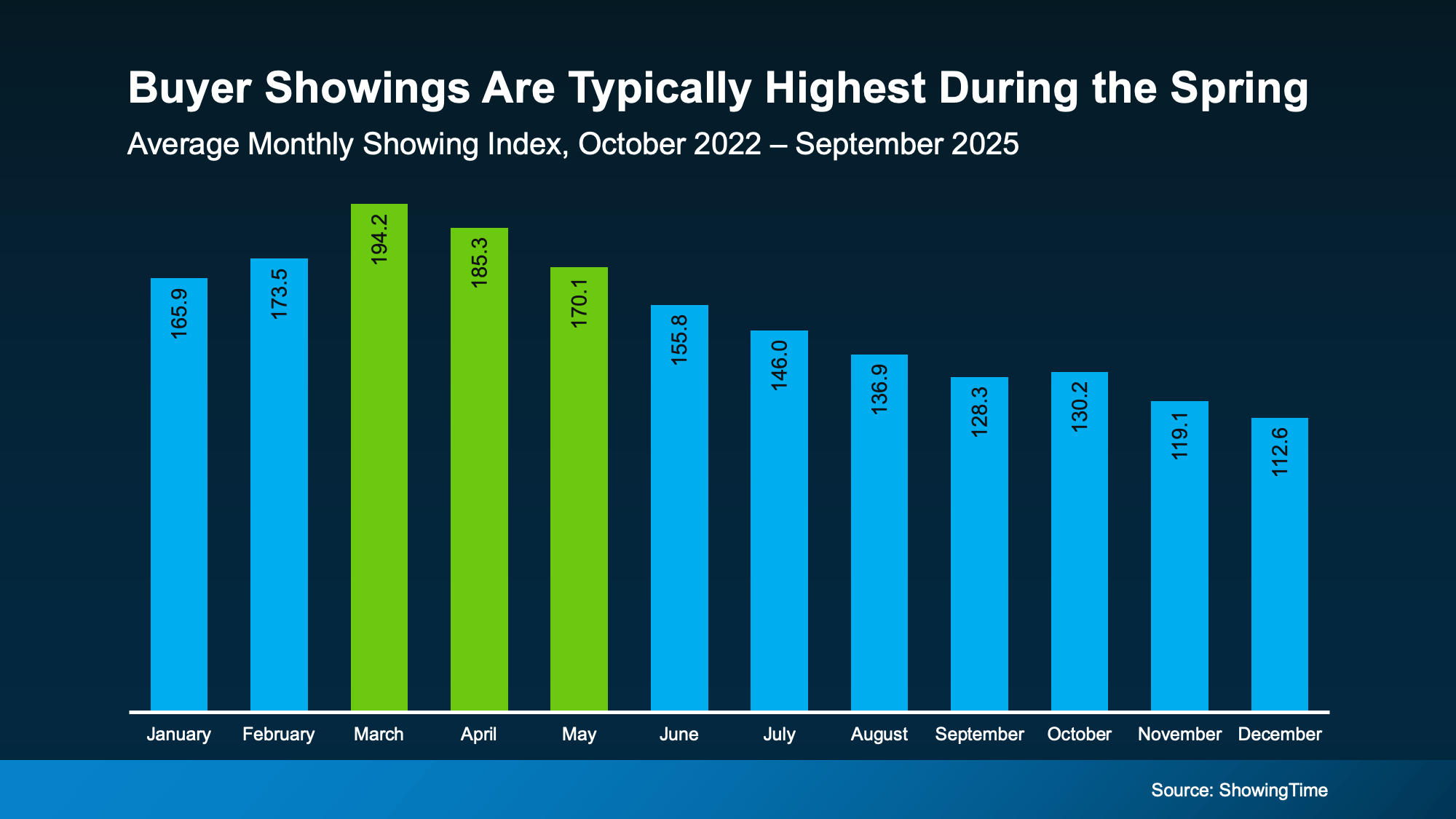

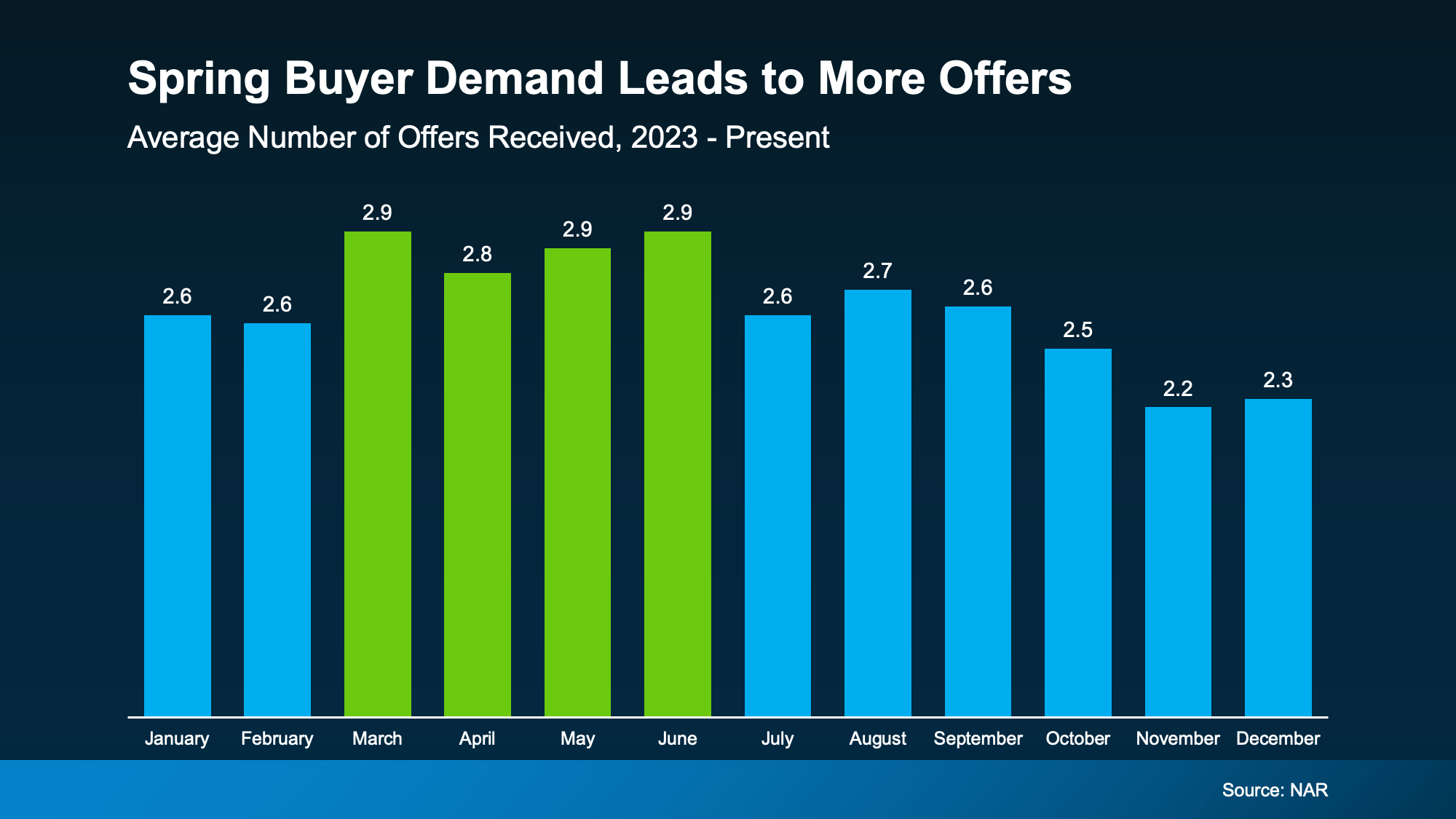

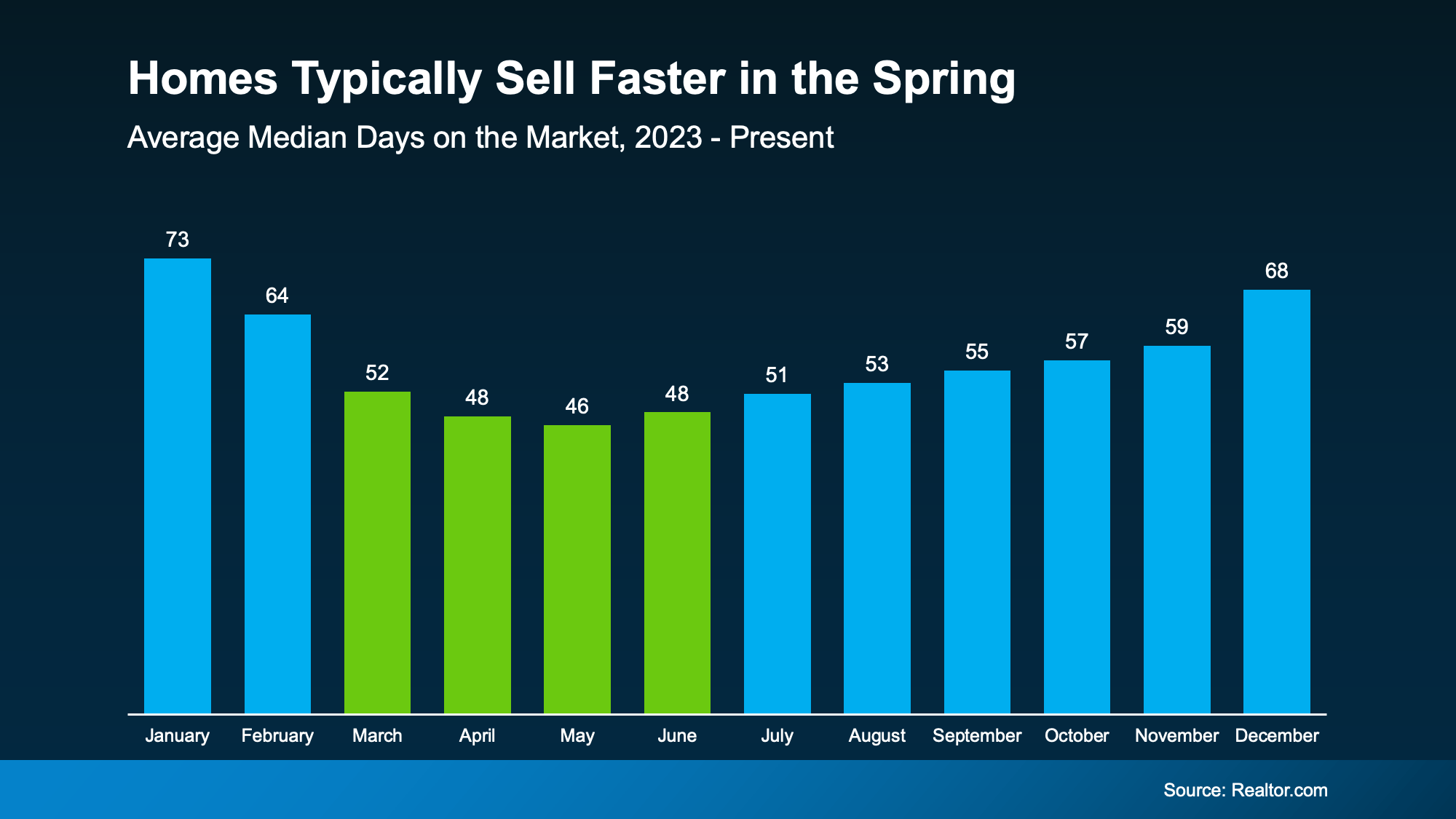

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that's a difference you can feel.

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that's a difference you can feel.