Here’s to a Wonderful 2022!

Friday, December 31, 2021

Displaying blog entries 51-60 of 64

There are a lot of questions right now regarding the real estate market as we head into 2022. The forbearance program is coming to an end and mortgage rates are beginning to rise.

With all of this uncertainty, anyone with a megaphone – from the mainstream media to a lone blogger – has realized that bad news sells. Unfortunately, we’ll continue to see a rash of troublesome headlines over the next few months. To make sure you aren’t paralyzed by a headline, turn to reliable resources for a look at what to expect from the housing market next year.

There are already alarmist headlines starting to appear. Here are two recent topics you may have seen in the news.

There are a number of headlines circulating that call out the rising foreclosures in today’s real estate market. Those stories focus on an overly narrow view on that topic: the current volume of foreclosures compared to 2020. They emphasize that we’re seeing far more foreclosures this year compared to last.

That seems rather daunting. However, though it’s true foreclosures have been up over the 2020 numbers, it’s important to realize that there were virtually no foreclosures last year because of the forbearance plan. If we compare this September to September of 2019 (the last normal year), foreclosures were down 70% according to ATTOM.

Even Rick Sharga, an Executive Vice President of the firm that issued the report referenced in the above article, says:

“As expected, now that the moratorium has been over for three months, foreclosure activity continues to increase. But it's increasing at a slower rate, and it appears that most of the activity is primarily on vacant and abandoned properties, or loans in foreclosure prior to the pandemic.”

Homeowners who have been impacted by the pandemic are not generally the ones being burdened right now. That’s because the forbearance program has worked. Ali Haralson, President of Auction.com, explains that the program has done a remarkable job:

“The tsunami of foreclosures many feared in the early days of the pandemic has not materialized thanks in large part to the swift and decisive foreclosure protections put in place by government policymakers and the mortgage servicing industry.”

And the government is still making sure homeowners have every opportunity to stay in their homes. Rohit Chopra, the Director of the Consumer Financial Protection Bureau (CFPB), issued this statement just last week:

“Failures by mortgage servicers and regulators worsened the impact of the economic crisis a decade ago. Regulators have learned their lesson, and we will be scrutinizing servicers to ensure they are doing all they can to help homeowners and follow the law.”

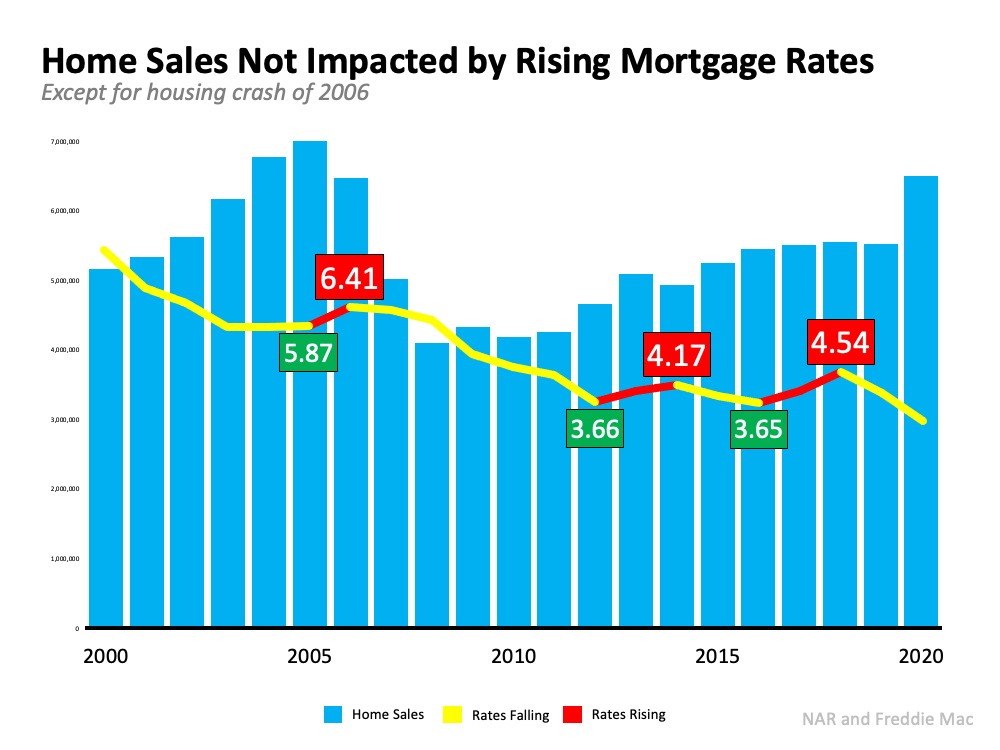

Another topic that’s generating frequent headlines is the rise in mortgage rates. Some people are expressing concern that rising rates will negatively impact the housing market by causing home sales to dramatically decline. The resulting headlines are raising unneeded alarm bells. To counteract those headlines, we need to take a look at what history tells us. Looking at data over the last 20 years, there’s no evidence that an increase in rates dramatically forces sales to come to a halt. Nor does home price appreciation come to a screeching stop. Let’s look at home sales first: The last three times rates increased (shown in the graph above in red), sales (depicted in blue in the graph) remained rather consistent. It’s true that sales fell rather dramatically from 2007 through 2010, but mortgage rates were also falling at the time. The next two instances showed no meaningful drop in sales.

The last three times rates increased (shown in the graph above in red), sales (depicted in blue in the graph) remained rather consistent. It’s true that sales fell rather dramatically from 2007 through 2010, but mortgage rates were also falling at the time. The next two instances showed no meaningful drop in sales.

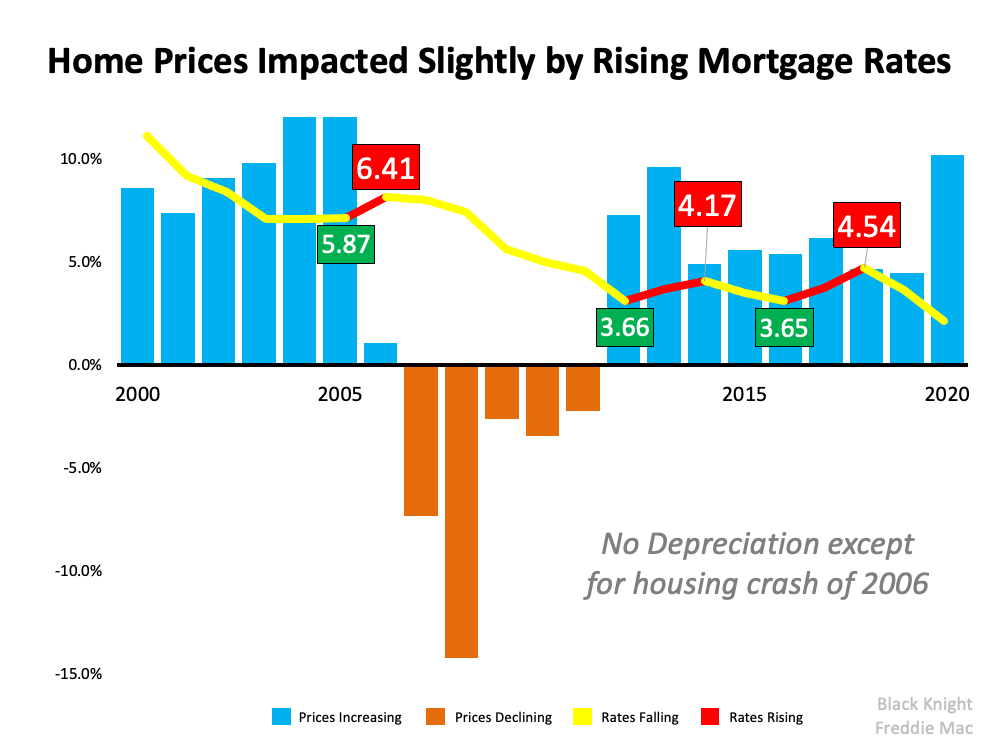

Now, let’s take a look at home price appreciation (see graph below): Again, we see that a rise in rates didn’t cause prices to depreciate. Outside of the years following the crash, prices continued to appreciate, just at a slower rate.

Again, we see that a rise in rates didn’t cause prices to depreciate. Outside of the years following the crash, prices continued to appreciate, just at a slower rate.

There’s a lot of misinformation out there. If you want the best advice on what’s happening in the current housing market, let’s connect.

With home prices continuing to deliver double-digit increases, some are concerned we’re in a housing bubble like the one in 2006. However, a closer look at the market data indicates this is nothing like 2006 for three major reasons.

Back in 2006, nearly everyone could qualify for a loan. The Mortgage Credit Availability Index (MCAI) from the Mortgage Bankers’ Association is an indicator of the availability of mortgage money. The higher the index, the easier it is to obtain a mortgage. The MCAI more than doubled from 2004 (378) to 2006 (869). Today, the index stands at 130. As an example of the difference between today and 2006, let’s look at the volume of mortgages that originated when a buyer had less than a 620 credit score. Dr. Frank Nothaft, Chief Economist for CoreLogic, reiterates this point:

Dr. Frank Nothaft, Chief Economist for CoreLogic, reiterates this point:

“There are marked differences in today’s run up in prices compared to 2005, which was a bubble fueled by risky loans and lenient underwriting. Today, loans with high-risk features are absent and mortgage underwriting is prudent.”

During the housing bubble, as prices skyrocketed, people were refinancing their homes and pulling out large sums of cash. As prices began to fall, that caused many to spiral into a negative equity situation (where their mortgage was higher than the value of the house).

Today, homeowners are letting their equity build. Tappable equity is the amount available for homeowners to access before hitting a maximum 80% combined loan-to-value ratio (thus still leaving them with at least 20% equity). In 2006, that number was $4.6 billion. Today, that number stands at over $8 billion.

Yet, the percentage of cash-out refinances (where the homeowner takes out at least 5% more than their original mortgage amount) is half of what it was in 2006.

FOMO (the Fear Of Missing Out) dominated the housing market leading up to the 2006 housing bubble and drove up buyer demand. Back then, housing supply more than kept up as many homeowners put their houses on the market, as evidenced by the over seven months’ supply of existing housing inventory available for sale in 2006. Today, that number is barely two months.

Builders also overbuilt during the bubble but pulled back significantly over the next decade. Sam Khater, VP and Chief Economist, Economic & Housing Research at Freddie Mac, explains that pullback is the major factor in the lack of available inventory today:

“The main driver of the housing shortfall has been the long-term decline in the construction of single-family homes.”

Here’s a chart that quantifies Khater’s remarks: Today, there are simply not enough homes to keep up with current demand.

Today, there are simply not enough homes to keep up with current demand.

This market is nothing like the run-up to 2006. Bill McBride, the author of the prestigious Calculated Risk blog, predicted the last housing bubble and crash. This is what he has to say about today’s housing market:

“It’s not clear at all to me that things are going to slow down significantly in the near future. In 2005, I had a strong sense that the hot market would turn and that, when it turned, things would get very ugly. Today, I don’t have that sense at all, because all of the fundamentals are there. Demand will be high for a while because Millennials need houses. Prices will keep rising for a while because inventory is so low.”

Here is the latest update on vacation rental study by Clackamas County:

Good afternoon,

After months of delay because of the COVID-19 pandemic and the wildfires, the Clackamas County Board of Commissioners has scheduled a policy session on short-term rental regulations for 3 p.m., Tuesday, Oct. 13, to review the major points of the draft regulations and set public hearings. The tentative plan is to hold public hearings and have the Board take action before the end of 2020, with any new regulations going into effect on July 1, 2021.

More details are in the staff report for the meeting. You can connect to the Zoom meeting to observe and see the staff report athttps://www.clackamas.us/meetings/bcc/presentation/2020-10-13-1.

As you may remember, the draft regulations were first created in 2019 at the request of the Board of Commissioners, in response to the increasing number of residents who use their homes for short-term or vacation rentals. The regulations include provisions for short-term rental owners to register with the county and pay a fee, and for enforcement of the regulations to be carried out by either the Sheriff’s Office or Code Enforcement, depending on the issue.

Clackamas County defines a short-term rental, or vacation rental, as a dwelling unit, or portion of a dwelling unit, that is rented to any person or entity for lodging or residential purposes, for a period of up to 30 consecutive nights.

Key components of the proposed regulations include rules regarding maximum occupancy, off-street parking, garbage pick-up, quiet hours, and fire and safety requirements. All short-term rentals would be subject to the same regulations, except that short-term rental properties inside the Portland metropolitan urban growth boundary would be required to be the owner’s primary residence or located on the same tract as the owner's primary residence. (The owner would not be required to be there when the short-term rental was occupied.) Details are available online at www.clackamas.us/planning/str.

For more information, contact Principal Planner Martha Fritzie at [email protected] or 503-742-4529.

You received this email because you have expressed an interest in regulations for short-term rentals in unincorporated Clackamas County. If you no longer wish to receive these emails, please let me know. Thank you.

Ellen Rogalin, Community Relations Specialist

Clackamas County Public & Government Affairs

Transportation & Development | Business & Community Services

503-742-4274 | 150 Beavercreek Road, Oregon City, OR 97045

Office hours: 9 am – 6 pm, Monday-Friday

Every year around this time, many homeowners begin the process of preparing their homes in case of extreme winter weather. Some others skip winter all together by escaping to their vacation homes in a warmer climate.

For those homeowners staying at their first residence, AccuWeather warns:

“The late-week cold shot should fade next week, but this is a warning shot for winter's return late in the month and early February."

Given this, it’s time to go and stock up on winter weather supplies! However, if you’re tired of shoveling snow and dealing with the cold weather, maybe it’s time to consider obtaining a vacation home!

According to the Investment & Vacation Home Buyers 2018 Report by NAR:

“72% of vacation property owners and 71% of investment property owners believe now is a good time to buy.”

It’s time to take advantage of the equity in your home. As the latest Equity Report from ATTOM Data Solutions stated:

“Nearly 14.5 million U.S. properties (are) equity rich — where the combined estimated amount of loans secured by the property was 50 percent or less of the property’s estimated market value — up by more than 433,000 from a year ago to a new high as far back as data is available, Q4 2013.

The 14.5 million equity rich properties in Q3 2018 represented 25.7 percent of all properties with a mortgage.”

This means that over a quarter of Americans who have a mortgage would be able to use some of their home equity to make a significant down payment toward a vacation home, and many are doing just that! According to the same report by NAR:

“33% of vacation buyers purchased in a beach area, 21% purchased on a lakefront, and 15% purchased a vacation home in the country.”

We have everything from Government Camp ski condos to rustic cabins in the woods dotting the Mt. Hood National Forest. Our supply stretches from Brightwood, Welches, and Rhododendron to Government Camp!

Many homeowners who are close to retirement will use some of their equity to purchase vacation homes, which may eventually become their permanent homes post-retirement!

If you are a homeowner looking to take advantage of your home equity by investing in a vacation home, let’s get together to discuss your options!

Displaying blog entries 51-60 of 64