Rates Are the Lowest They’ve Been in the Last 3 Spring Seasons

Wednesday, April 29, 2026

Add Comment

Displaying blog entries 1-6 of 6

At some point, as you start thinking about the years ahead, this question tends to come up:

“Could I stay here long-term… or would it make more sense to move?”

It’s not always urgent. It often shows up in small moments, like going up and down the stairs, keeping up with the maintenance, or just thinking about what the next chapter of your life might look like in this home.

And for most people, the answer is simple. They want to stay.

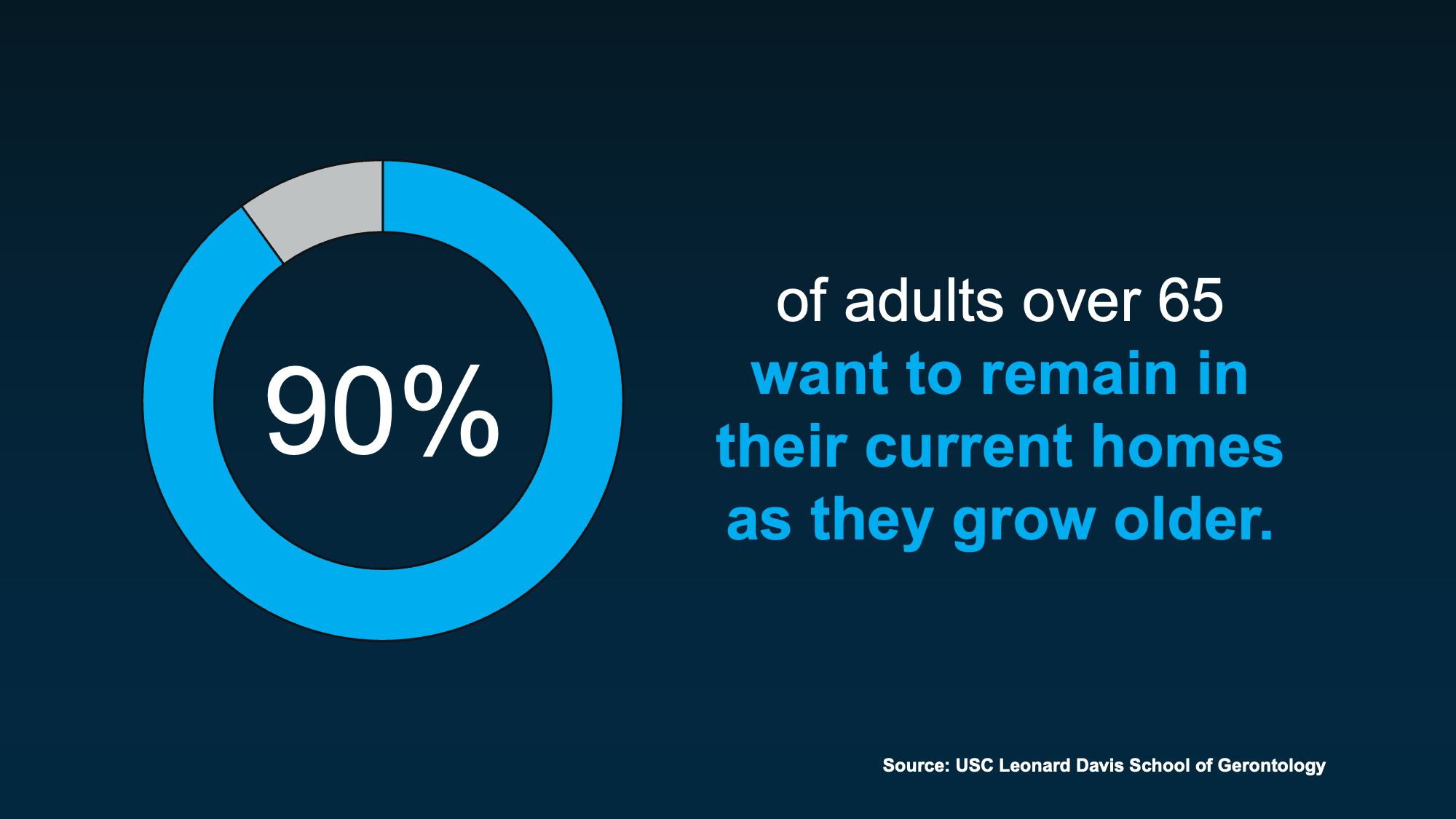

The USC Leonard Davis School of Gerontology found about 90% of adults over 65 prefer to stay in their homes as they get older (see below):

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

But even if staying feels like the right answer, it’s still worth thinking ahead about what that might actually look like. That’s where the right agent can really help.

Aging in place is definitely possible. But it’s better if you have a plan. And here’s why. The home that once worked perfectly may need to change with you over the years. And it’s easier if you can anticipate those expenses.

Some of those changes are going to be simple. Others can be a meaningful investment. And that’s why thinking about it early matters. Not because you need to decide anything right now, but because it gives you time.

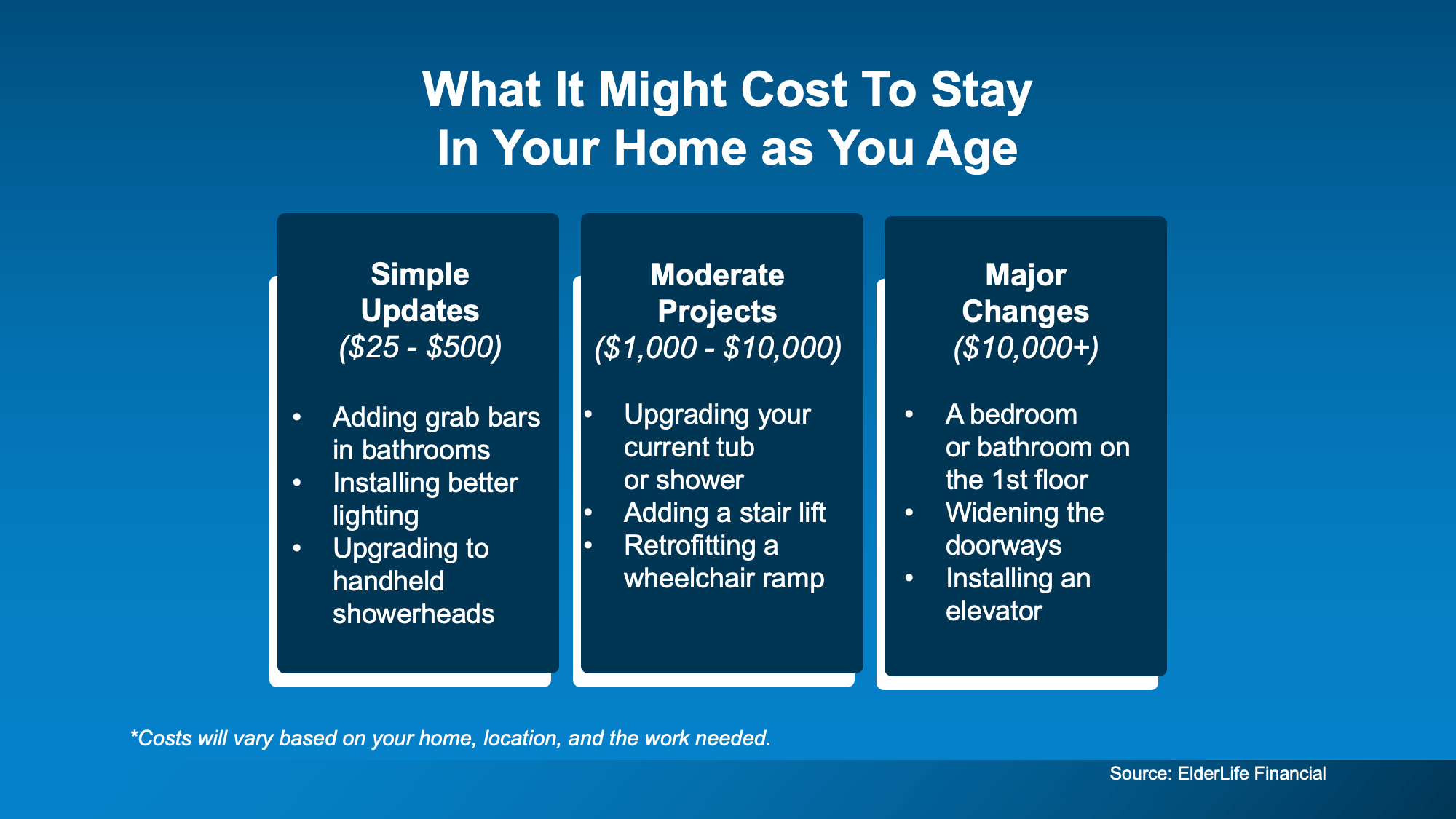

According to ElderLife Financial, here's a rough baseline of what it could cost depending on what needs to be done (see below):

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

And don’t worry. If your heart is really set on staying, but the costs feel like a concern, it helps to know you have options. Depending on your situation, there may be financial assistance programs available, along with tools like home warranties to help manage unexpected costs.

Just remember, if you’re thinking about making updates, it’s always worth having a quick conversation before you start. A real estate agent can help you understand which changes tend to make sense for your situation and how they may impact your home’s value based on your local market.

But staying isn’t always the best fit for every situation. According to Pegasus Senior Living:

“While most seniors hope to age in place, practical considerations sometimes make selling a home the wiser choice.”

Sometimes, it comes down to a simple shift: when the home that once made life easier, starts to make it harder.

That might look like:

And sometimes, it’s not about necessity at all. It’s about lifestyle. Some homeowners just don’t want to live through major renovations. Others are ready to simplify, downsize, or move somewhere that better fits this next chapter, whether that’s a smaller home, a 55+ community, or a place closer to family.

For them, moving simply means making daily life easier.

There’s no one-size-fits-all answer here.

Some people stay and make updates. Others move to simplify things. Either can be the right choice. The goal isn’t to pick one today. It’s to understand your options early, so when the time comes, you feel confident instead of rushed.

And if you ever want a sounding board to think through what the future could look like for you, let’s connect.

There’s a lot of uncertainty right now and that’s leading to some dramatic headlines. And if you’re thinking about buying a home, that can make you feel a little less sure about your decision.

A recent study by CNBC asked homebuyers what they’re most worried about, and three themes kept coming up again and again:

But a lot of what you may be hearing on those is based more on misconceptions. Not facts. So, let’s break it down and separate fact from fiction.

One idea doing its rounds on social is that mortgage rates are going to drop dramatically soon. So, it’s better to wait to buy.

But is that really what’s expected?

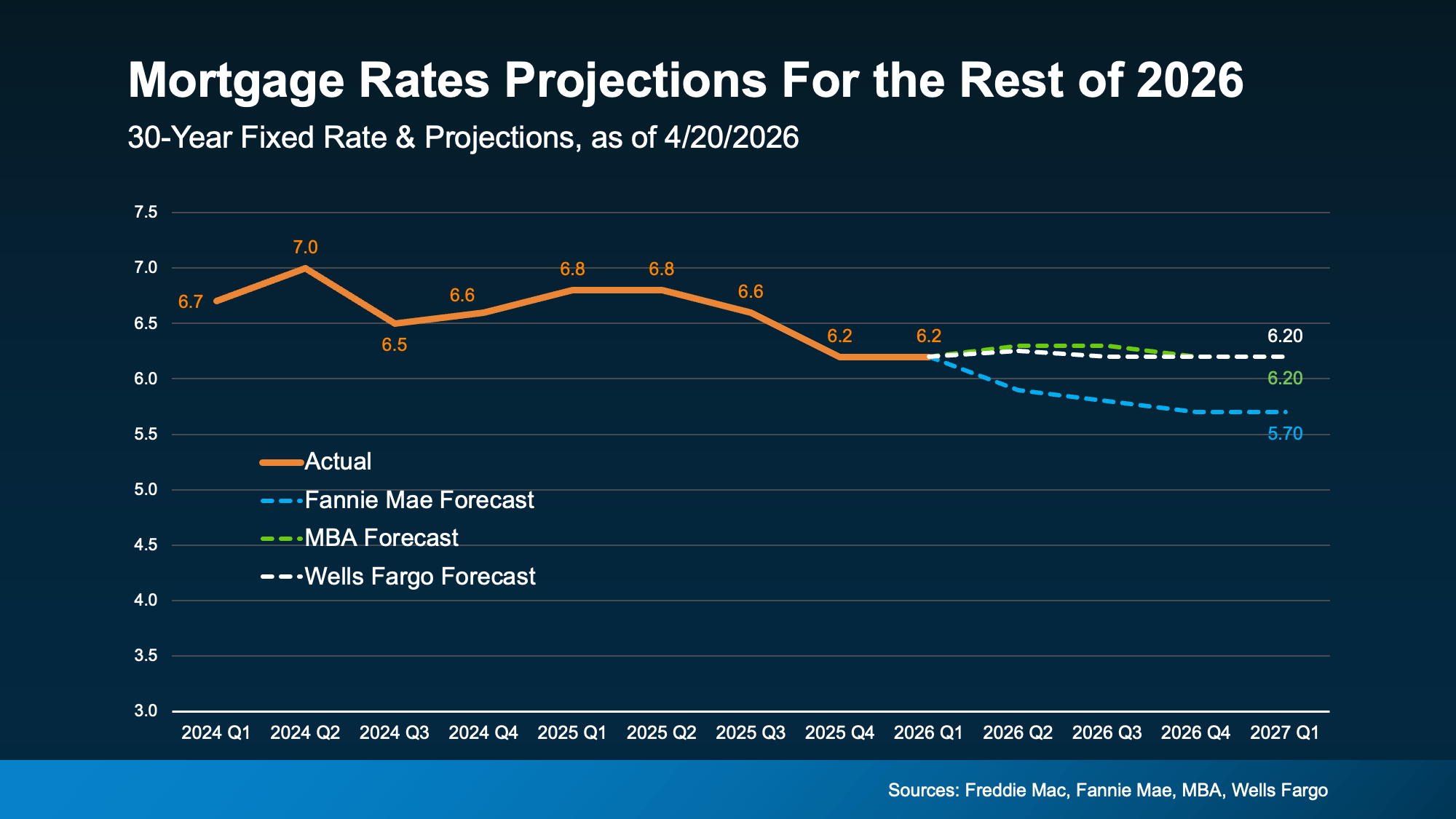

While mortgage rates have come down a bit in the last few weeks, forecasts don’t show a major drop ahead. The most likely scenario is that rates stay somewhere in the low 6% range this year.

And that’s not a big change from where rates are now (see graph below):

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. As U.S. News explains:

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. As U.S. News explains:

“Mortgage rates aren't expected to change much over the next several quarters . . .”

Not to mention, even with rates where they are today, it’s already more affordable than a year ago. So, even if they don’t change much, it’s still better than it was.

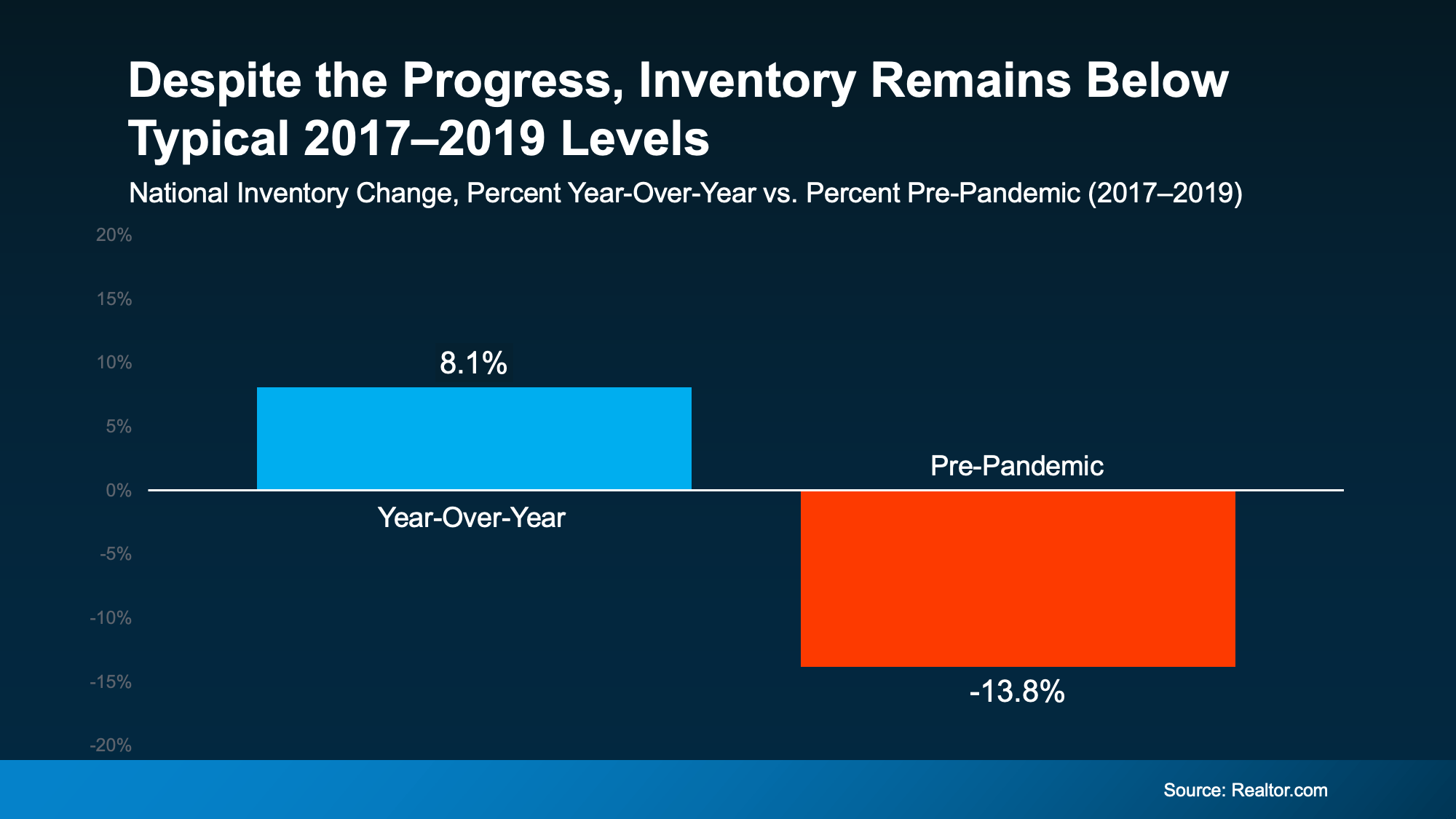

You’ve probably heard inventory is up. And nationally, it is. The number of homes for sale is 8% higher than this time last year. But that's not a bad thing. In fact, it’s one of the reasons buyers have a bit more breathing room right now.

The problem is the headlines are making something good, sound bad. They’re focusing on how this is the most inventory we’ve had since 2019 or how many homes builders are building. And that can make it sound like the number of homes for sale is rising too far, too fast.

But that’s not what the bigger picture shows.

Data from Realtor.com proves that, even though inventory is up compared to last year, it’s still nearly 14% lower than it was during the last normal housing market (2017-2019):

While it can vary a lot based on where you live, only 9 states have more inventory than pre-pandemic today. That’s a key reason why there still aren’t enough homes for sale to trigger something like the crash back in 2008.

While it can vary a lot based on where you live, only 9 states have more inventory than pre-pandemic today. That’s a key reason why there still aren’t enough homes for sale to trigger something like the crash back in 2008.

You’ve probably seen this one, too. The confusion is coming from the fact that some metros are experiencing slight price declines. And influencers are running with that and saying prices are crashing. But that’s not the reality.

Most areas are seeing prices rise, not fall. And that’s because:

And those are 3 big reasons prices aren’t headed for a crash.

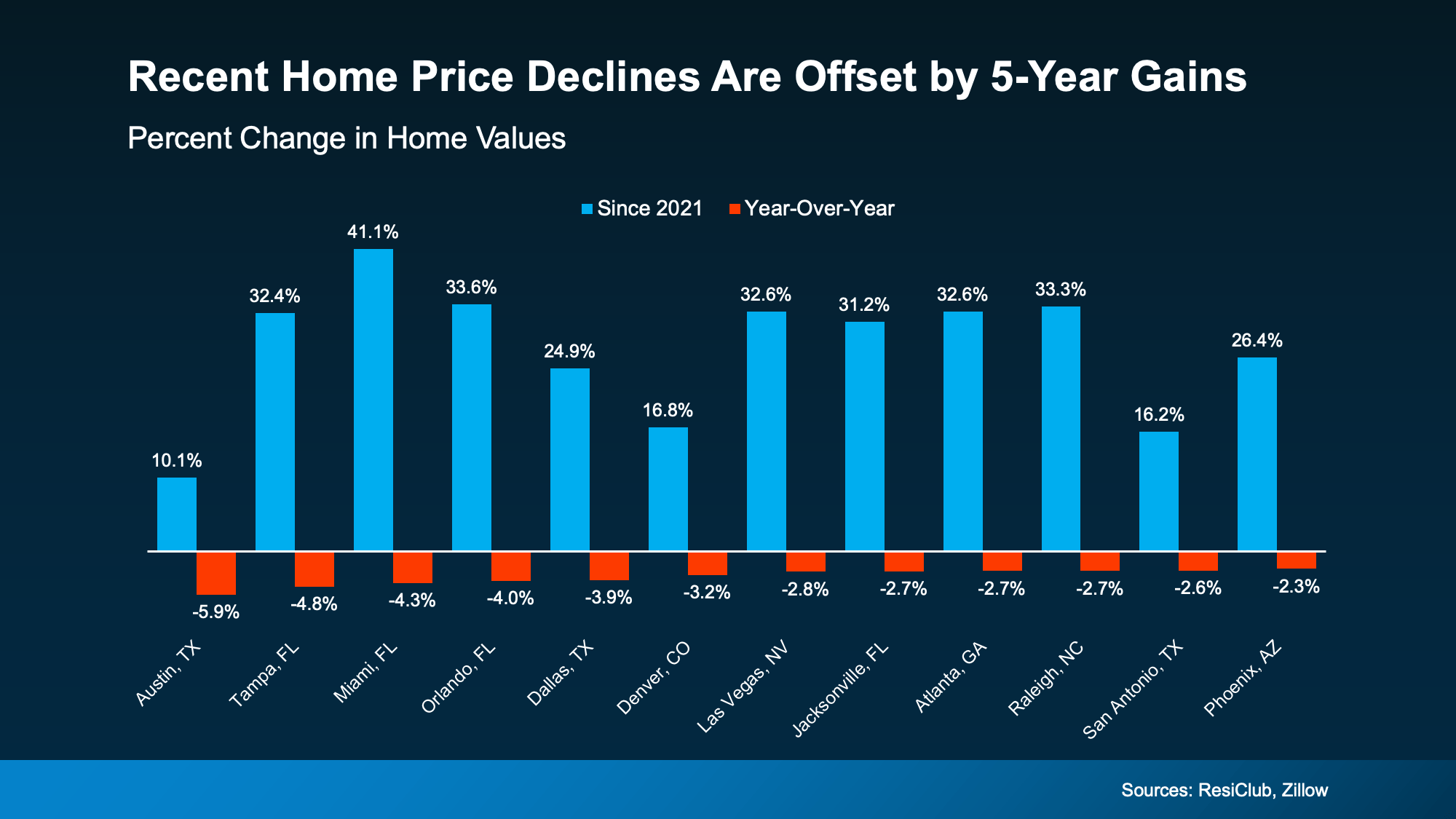

And even in the markets experiencing mild declines, the drops aren’t enough to cancel out the big gains most homeowners have seen in the last 5 years (see graph below):

That’s not a crash. That’s just prices moderating after a few record-breaking years.

That’s not a crash. That’s just prices moderating after a few record-breaking years.

Online posts are going to make things sound worse than they are. If you want a true, data-bound look at what’s really happening in today’s market, lean on a real estate agent.

Let’s connect so you have someone to separate fact from fiction today.

You’ve probably asked yourself lately: Is it even worth trying to buy a home right now? It’s a question a lot of people are asking.

With today’s home prices and mortgage rates, renting can feel like the easier path. In some cases, it might even seem like the only realistic option right now. And if that’s where you are, there’s nothing wrong with that.

But if you’re weighing the decision, there’s one part of the conversation that doesn’t get talked about enough.

It’s what each choice does for your future.

Depending on your situation, renting does have some advantages:

But even with those benefits, a Bank of America survey found 70% of aspiring homeowners worry about what long-term renting means for their future. And that concern comes down to one thing: you’re not building anything for your future. As Yahoo Finance explains:

“Paying rent doesn't build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

So, while renting may feel easier, the flexibility you get comes at a cost.

On the other hand, owning a home is one of the most consistent ways people build wealth over time. Why? When you’re a homeowner, you gain something called equity. That’s the difference between what your home is worth and what you owe.

That equity grows with every monthly payment you make. It also gets a boost as home values go up through the years – and it adds up quicker than you may think.

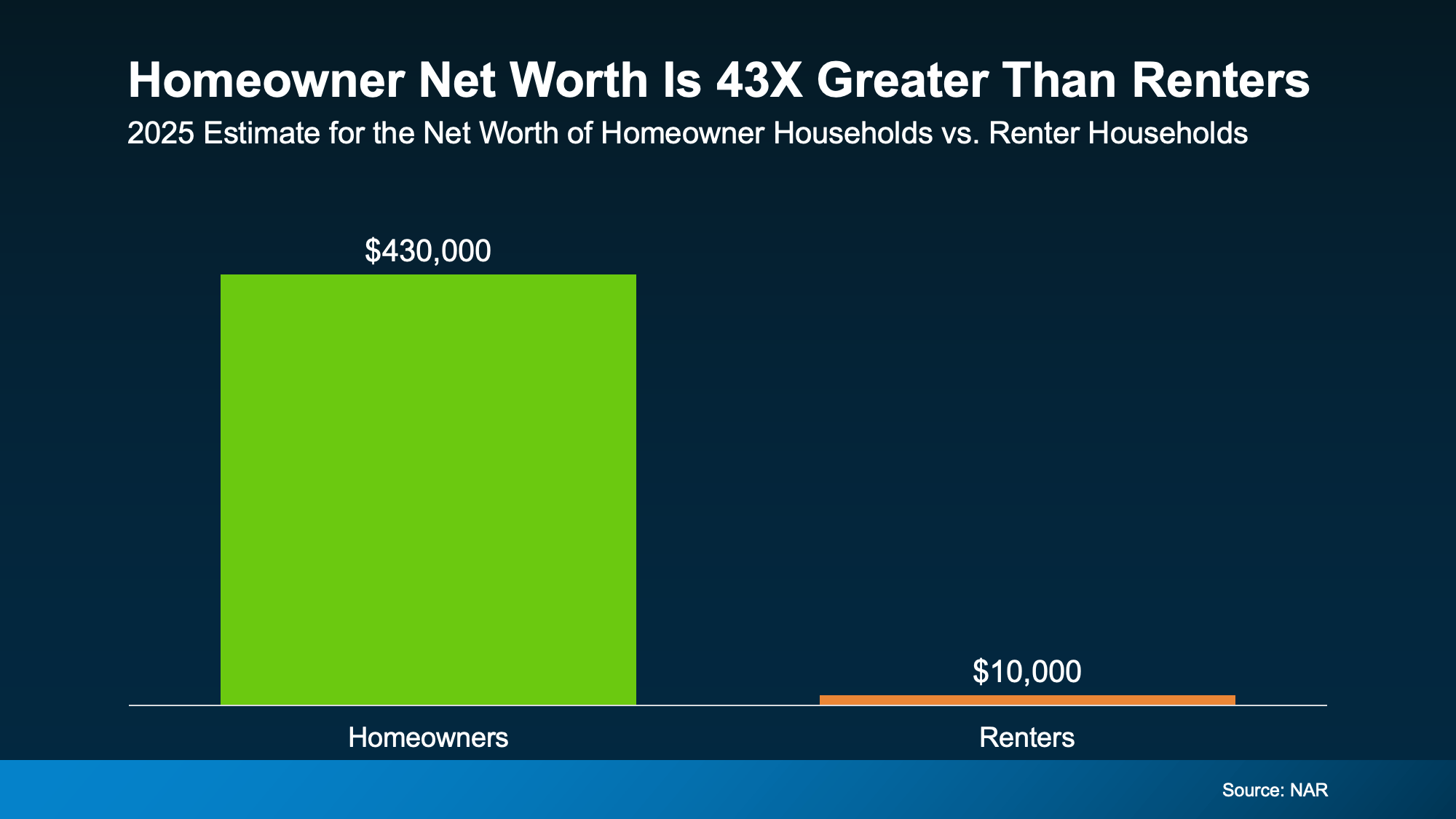

Today, the National Association of Realtors (NAR) says the average homeowner’s net worth is 43X greater than that of a renter:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

And it’s not because homeowners make wildly different decisions day to day. It’s because over time, one path builds something, and the other doesn’t.

So sure, buying comes with some upfront costs and more responsibility. But it’s basically a savings account you can live in.

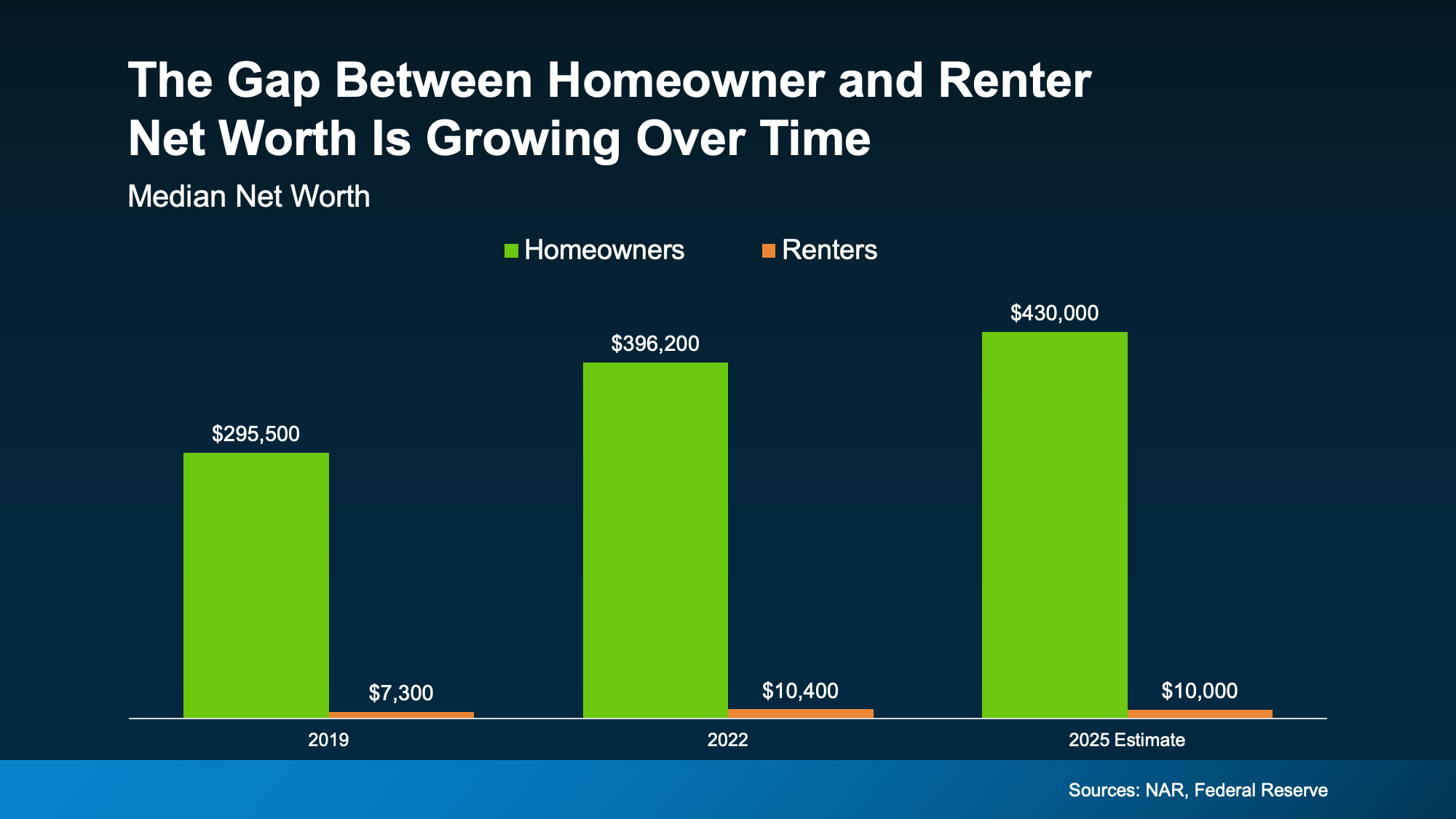

And here’s something else interesting. That net worth gap between renters and homeowners has been widening over time, not shrinking.

If you look back at the reports on net worth through the years, you can see the gap is growing as homeowners gain wealth and renters stay stuck in the rental trap (see graph below):

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

Even in 2025, when home prices were moderating, homeowners still gained even more ground. And that tells you something important:

When you can afford it and you’re ready for the responsibility, history shows buying is usually worth it in the long run. Because either way, you’re paying for someone’s mortgage and building someone’s net worth.

When you rent, it’s your landlord’s mortgage – not yours. But when you buy? Your monthly payments help build equity.

The question is: whose do you want to pay? Yours or theirs?

The short answer is, it depends on your situation.

While the long-term benefits of buying are clear, that doesn’t mean the timing is right for everyone right now. And that’s okay. You should only buy a home once you’re ready and the numbers work for you.

But whether you’re looking to buy now or planning for the future, the first step is the same. You should have a quick conversation with a local real estate agent about your goals, timeline, and budget.

They can help you run the numbers and see what’s realistic. You may find buying is closer than you thought. And if not, you’ll at least know exactly what it will take to get there.

Because the sooner you have a plan, the sooner you can decide when it makes sense, instead of wondering if it ever will.

Renting may feel more do-able today. But over time, it could cost you.

If you want to ditch renting and start building something for your future, it starts with a simple conversation. Let’s connect, talk about your specific goals, and explore your options – so you’re ready when the time is right for you.

SANDY, Ore. — Personal use firewood permits are now available for the season on Mt. Hood National Forest.

All woodcutters must obtain a firewood permit to cut and haul firewood from the Forest. Permits are available at a district office or by submitting a firewood permit application. Each household may collect a maximum of six cords annually with a free firewood permit for personal use only. Permits are valid through November 30.

Woodcutters who need more than six cords of firewood or intend to collect firewood for resale must purchase a commercial firewood permit, which is available upon request pending availability.

All woodcutters must carry their permit, firewood load tags, firewood map, and a current information sheet while harvesting. Woodcutters may only collect and cut downed wood. Felling standing trees, dead or alive, is illegal. Firewood cutting areas are described on the required firewood maps and information sheets, which are updated regularly and reflect the current Industrial Fire Precaution Level of each area.

More firewood information is available online: www.fs.usda.gov/r06/mthood/permits/firewood

Conditions across Mt. Hood National Forest vary and may change rapidly. Some Forest Service roads may be snow-covered, icy, or muddy. Several roads remain impassable due to downed trees, landslides, culvert blockages, and other damage caused by December’s significant storms. Vehicle access to some areas may be limited due to wildfire closures. Always know before you go: www.fs.usda.gov/r06/mthood/alerts

Contact a district office for information on current conditions: www.fs.usda.gov/r06/mthood/offices

Some community members who rely on firewood to heat their home may struggle to harvest firewood due to age or physical disabilities. Learn more about Mt. Hood National Forest’s firewood assistance program and how to apply: www.fs.usda.gov/media/158825

Displaying blog entries 1-6 of 6