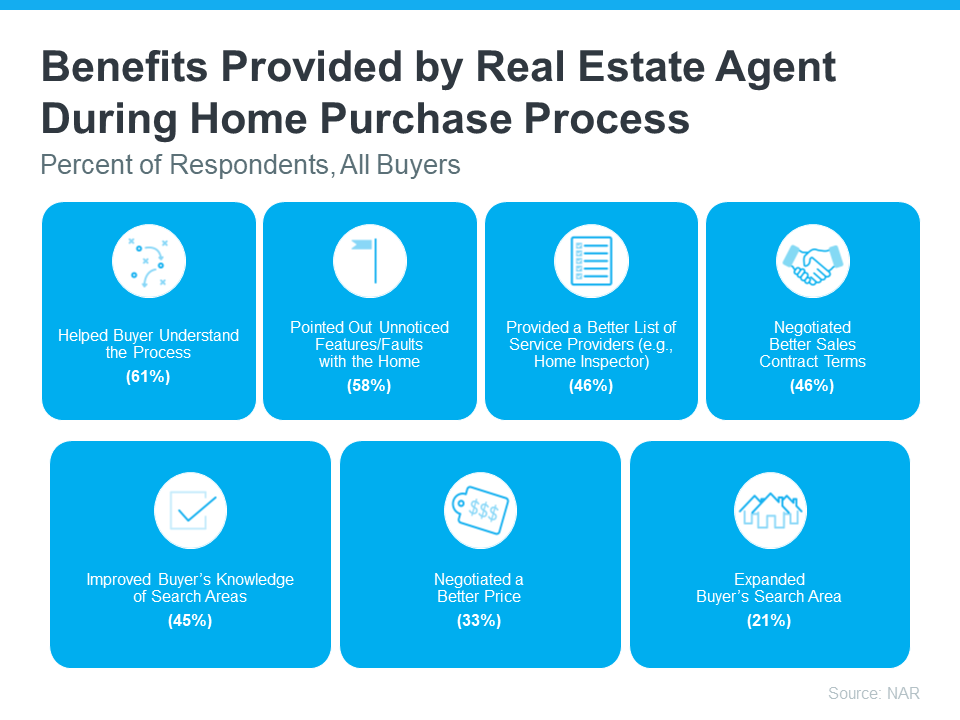

Working With an Agent Beats Going Solo

Sell Smarter: Why Working with a Real Estate Agent May Beat Going Solo

If you're thinking about selling your house on your own, called “For Sale by Owner” or FSBO, there are some important things to consider. Going this route means taking on a lot of responsibilities by yourself – and that can be a bit of a headache.

A recent report from the National Association of Realtors (NAR) found two of the most difficult tasks for people who sell their house on their own are getting the price right and understanding and performing paperwork.

Here are just a few of the ways an agent helps with those difficult tasks.

Getting the Price Right

Setting the right price for your house is important when you're trying to sell it. If you're selling your house on your own, two common issues can happen. For starters, you might ask for too much money (overpricing). Alternatively, you might not ask for enough (underpricing). Either can make it hard to sell your house. According to NerdWallet:

“When selling a home, first impressions matter. Your house’s market debut is your first chance to attract a buyer and it’s important to get the pricing right. If your home is overpriced, you run the risk of buyers not seeing the listing.

. . . But price your house too low and you could end up leaving some serious money on the table. A bargain-basement price could also turn some buyers away, as they may wonder if there are any underlying problems with the house.”

To avoid these problems, it's a good idea to team up with a real estate agent. Real estate agents know how to figure out the perfect price because they understand the local housing market. They can use their expertise to set a price that matches what buyers are willing to pay, giving your house the best chance to impress from the start.

Understanding and Performing Paperwork

Selling a house involves a bunch of paperwork and legal documentation that has to be just right. There are a lot of rules and regulations to follow, making it a bit tricky for homeowners to manage everything on their own. Without a pro by your side, you could end up facing liability risks and legal complications.

Real estate agents are experts in all the contracts and paperwork needed for selling a house. They know the rules and can guide you through it all, reducing the chance of mistakes that might lead to legal problems or delays.

So, instead of dealing with the growing pile of documents on your own, team up with an agent who can be your advisor, helping you avoid any legal bumps in the road.

Bottom Line

Selling your house is a big deal, and it can be complicated. Having a real estate agent can make a huge difference with setting the right price and managing all the details, so you can sell confidently. Let’s connect to make the process smooth and take the stress off your plate.