Many Mt. Hood Owners Delisted and Are Now Re-Listing

Tuesday, March 24, 2026

Add Comment

Displaying blog entries 31-40 of 1996

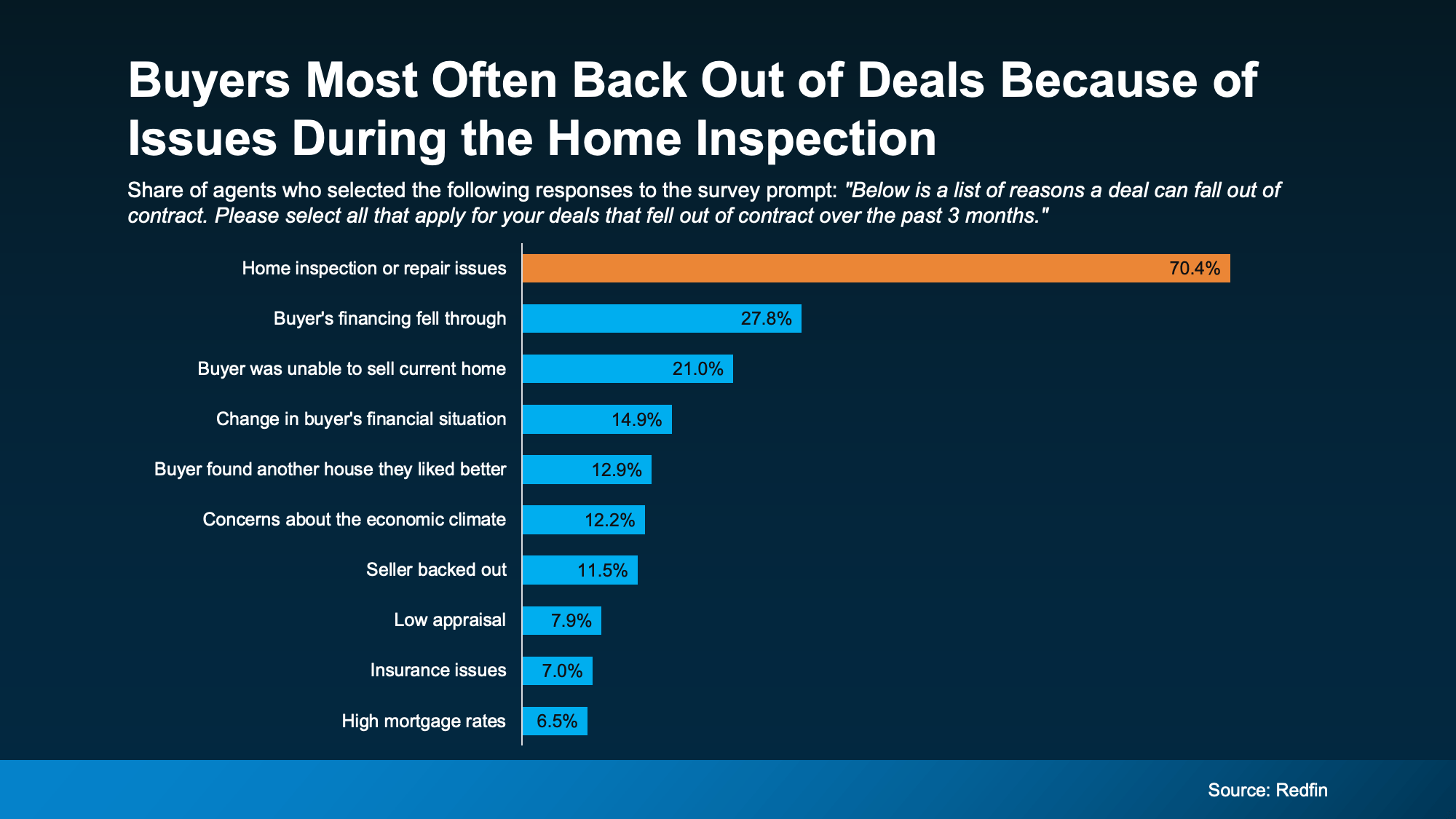

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They'll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

But remember, you don't have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, let's connect so we can keep your sale on track from day one.

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They'll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

But remember, you don't have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, let's connect so we can keep your sale on track from day one.

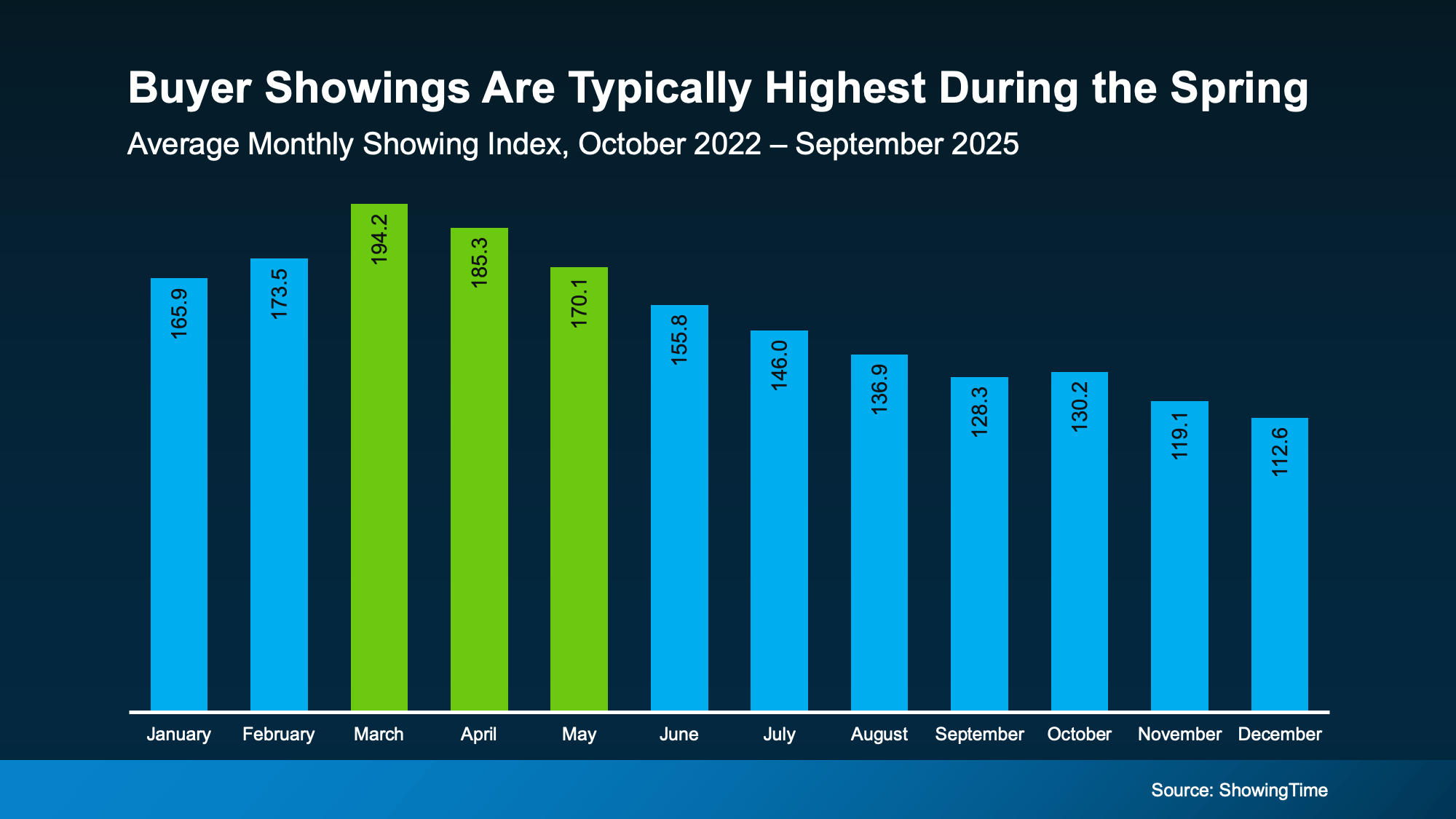

Homeowners looking to sell usually want three things: plenty of interested buyers, strong offers, and a short timeline. Spring is the season that most often delivers all three.

So, if a move has been on your mind this year, this is the window where momentum tends to work in your favor. Here’s what makes this season so powerful for sellers.

Typically speaking, in the housing market, there’s no more popular time to move than the Spring. Historically, data coming out of ShowingTime proves that’s when buyer activity peaks each year. Take a look for yourself (see graph below):

And this year, there’s more than just the seasonal trend working in your favor. Mortgage rates are also sitting near 3-year lows – and that combination matters.

And this year, there’s more than just the seasonal trend working in your favor. Mortgage rates are also sitting near 3-year lows – and that combination matters.

More buyers + improving affordability = more eyes on your house.

That doesn’t mean the market will return to the frenzy of the pandemic – far from it. But it does mean more buyers will be ready to re-enter the market. And that’s good for you. As Redfin says:

“Homebuying demand is improving . . . and mortgage-purchase applications are sitting near their highest level in three years. . ."

You should make sure your house is listed so you can take advantage of the uptick in demand. Because more activity means one thing: more opportunity to get a deal done.

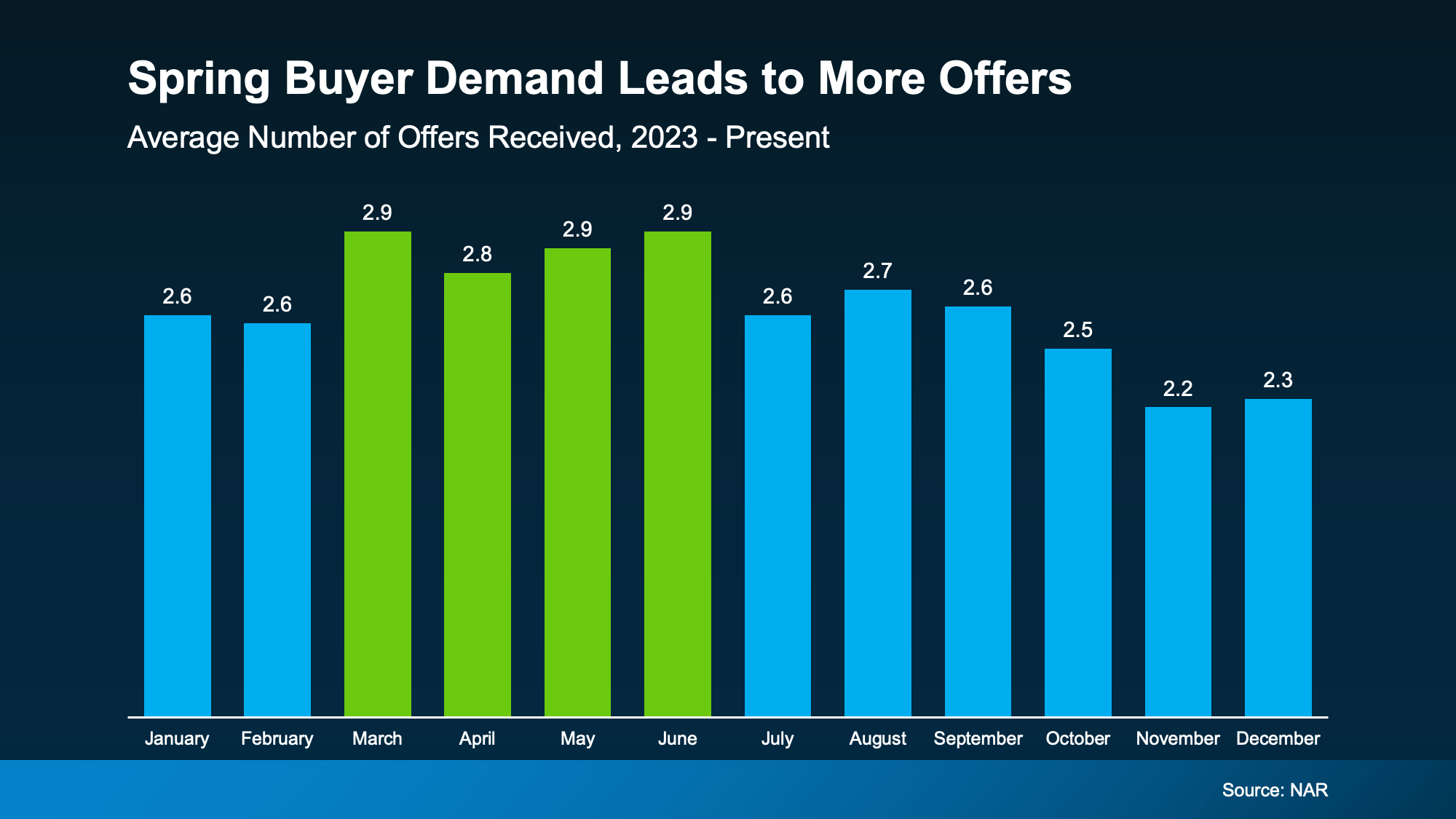

With more buyer demand, it makes sense that you may get more offers on your house. And history shows that’s usually true.

If we look at the data for the last three years from the National Association of Realtors (NAR), and take the averages for each month, it’s clear sellers in the Spring get more offers (see graph below):

Now, don’t expect the excessive bidding wars that were so famous in 2020 and 2021. But it does mean, seasonality could help you out this Spring. As Realtor.com explains:

Now, don’t expect the excessive bidding wars that were so famous in 2020 and 2021. But it does mean, seasonality could help you out this Spring. As Realtor.com explains:

“Spring typically brings out more buyers who are ready to make a move before summer. Listings see more views, showings, and offers during this season.”

And that could be really good for your bottom line.

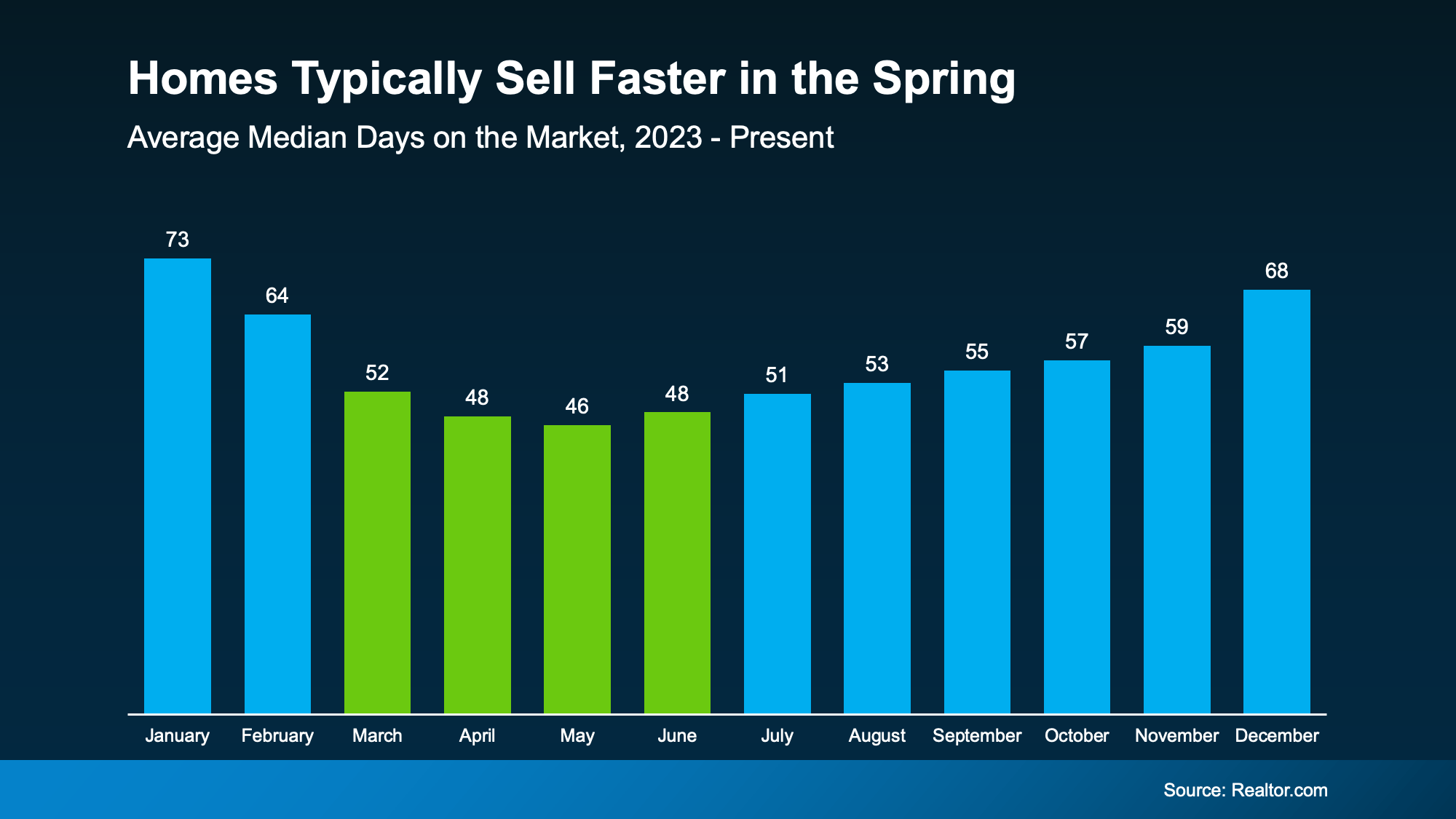

There’s one more predictable pattern that happens pretty much every Spring based on research from Realtor.com. Homes sell faster (see graph below):

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that's a difference you can feel.

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that's a difference you can feel.

Since homes have been taking longer to sell lately, listing your house during what’s usually the most active time of the year means you’re setting yourself up to move as quickly as possible. And isn’t that what sellers really want?

The faster your home sells, the earlier you can move on to what’s next for you.

If you’re eager to go on to your next chapter, need to downsize, or you’ve run out of space, Spring may be your best time to sell.

Spring doesn’t guarantee a sale. Strategy still matters. But this season gives you something valuable: momentum.

More buyers. More activity. More opportunity.

The real question is: if you’re going to sell this year, why not do it when the odds are in your favor?

Let’s talk about what selling this season could mean for your house and your timeline.

You’ve probably seen posts on social media talking about how “home prices are falling.” And when you see something like that, it’s normal to wonder:

Is this the start of a crash?

What does this mean for my house?

Let’s clear this up right away. This is not a crash. And your home is not suddenly losing a lot of value.

Here’s what often gets left out of what you’re seeing online. While some markets are experiencing slight declines, they’re the minority. Most places are still seeing prices rise or at the very least, hold steady.

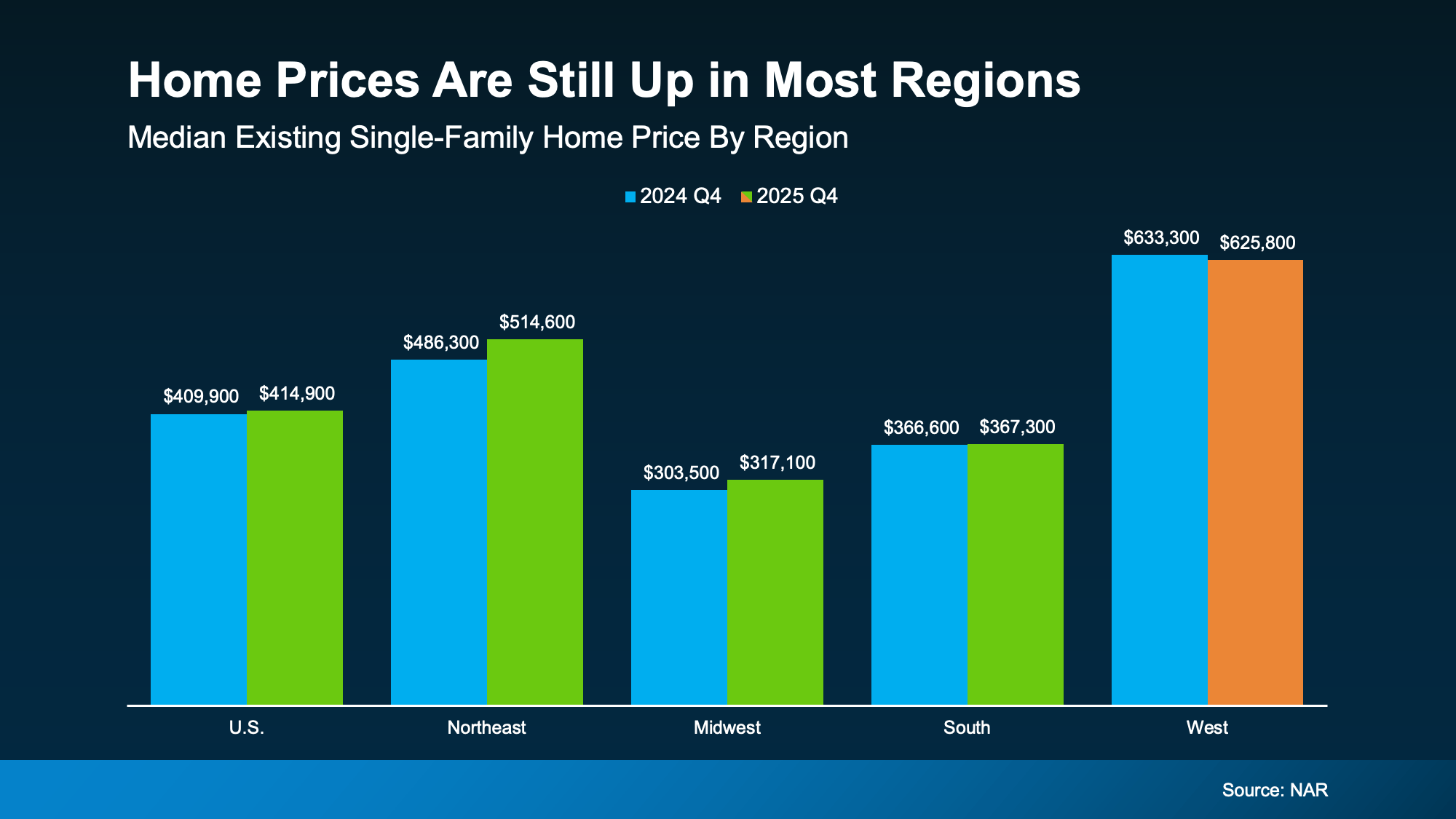

That’s why, at the national level, home prices are still rising, just at a slower pace. According to the National Association of Realtors (NAR):

“Home prices continued to rise in the fourth quarter of 2025. National median prices rose 1.2% year over year to $414,900.”

That’s not the rapid growth of a few years ago, but it’s not a downturn either. And just to really drive this home, here’s a look at the data from NAR at a regional level, so you can see that the negative narrative spun up online isn’t the whole truth (see graph below):

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

There is no wave of falling prices across the country. Instead, there are just a few pockets adjusting after several years of what’s typically considered unsustainable or exponential growth.

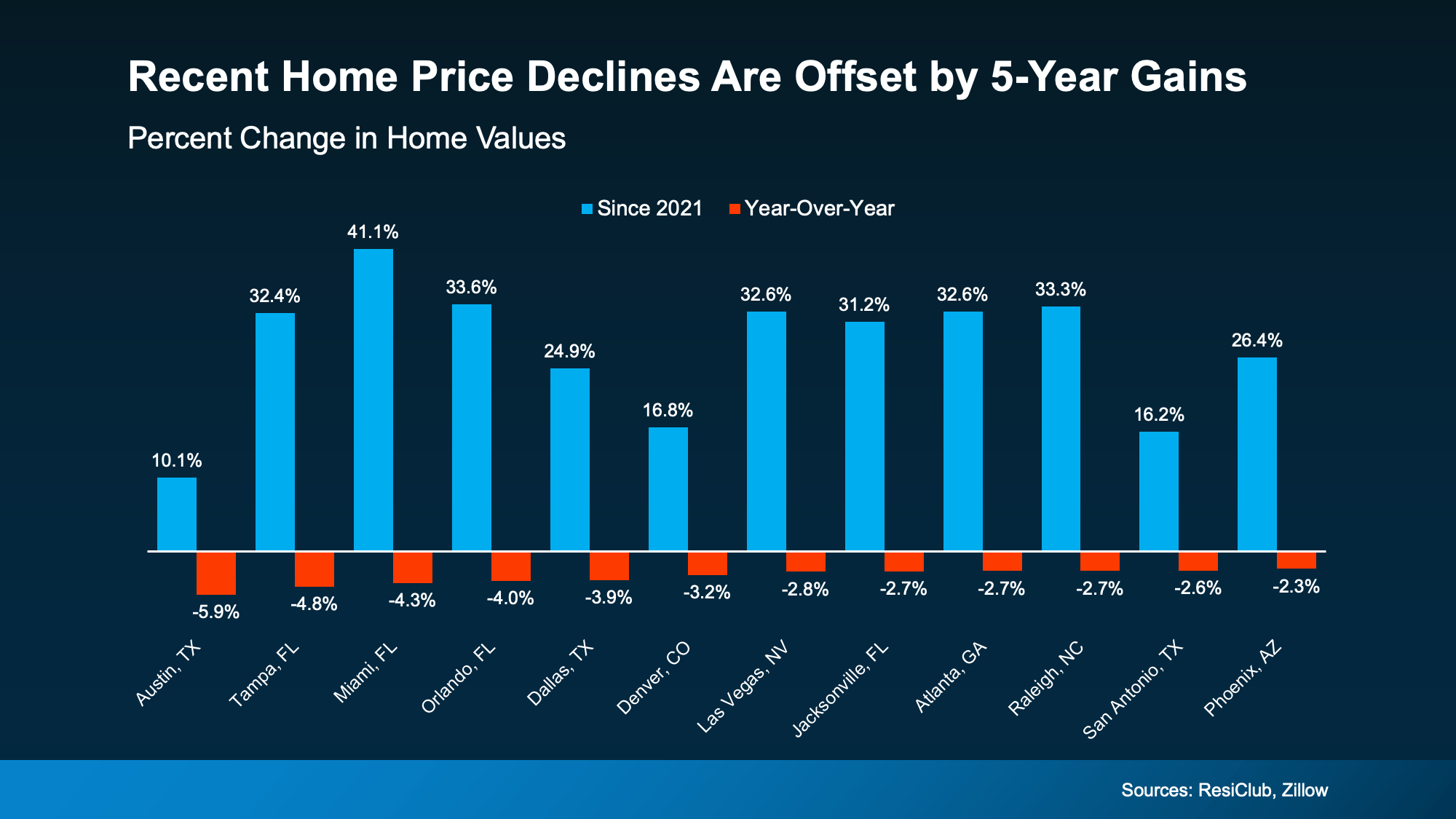

Okay, but what about the places where prices have declined? According to ResiClub and Zillow, that’s not a cause for major concern. When you zoom out and look at those same markets over the past five years, the story changes (see graph below):

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

Online chatter tends to shine a spotlight on the few areas that are down. But the bigger picture shows most homeowners are still in a very strong position.

Of course, every market, and every home, is different. But broadly speaking, home values are holding steady. And this isn’t a sign of widespread trouble in the market.

Despite what you may be seeing online, home prices are rising or holding steady in most parts of the country.

If you’re curious what your home is worth today, let’s take a look at the numbers together. Because context, and local expertise, matter more than what you’re seeing online.

There’s one number that decides how your sale goes before buyers ever step inside your home – and that’s your asking price.

Set it too high, and your house sits while buyers scroll past it.

But set it too low and you’ll leave real money on the table.

Here’s the problem. A lot of homeowners are basing their number on an online home value tool. And that’s where things can go sideways.

There’s one decision you're going to make when you sell that determines whether your house sells quickly, or it sits. Whether buyers make an offer, or scroll past it. Whether you walk away with the maximum return, or you end up cutting the price later.

And that’s your asking price.

If you’re thinking of moving and trying to figure out what your house may sell for, it’s tempting to start with an online home value tool. They’re fast, free, and easy. And you don’t have to talk to anyone. But here’s the problem: they don’t know your house.

And that can be a bigger drawback than you realize.

Online tools often lag behind the market. They look in the rearview mirror, relying on closed sales and delayed information. And in that sense, they’re using incomplete data.

That’s not a miss in how these systems are built. Some information just isn’t available online. Bankrate explains:

“While these tools can be a useful starting point, keep in mind that they typically do not provide the most accurate pricing. Algorithms can only rely on the information available; they can’t account for things like a home’s condition or renovations made since the last public information was updated.”

They can’t see:

So, while they may do a good job in some cases, they can’t be as accurate as a local agent who has boots on the ground day in and day out.

In a market where buyers have more options, a seemingly small margin of error can cost you thousands if you price too low, or weeks of lost momentum and time if you price too high.

If you want to sell for the most money and in the least amount of time, you don’t want the fast answer on how to price your house. You want the right one.

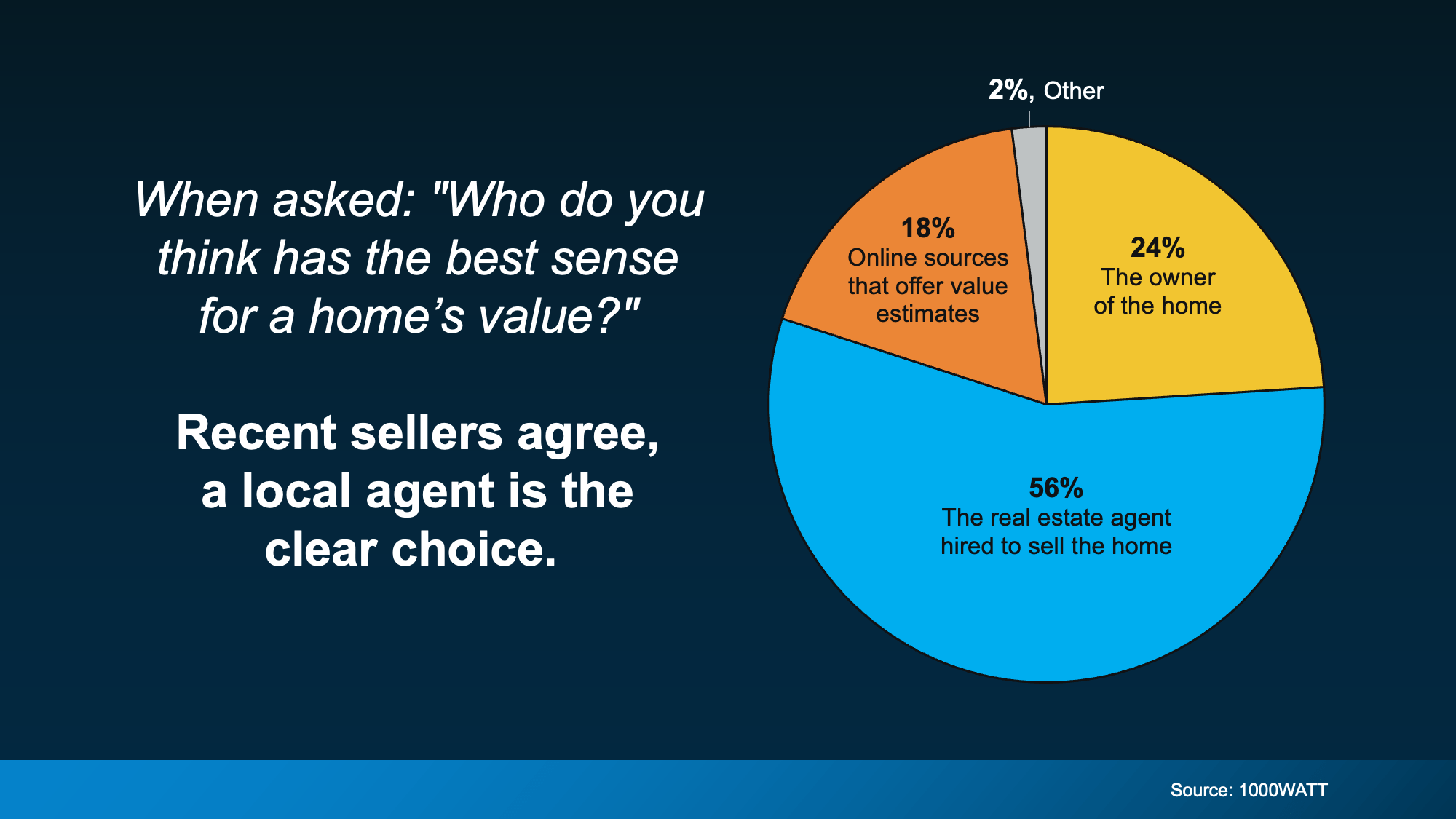

That’s why the savviest homeowners today don’t rely on algorithms when it actually matters. They rely on people, specifically trusted local agents.

According to 1000WATT, sellers overwhelmingly believe real estate agents have the best sense of a home’s true value, far more than any automated tools.

That confidence isn’t accidental. As Bankrate puts it:

That confidence isn’t accidental. As Bankrate puts it:

“A professional appraiser or real estate agent can visit the home in person, assess the neighborhood as a whole as well as the individual property, perform more thorough market research, and consider subjective details.”

And those details matter. A skilled local agent doesn’t just pull reports. They know what’s happening right now:

And once an agent steps foot in your house, they may even find your online estimate undershot your value. So, if you stuck with the estimate you got online, you’d actually be leaving money on the table. And no one wants that.

While online tools can give you a rough starting point, only a local expert can give you a price that actually works.

If you want to know the right number for your house, not just the easiest one to find, let’s talk.

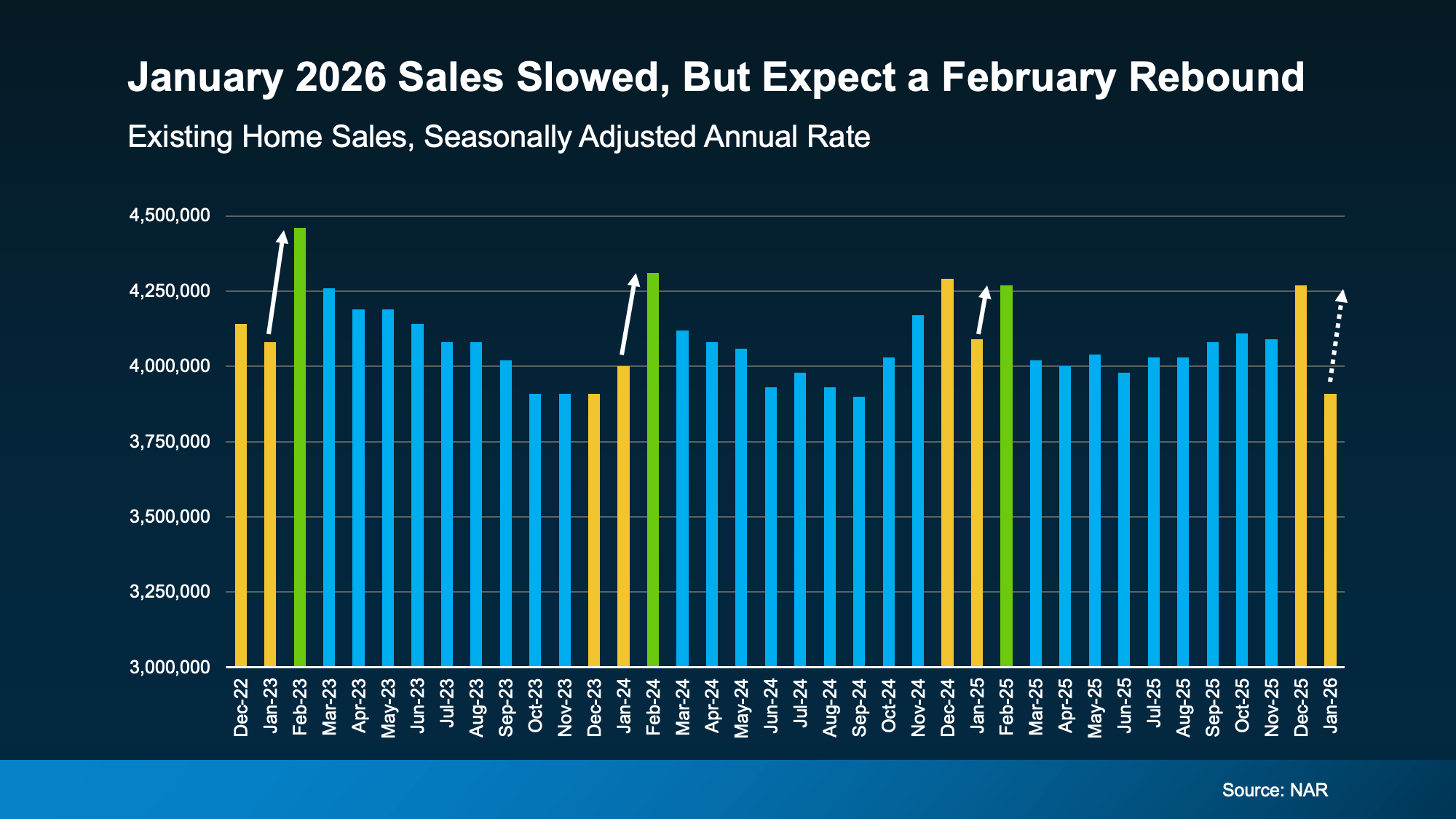

If you saw headlines that talked about how “home sales fell sharply in January,” it probably raised an eyebrow – especially if you’re thinking about selling your house. But context matters.

Yes, in January, home sales declined. But that has more to do with seasonality and the weather than it does with any big drop off in demand.

Reports coming out of the National Association of Realtors (NAR) say the pace of home sales fell roughly 8.4% last month compared to the month before. And that’s true. But it isn’t necessarily cause for alarm.

Data show it’s normal for sales to dip in January. In the last 4 years, that pattern has held true all but once. And sure, the decline we saw this year was a steeper drop off than the norm (the yellow bars on the right), but that can be explained too. More on that in a moment.

The really important part you’re not going to get from the headlines is this: typically speaking, the pace of home sales picks back up in February as the spring market starts to take off. That’s shown in the green bars below.

So even though the market slowed a bit momentarily, it should start to pick back up.

So even though the market slowed a bit momentarily, it should start to pick back up.

And just in case you’re wondering, why the bigger drop this year, especially with mortgage rates being lower than last year? Here’s your answer. As Realtor.com explains:

“Winter storm Fern, which dumped snow and ice across large swaths of the country, likely disrupted some closings, weighing on the data and making it difficult to pick out the housing market momentum trend from the weather noise.”

This January, 40 states were hit with widespread winter weather according to the National Weather Service. And in real estate, that slows down the momentum. Here’s why.

Existing home sales data tracks closed transactions, not new contracts. So, if inspections, appraisals, or final walk-throughs get delayed by storms, those deals often slide into the next month instead of falling apart – especially when buyers and sellers are still trying to move forward.

January’s missing sales are more likely “postponed” than “lost.” They haven’t disappeared. They’re just taking a little longer to close.

The rest of the data still points to a market that has traction heading into spring.

Affordability has improved for the 7th month in a row, and buyers are regaining negotiating power in many markets throughout the nation. So, this one monthly report doesn’t mean buyers aren’t buying. It just means, as weather warms up, activity should too.

Don’t confuse a weather-impacted month with a market losing steam. If anything, improving affordability is an indicator of more activity to come, not less.

If you have questions about what you’re hearing online or in the news, let’s chat. Because the truth is, a little context can give you back your peace of mind.

Displaying blog entries 31-40 of 1996