Do You Know What Your House Is Worth Today on Mt. Hood?

Wednesday, February 18, 2026

Add Comment

Displaying blog entries 21-30 of 450

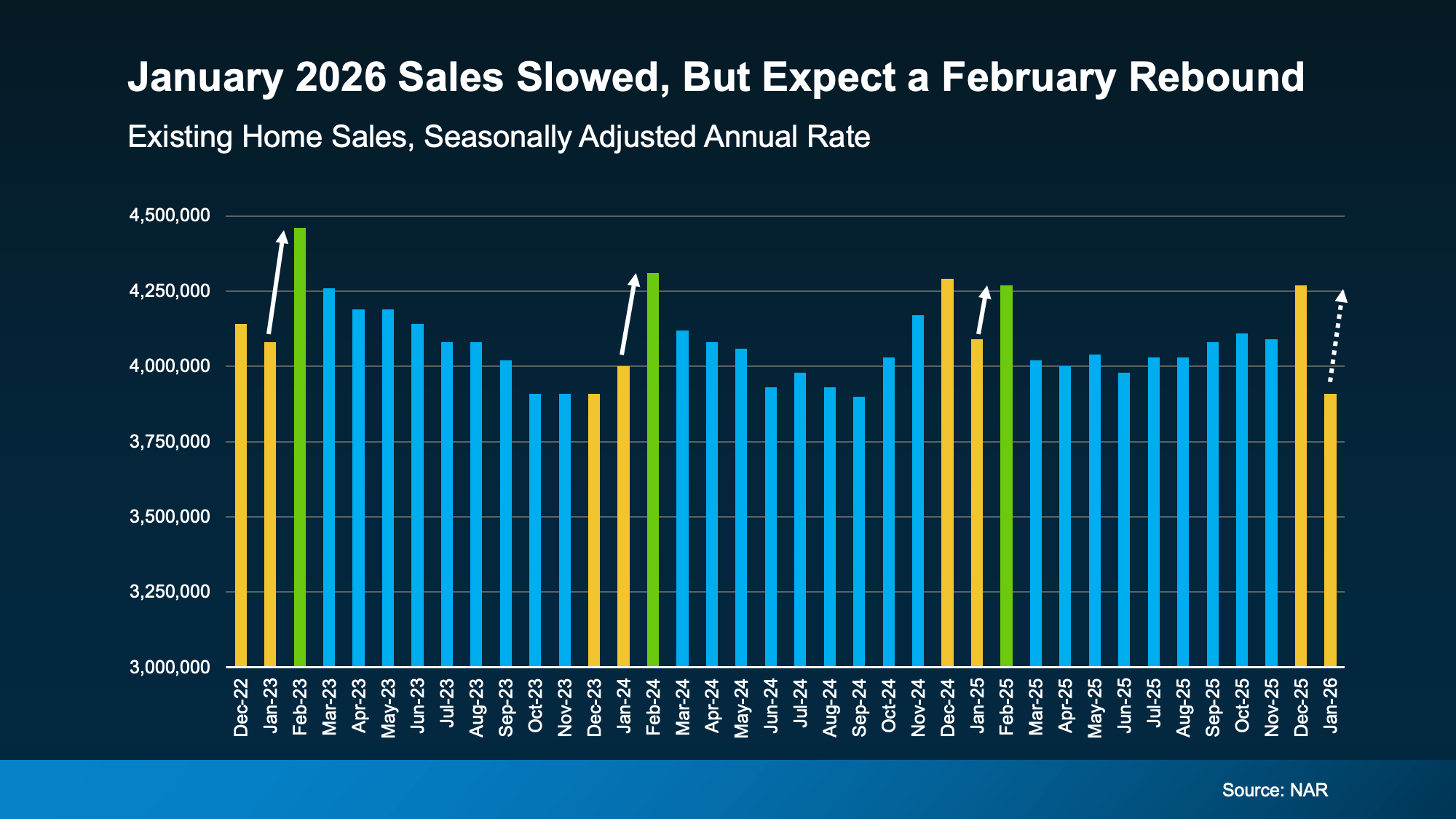

If you saw headlines that talked about how “home sales fell sharply in January,” it probably raised an eyebrow – especially if you’re thinking about selling your house. But context matters.

Yes, in January, home sales declined. But that has more to do with seasonality and the weather than it does with any big drop off in demand.

Reports coming out of the National Association of Realtors (NAR) say the pace of home sales fell roughly 8.4% last month compared to the month before. And that’s true. But it isn’t necessarily cause for alarm.

Data show it’s normal for sales to dip in January. In the last 4 years, that pattern has held true all but once. And sure, the decline we saw this year was a steeper drop off than the norm (the yellow bars on the right), but that can be explained too. More on that in a moment.

The really important part you’re not going to get from the headlines is this: typically speaking, the pace of home sales picks back up in February as the spring market starts to take off. That’s shown in the green bars below.

So even though the market slowed a bit momentarily, it should start to pick back up.

So even though the market slowed a bit momentarily, it should start to pick back up.

And just in case you’re wondering, why the bigger drop this year, especially with mortgage rates being lower than last year? Here’s your answer. As Realtor.com explains:

“Winter storm Fern, which dumped snow and ice across large swaths of the country, likely disrupted some closings, weighing on the data and making it difficult to pick out the housing market momentum trend from the weather noise.”

This January, 40 states were hit with widespread winter weather according to the National Weather Service. And in real estate, that slows down the momentum. Here’s why.

Existing home sales data tracks closed transactions, not new contracts. So, if inspections, appraisals, or final walk-throughs get delayed by storms, those deals often slide into the next month instead of falling apart – especially when buyers and sellers are still trying to move forward.

January’s missing sales are more likely “postponed” than “lost.” They haven’t disappeared. They’re just taking a little longer to close.

The rest of the data still points to a market that has traction heading into spring.

Affordability has improved for the 7th month in a row, and buyers are regaining negotiating power in many markets throughout the nation. So, this one monthly report doesn’t mean buyers aren’t buying. It just means, as weather warms up, activity should too.

Don’t confuse a weather-impacted month with a market losing steam. If anything, improving affordability is an indicator of more activity to come, not less.

If you have questions about what you’re hearing online or in the news, let’s chat. Because the truth is, a little context can give you back your peace of mind.

Buying a home is one of the biggest purchases you’ll ever make. And homeowner’s insurance is what protects that investment. Think of it as your safety net. NerdWallet explains it:

But that peace of mind does come with a cost, and lately those costs have been rising.

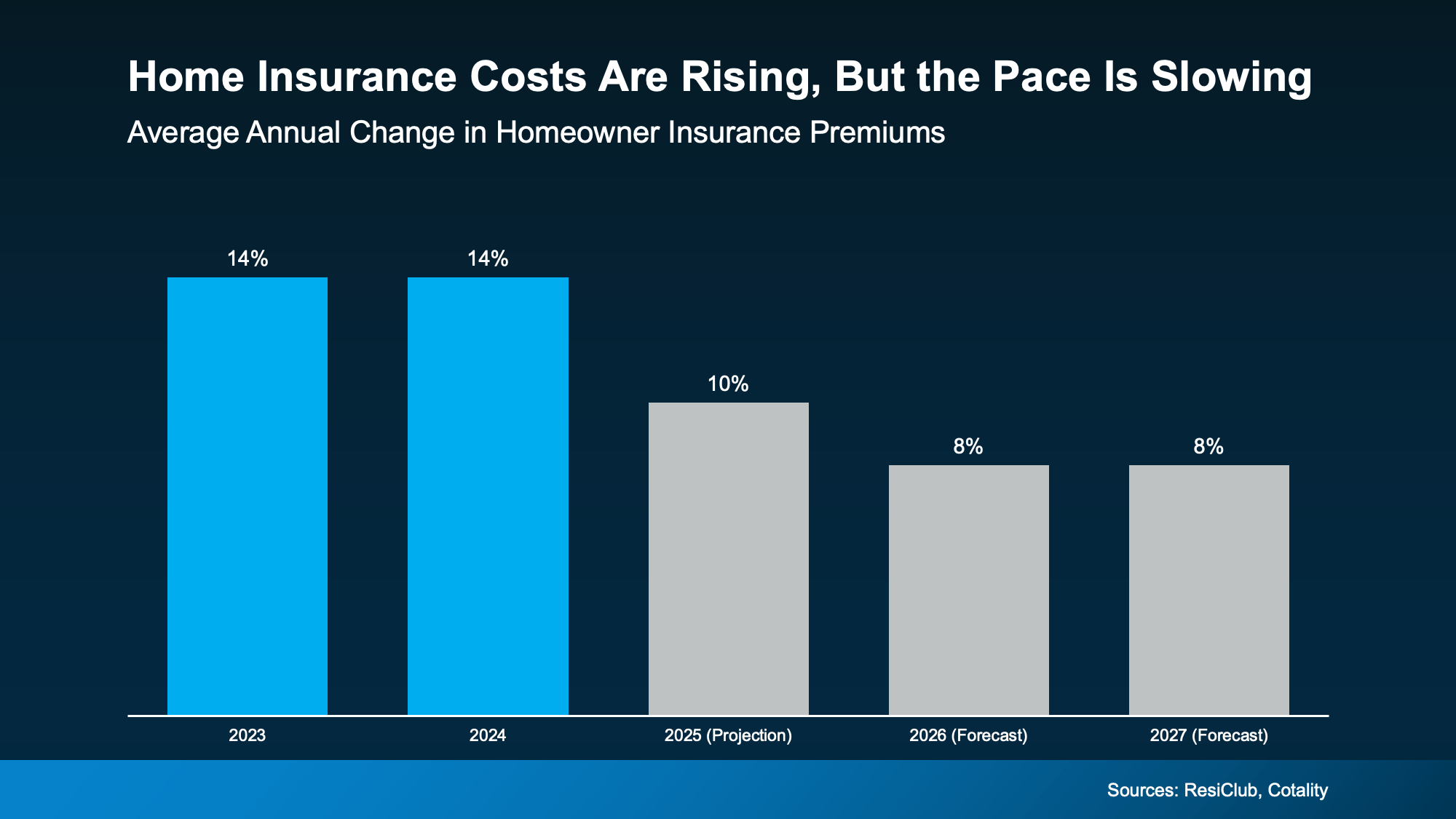

There are a number of factors causing insurance premiums to rise today. But, in the simplest sense, here’s what’s driving prices up according to the Insurance Research Council (IRC).

Severe weather events and natural disasters are happening increasingly often, leading to more claims. At the same time, homebuilding materials and labor are more expensive. So, when it comes time to work on those claims, insurers have to manage higher costs to repair or rebuild the affected homes.

That combination adds up to higher premiums. You can see how it’s climbed recently in the graph below. Each bar marks the percentage increase in insurance costs for that calendar year.

The good news is, the annual pace of the increase may be starting to ease according to ResiClub and Cotality. By their count:

The good news is, the annual pace of the increase may be starting to ease according to ResiClub and Cotality. By their count:

That’s still an increase, but at least the pace is slowing down. And here's another silver lining.

While insurance costs are rising, mortgage rates are falling. And that can help offset some of this expense. As Michael Gaines, Senior VP of Capital Markets, Cardinal Financial, explains:

“Rising taxes and insurance do create pressure, but they don’t erase the benefits of a lower rate . . . A small rate improvement, paired with the right loan program and smart planning, can still make homeownership possible . . . It’s less about one factor canceling another out, and more about helping buyers layer the right solutions together.”

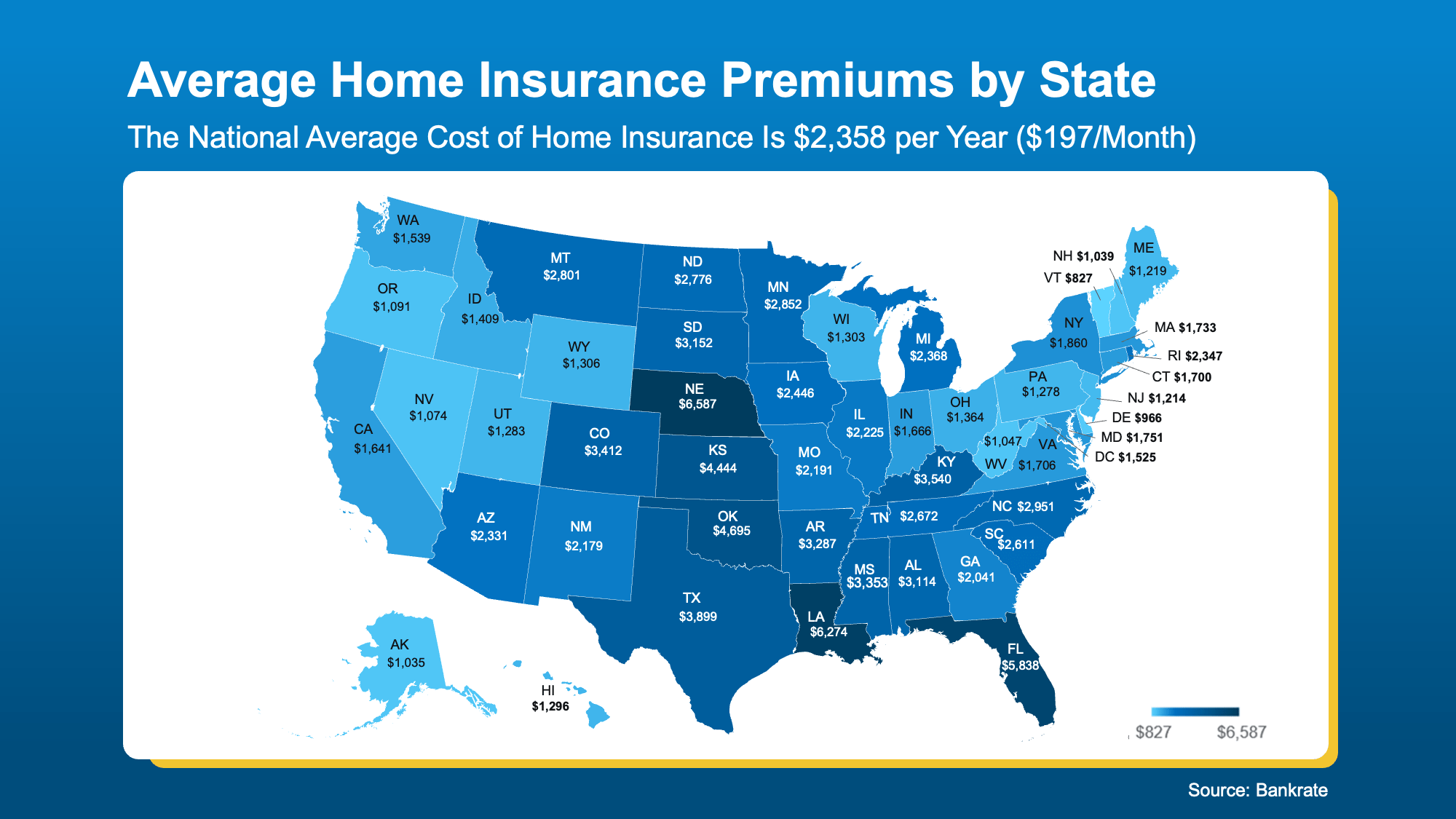

So how much do you need to budget for this? It depends on the price point and location of house, the coverage you need, and more. And just like with everything else in real estate, costs vary by area.

You can get a rough idea of your state’s typical premiums in the map below:

So, What Can You Do About It?

So, What Can You Do About It?Generally speaking, your first insurance payment will be wrapped into your closing costs. But after that, it’ll become a recurring expense. That’s why knowing these premiums are rising is so important. It helps you factor that into your budget, so you go in with a full picture of what you can comfortably afford.

If you’re crunching the numbers and trying to find other ways to save, here are a few tips from Insurify and NerdWallet that can help you get the best insurance price possible:

If you’re thinking about buying a home, don’t forget to plan ahead for your homeowner’s insurance.

While costs are rising, knowing what to expect and how to shop around can make a big difference as you’re budgeting for your purchase. Because this isn’t coverage you’ll want to skimp on. It’s your best protection for what’s likely your biggest investment.

Wondering what to expect from the housing market in 2026? You’re not the only one. For the past few years, affordability has been the biggest barrier standing between most people and their next move. And a lot of buyers and sellers have been holding their breath waiting for things to get better. The good news? It’s finally happening.

In 2025, affordability was the best it’s been in 3 years. And experts agree the momentum will keep going in 2026. And that’s based on their analysis of the key factors shaping the housing market in the year ahead: mortgage rates, inventory, and home prices.

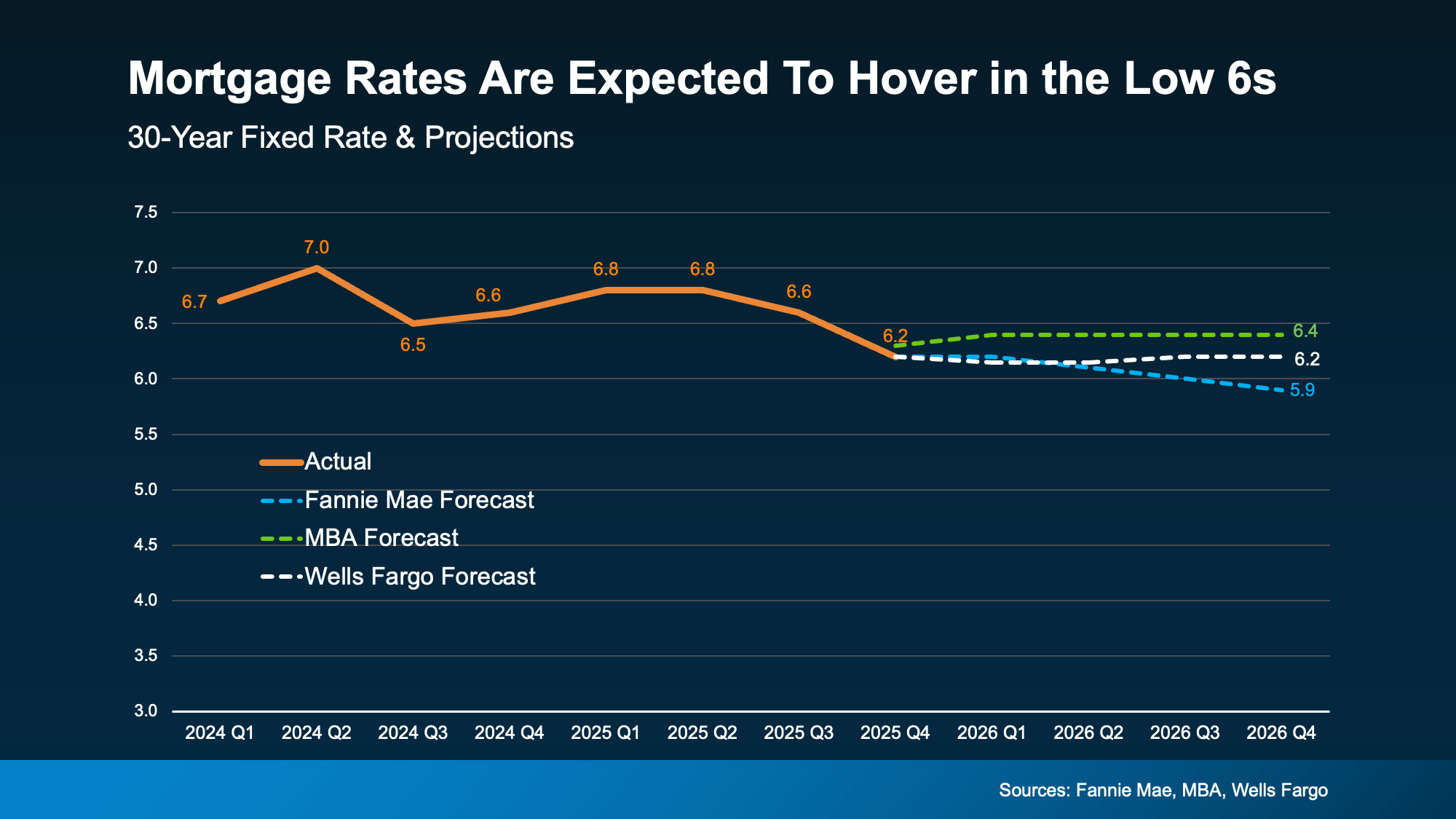

Mortgage rates have already come down from their peak. By some counts, they dropped by almost a full percentage point over the course of the last year. And that’s a big deal, even if it doesn’t sound like it. But how low will they go? And should you wait for them to come down more? Here’s your answer.

Forecasts suggest they’ll stay pretty much where they are now and hover in the low 6% range throughout 2026 (see graph below):

Where they go from here really depends on what happens with the economy, the job market, and any changes in monetary policy the Fed makes in the year ahead. The important thing is, they’re already lower than they were just one year ago and that’s ideal if you’re planning a 2026 move.

Where they go from here really depends on what happens with the economy, the job market, and any changes in monetary policy the Fed makes in the year ahead. The important thing is, they’re already lower than they were just one year ago and that’s ideal if you’re planning a 2026 move.

In 2025, the number of homes for sale improved by about 15%. As inventory rose, buyers regained things they hadn’t had in years: options, time to consider those options, and negotiating leverage. That helped restore more balance to the housing market.

Not to mention, the inventory gains are a big piece of what’s helped price growth slow down – which in turn improves affordability.

While the inventory gains this year aren’t expected to be as steep, experts at Realtor.com say the supply of homes for sale should grow by another 8.9% this year.

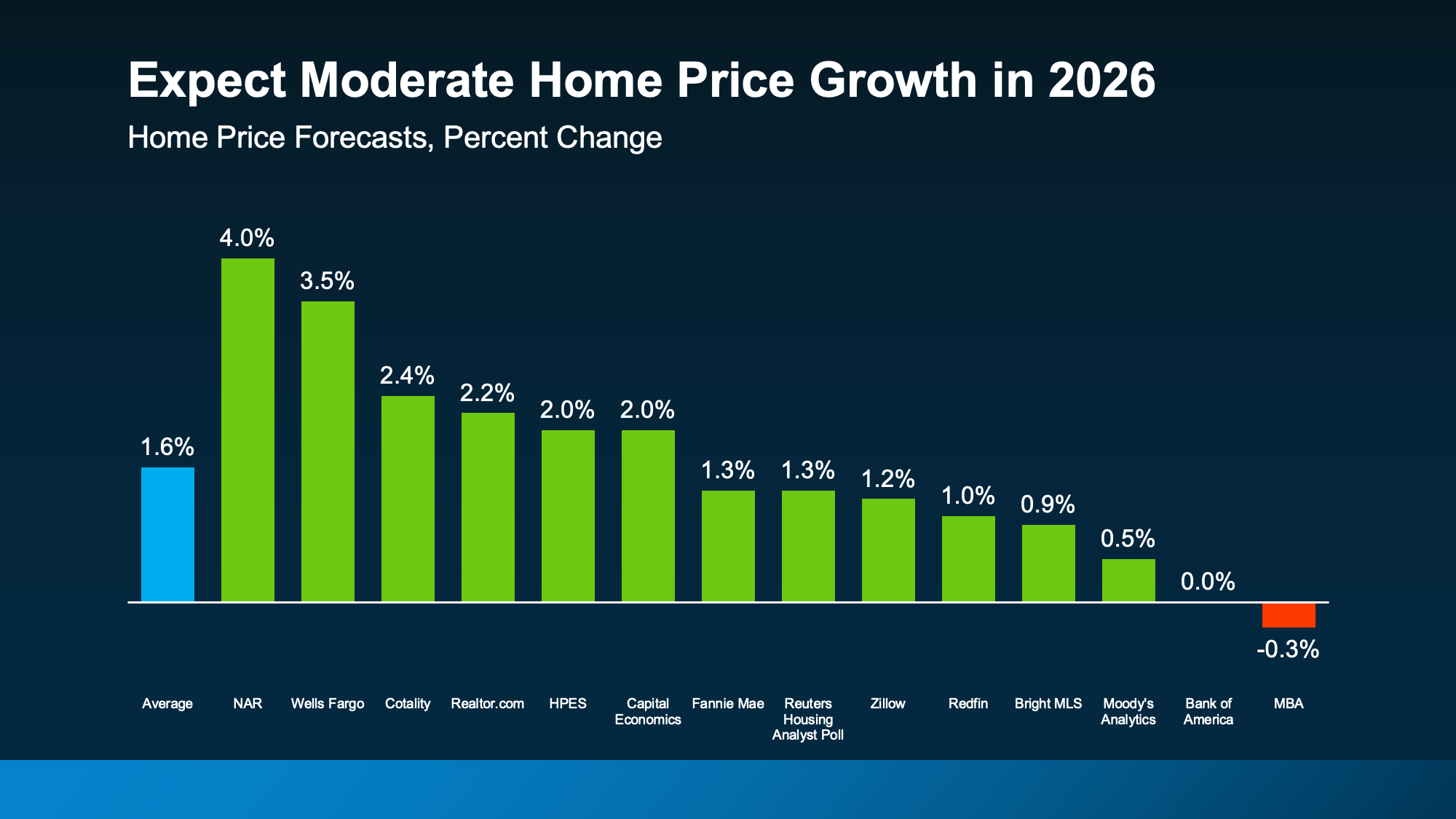

With more homes for sale, there isn’t as much upward pressure on prices right now. And we’ve seen that shake out over the past year. Even so, the overwhelming majority of experts say, nationally, prices will continue rising in the year ahead – just at a slower pace. On average, they say prices will rise by 1.6% in 2026 (see graph below):

And that's reassuring if you've been fed content on social media saying prices are going to come crashing down. But here’s what you need to remember most about this. It’s going to vary a lot by area.

And that's reassuring if you've been fed content on social media saying prices are going to come crashing down. But here’s what you need to remember most about this. It’s going to vary a lot by area.

So, lean on a local agent for the latest on what’s happening where you are. Some markets will see prices rise more than this. Others may see prices come down slightly. It really all depends on conditions in your local market

But overall, prices will continue to rise at the national level. And that’s good for the market as a whole. As Realtor.com explains:

“For homebuyers and sellers, the shift signals a more balanced market—one where price growth steadies, rate relief offers breathing room, and negotiating power tilts subtly toward buyers.”

All of this adds up to a better affordability equation in 2026. And that’s exactly why experts are saying we should see more homes sell (and more people buy) this year.

As Mischa Fisher, Chief Economist at Zillow, says:

As Mischa Fisher, Chief Economist at Zillow, says:

“Buyers are benefiting from more inventory and improved affordability, while sellers are seeing price stability and more consistent demand. Each group should have a bit more breathing room in 2026.”

The bottom line is, more people are finally going to be able to make their move this year. So, the question is: will you be one of them? The market is giving you an opportunity you haven’t had in a while. Maybe it’s time to take advantage of it.

Affordability won't change suddenly overnight. But, with several key trends working together, it should slowly and steadily improve in the months ahead.

That’s exactly why, in 2026, you should see a market with more balance, more predictability, and more breathing room than you’ve had in years.

Want more information about the opportunities unlocking in our local market?

Let’s chat.

If you’re thinking about selling your house this year, you may be torn between two options:

In 2026, that decision matters more than it used to. Here’s what you need to know.

Over the past year, the number of homes for sale has been climbing. And this year, a Realtor.com forecast says it could go up another 8.9%. That matters. As buyers gain more options, they also re-gain the ability to be selective. So, the details are starting to count again.

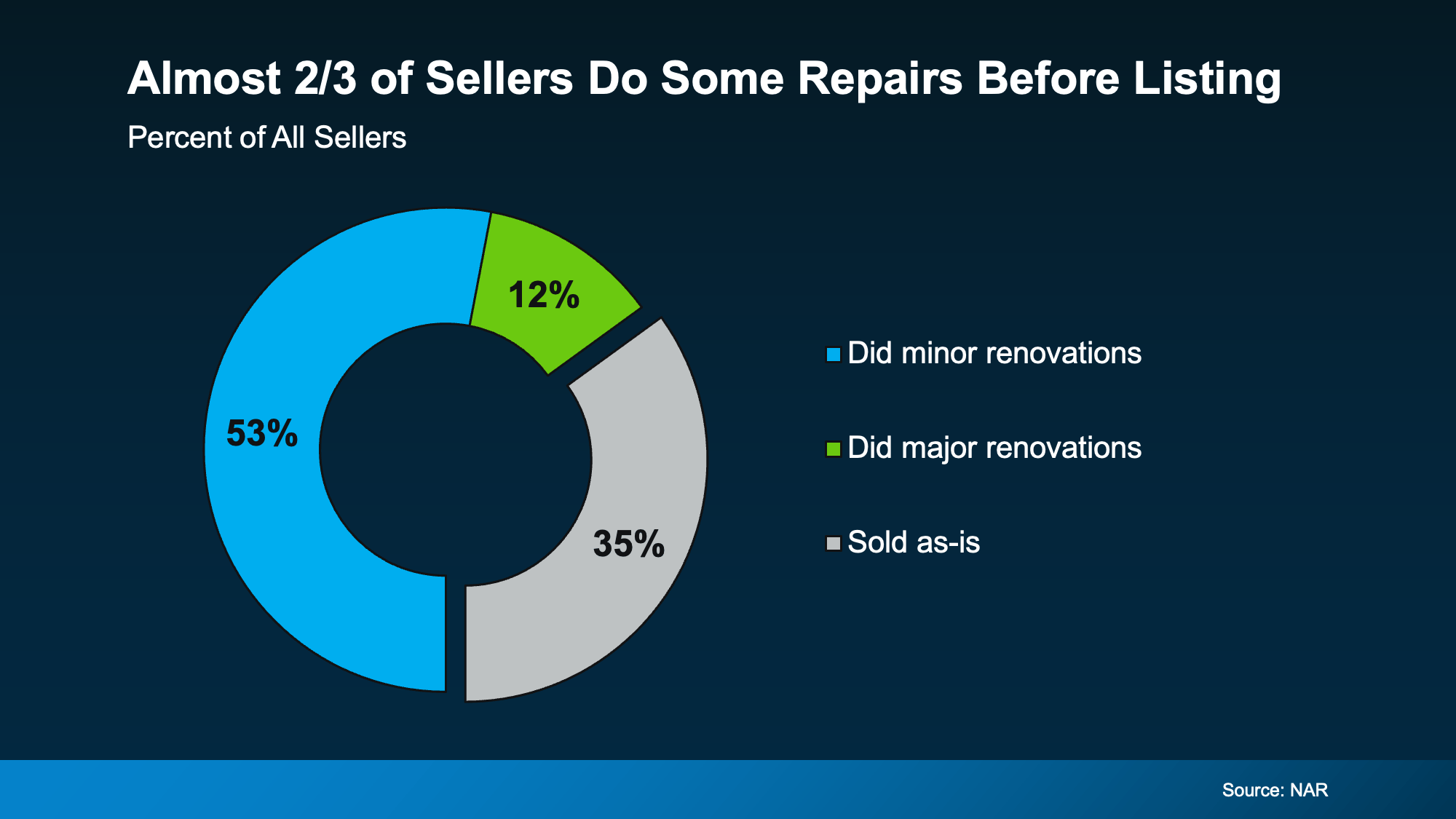

That’s one reason most sellers choose to make some updates before listing.

According to a recent study from the National Association of Realtors (NAR), two-thirds of sellers (65%) completed minor repairs or improvements before selling (the blue and the green in the chart below). And only one-third (35%) sold as-is:

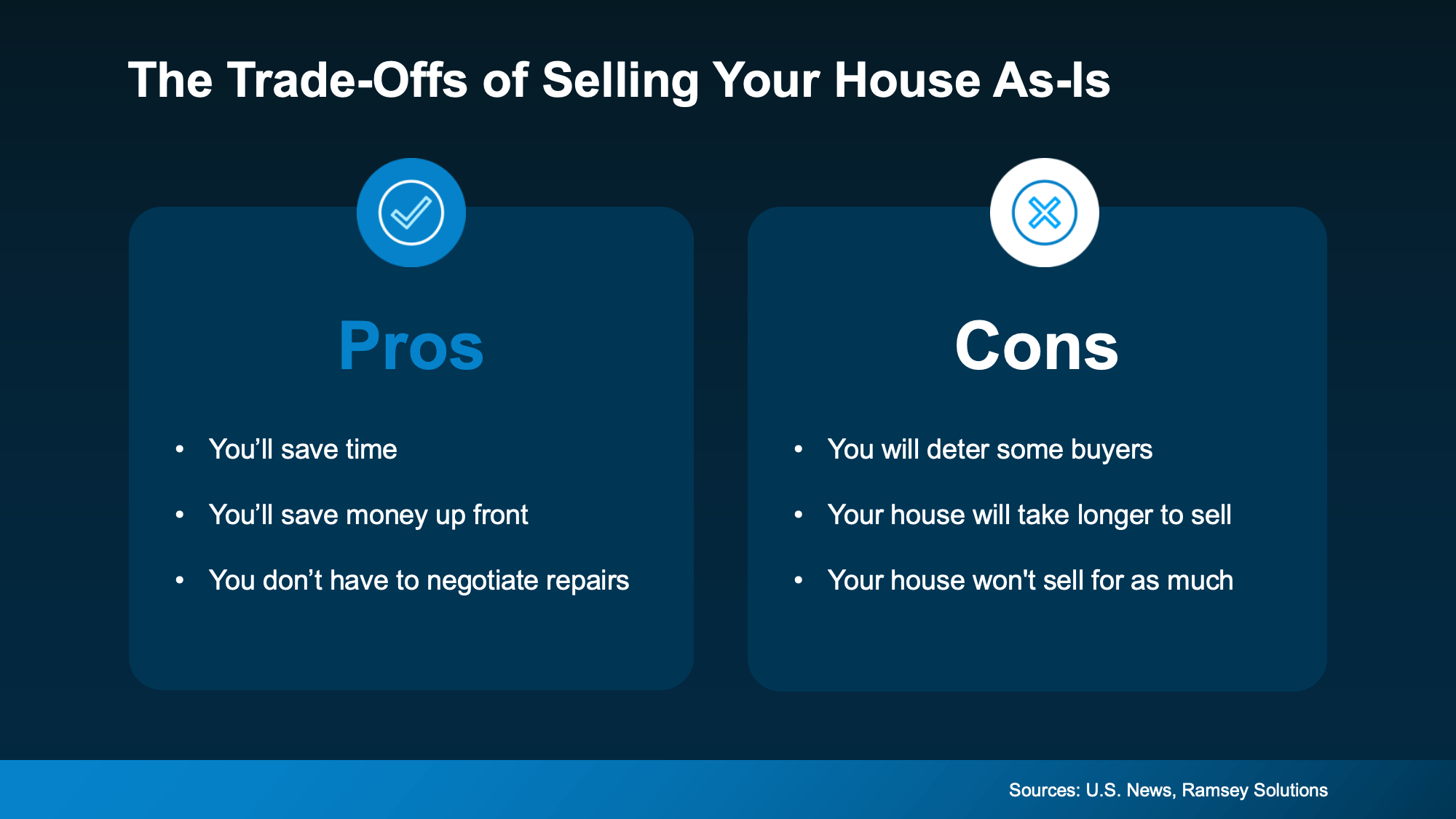

Selling as-is means you’re signaling upfront that you won’t handle repairs before listing or negotiate fixes after inspection. That can definitely simplify things on your end, but it also narrows your buyer pool.

Homes that are move-in ready typically attract more buyers and stronger offers. On the flip side, when a home needs work, fewer buyers are willing to take it on. That can mean fewer showings, fewer offers, more time on the market, and often a lower final price.

It doesn’t mean your house won’t sell – it just means it may not sell for as much as it could have.

How an Agent Can Help

How an Agent Can HelpSo, what should you do? The answer isn’t one-size-fits-all. It’s going to depend a lot on your house and your local market.

And that’s why working with an agent is a must. The right agent will help you weigh your options and anticipate what your house may sell for either way – and that can be a key factor in your final decision.

The good news is, there's still time to get repairs done. Typically speaking, the spring is the peak homebuying season, so there are still several months left before buyer demand will be at its seasonal high. That means you have time to make some repairs, without rushing or stressing, and still hit the listing sweet spot.

The choice is yours. No matter what you end up picking, your agent will market your house to draw in as many buyers as possible. And in today’s market, that expertise is going to be worth it.

While selling as-is can still make sense in certain situations, in some markets today, it may cost you. So, no, you don’t have to make repairs before you list. But you may want to.

To make sure you’re considering all your options and making the best choice possible, let's have a quick conversation about your house.

Momentum is quietly building in the housing market. New data from NerdWallet shows more Americans are starting to think about buying a home again. Last year, 15% of respondents said they planned to buy a home in the next 12 months. This year, that number rose to 17%.

That 2% increase might not sound like a big jump, but in a market where buyer demand has been cooling for the past few years, it’s a sign things are starting to shift. More people are feeling ready (or at least closer to ready) to take the leap and buy a home in 2026.

And if you’re in that camp and buying a home is on your goal sheet this year, this is your nudge to connect with a local agent and a trusted lender to start laying the groundwork now.

If you’re eager to get the ball rolling right away, here's what to tackle first:

Even if buying feels like a late-2026 goal, this moment still matters. The buyers who feel the most confident later are usually the ones who quietly prepared earlier.

That doesn’t mean big financial commitments or major lifestyle changes. It just means setting yourself up so you’re ready when the timing is right. Here are a few low-stress ways to do that:

If buying a home in 2026 is on your radar, let’s start the conversation today. Not to rush a decision, but to make sure you know how to get ready for your moment.

Because every move (whether it’s next year or later) is smoother when it starts with a plan. And if you need help coming up with one that works, let’s connect.

If a move is on your radar for 2026, there’s a lot more working in your favor than there has been in a while.

After a stretch where many people felt stuck, 2026 is shaping up to be a year with more balance, more options, and more clarity for people who want to make a move. Not because the market is suddenly “easy,” but because several key conditions are shifting.

Here’s what the experts are saying you have to look forward to.

Danielle Hale, Chief Economist at Realtor.com:

“After a challenging period for buyers, sellers and renters, 2026 should offer a welcome, if modest, step toward a healthier housing market.”

The National Association of Realtors (NAR):

“Top economists have one word to sum up the housing market for 2026: opportunity. Lower mortgage rates and a rising supply of homes are expected to open up the housing market . . . something the real estate industry and potential home buyers and sellers have been waiting for, following three years of stagnation.”

Mark Fleming, Chief Economist at First American:

“. . . for the first time in several years, the underlying forces are finally aligned toward gradual improvement. Mortgage rates may drift down only slowly, but income growth exceeding house price appreciation will provide a boost to house-buying power — even in a higher-rate world. Affordability won’t snap back overnight, but like a ship finally catching a steady tailwind, it’s now sailing in the right direction.”

Mischa Fisher, Chief Economist at Zillow:

“Buyers are benefiting from more inventory and improved affordability, while sellers are seeing price stability and more consistent demand. Each group should have a bit more breathing room in 2026.”

Just remember, while the national outlook is improving, conditions will still be different based on where you live. Some markets will move faster than others. Some will see stronger price growth. Others will remain flat. As Lisa Sturtevant, Chief Economist at Bright MLS, explains:

“Market performance will hinge on local economic conditions, making 2026 one of the most geographically divided markets we’ve seen in years.”

That’s why understanding what’s happening in your specific area is key. The national trends set the stage, but local dynamics determine how they play out for you. And that's why you need an agent.

If you want to talk through what’s expected for our local market and which trends you’ll want to take advantage of, let’s connect.

Displaying blog entries 21-30 of 450