The Downside of Selling Your House on Mt. Hood

Friday, June 21, 2024

Add Comment

Displaying blog entries 131-140 of 875

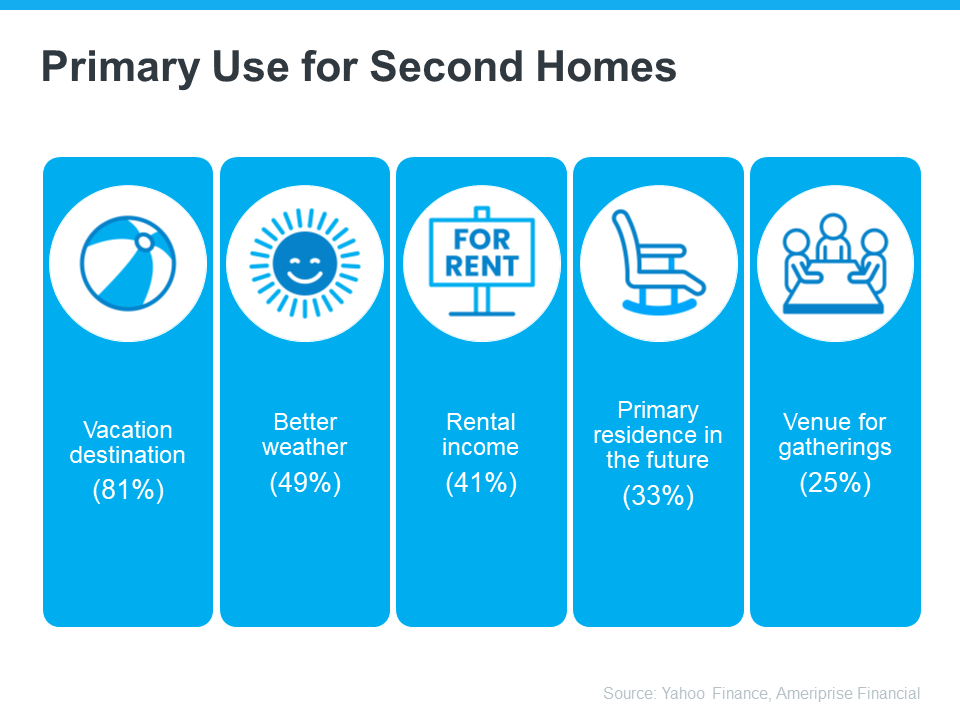

Summer is officially here and that means it’s the perfect time to start planning where you want to vacation and unwind this season. If you’re excited about getting away and having some fun in the sun, it might make sense to consider if owning your own vacation home is right for you.

An Ameriprise Financial survey sheds light on why people buy a second, or vacation, home (see below):

And you don’t have to be wealthy to buy a vacation home. Bankrate shares two tips for how to make this dream more achievable for anyone who’s interested:

If the idea of basking in the sun at your very own vacation home sounds appealing, you might want to start looking now. Summer's when everyone's trying to buy their slice of paradise, so it’s best to start early.

Your first move is to team up with a real estate agent. They know all the ins and outs of the area you want to be in, and which homes you should look at. Plus, they can give you the lowdown on everything you need to know about having a second home and how it can benefit you. The same article from Bankrate says:

“Buying real estate in a new area — or even one you’ve vacationed in for many years — requires expert guidance. That makes it a good idea to work with an experienced local lender who specializes in loans for vacation homes and a local real estate professional. Local lenders and Realtors will understand the required rules and specifics for the area you are buying, and a local Realtor will know what properties are available.”

If the idea of owning your own vacation home appeals to you, let’s chat.

If you’re considering selling your house on your own as a “For Sale by Owner” (FSBO), you want to think about if it’s really worth the extra stress. Going this route means shouldering a lot of responsibilities by yourself – and, if you’re not an expert, that opens the door for mistakes to happen and can quickly become overwhelming.

A report from the National Association of Realtors (NAR) shows two key areas where people who sold their own house struggled the most: pricing and paperwork.

Here are just a few of the ways an agent makes those tasks a whole lot easier.

Setting the right price for your house is important. And, if you’re selling your house on your own, two common issues can happen. You might ask for too much money (overpricing). Or you might not ask for enough (underpricing). Either can make it hard to sell your house. According to NerdWallet:

“When selling a home, first impressions matter. Your house’s market debut is your first chance to attract a buyer and it’s important to get the pricing right. If your home is overpriced, you run the risk of buyers not seeing the listing.

. . . But price your house too low and you could end up leaving some serious money on the table. A bargain-basement price could also turn some buyers away, as they may wonder if there are any underlying problems with the house.”

To avoid these problems, team up with a real estate agent. Agents know how to figure out the perfect price because they have a deep understanding of the local housing market. And they’ll use that expertise to set a price that matches what buyers are willing to pay, giving your house the best chance to impress from the start.

Selling a house involves a bunch of paperwork and legal documentation that has to be just right. There are a lot of rules and regulations to follow, and that makes it a bit tricky for homeowners to manage everything on their own. Without a pro by your side, you could end up facing liability risks and legal complications.

Real estate agents are experts in all the contracts and paperwork needed for selling a house. They know the rules and can guide you through it all, reducing the chance of mistakes that might lead to legal problems or delays. As an article from First American explains:

“To buy or sell a home you need to accurately complete a lot of forms, disclosures, and legal documents. A real estate agent ensures you cross every ‘t’ and dot every ‘i’ to help you avoid having a transaction fall through and/or prevent a costly mistake.”

So, instead of dealing with the growing pile of documents on your own, team up with an agent who can be your advisor, helping you avoid any legal bumps in the road.

Selling a house on your own can cost you a lot of time and stress. Let’s connect so you have help with all the finer details, including setting the right price, handling all the paperwork, and so much more. That way we can take that stress off of your plate.

Buyers face challenges in any market – and today’s is no different. With higher mortgage rates and rising prices, plus the limited supply of homes for sale, there’s a lot to consider.

But, there's one way to avoid getting tripped up – and that’s leaning on a real estate agent for the best possible advice. An expert’s insights will help you avoid some of the most common mistakes homebuyers are making right now.

As part of the homebuying process, a lender will look at your finances to figure out what they’re willing to loan you for your mortgage. This gives you a good idea of what you can borrow so you can really wrap your head around the financial side of things before you start looking at homes. While house hunting can be a lot more fun than talking about finances, you don’t want to do this out of order. Make sure you get your pre-approval first. As CNET explains:

“If you wait to get preapproved until the last minute, you might be scrambling to contact a lender and miss the opportunity to put a bid on a home.”

While you may have a long list of must-haves and nice-to-haves, you need to be realistic about your home search. Even though your ideal state is you find a home that checks every box, you may need to be willing to compromise – especially since inventory is still low. Plus, a home that has everything you want may be too pricey. As Investopedia puts it:

“When you expect to find the perfect home, you could prolong the homebuying process by holding out for something better. Or you could end up paying more for a home just because it meets all your needs.”

Instead, look for something that has most of your must-haves and good bones where you can add anything else you may need down the line.

With today’s mortgage rates and home prices, there’s no arguing it’s expensive to buy a home. And while it may be tempting to stretch your finances a bit further than you’re comfortable with to make sure you get the house, you want to avoid overextending your budget. Make sure you talk to your agent about how changing mortgage rates impact your monthly payment. Bankrate offers this advice:

“Focus on what monthly payment you can afford rather than fixating on the maximum loan amount you qualify for. Just because you can qualify for a $300,000 loan doesn’t mean you can comfortably handle the monthly payments that come with it along with your other financial obligations. Every borrower’s case is different, so factor in your whole financial profile when determining how much house you can afford.”

This last one may be the most important of all. Buying a home is a process that involves a lot of steps, paperwork, negotiation, and more. Rather than take all of this on yourself, it’s a good idea to have a pro working with you. The right agent will reduce your stress and help the process go smoothly. As CNET explains:

“Attempting to buy a home without a real estate agent makes the process more arduous than it needs to be. A real estate agent can give you professional legal guidance, market expertise and support, which will save you time, money and stress. They can also increase your chances of finding the right home so you don’t have to spend hours scouring the internet for listings.”

Mistakes can cost you time, frustration, and money. If you want to buy a home in today’s market, let’s connect so you have a pro on your side who can help you avoid these missteps.

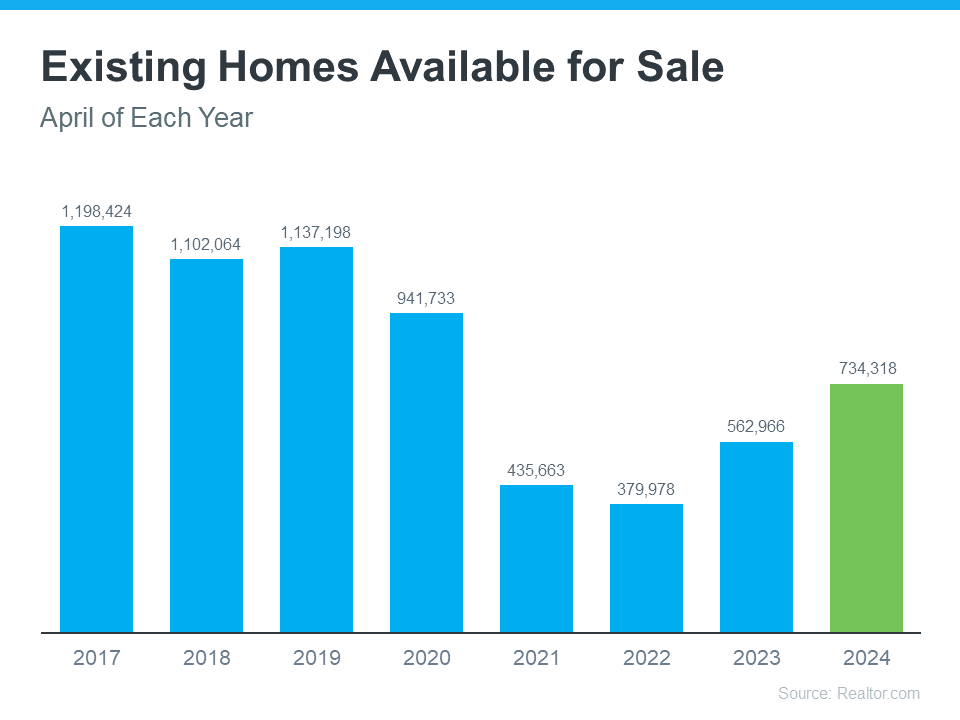

There’s no denying the last couple of years have been tough for anyone trying to buy a home because there haven’t been enough houses to go around. But things are starting to look up.

There are more homes up for grabs this year. The graph below uses the latest data from Realtor.com to show in April 2024 there were more homes for sale than there were over the last few years (2021-2023):

As Realtor.com explains:

“There were 30.4% more homes actively for sale on a typical day in April compared with the same time in 2023, marking the sixth consecutive month of annual inventory growth.”

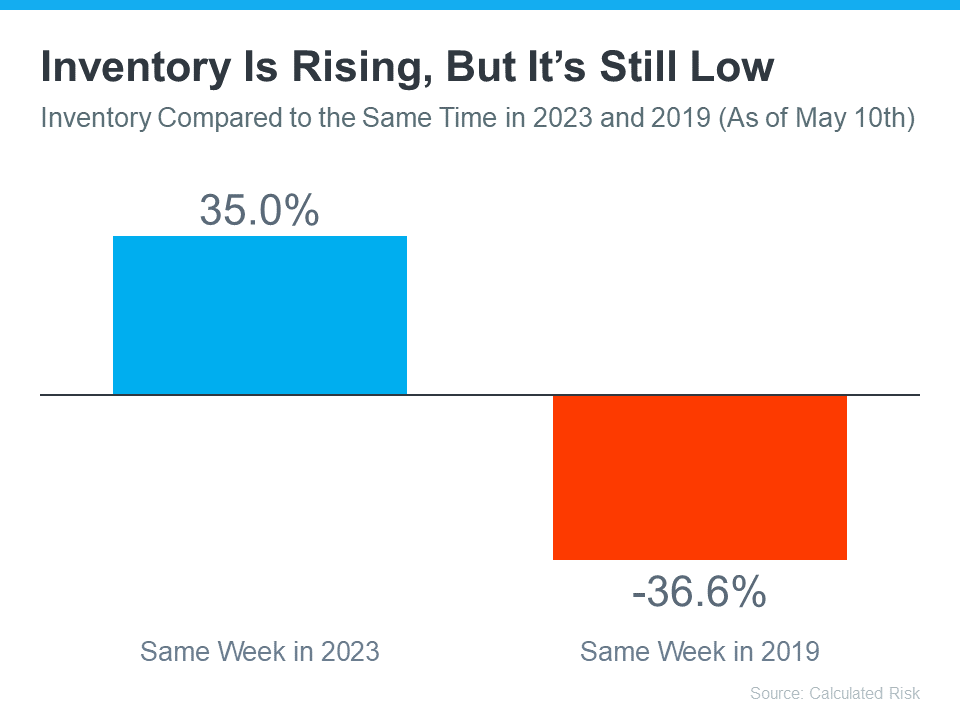

But does this growing inventory make house hunting easier? Yes and no.

Using the latest weekly data from Calculated Risk, the graph below shows, that even with the growth lately, there are still way fewer homes for sale than there were in the last normal year in the housing market:

If you’ve been looking to buy but put your plans on hold because you just couldn’t find what you were searching for, you might see more options now than you did over the past few years – but don't expect a huge selection.

To check out your growing options, it's a good idea to work with a local real estate agent you trust. Real estate is all about location. And an agent can help you get the scoop on the homes available in the area you're interested in. Bankrate explains:

“In today’s homebuying market, it’s more important than ever to find a real estate agent who really knows your local area — down to your specific neighborhood — and can help you successfully navigate its unique quirks.”

Let's team up so you have someone who can keep you in the loop on everything that might impact your move, like how many homes are up for sale right now.

Thinking about buying a home? While today’s mortgage rates might seem a bit intimidating, here are two solid reasons why, if you’re ready and able, it could still be a smart move to get your own place.

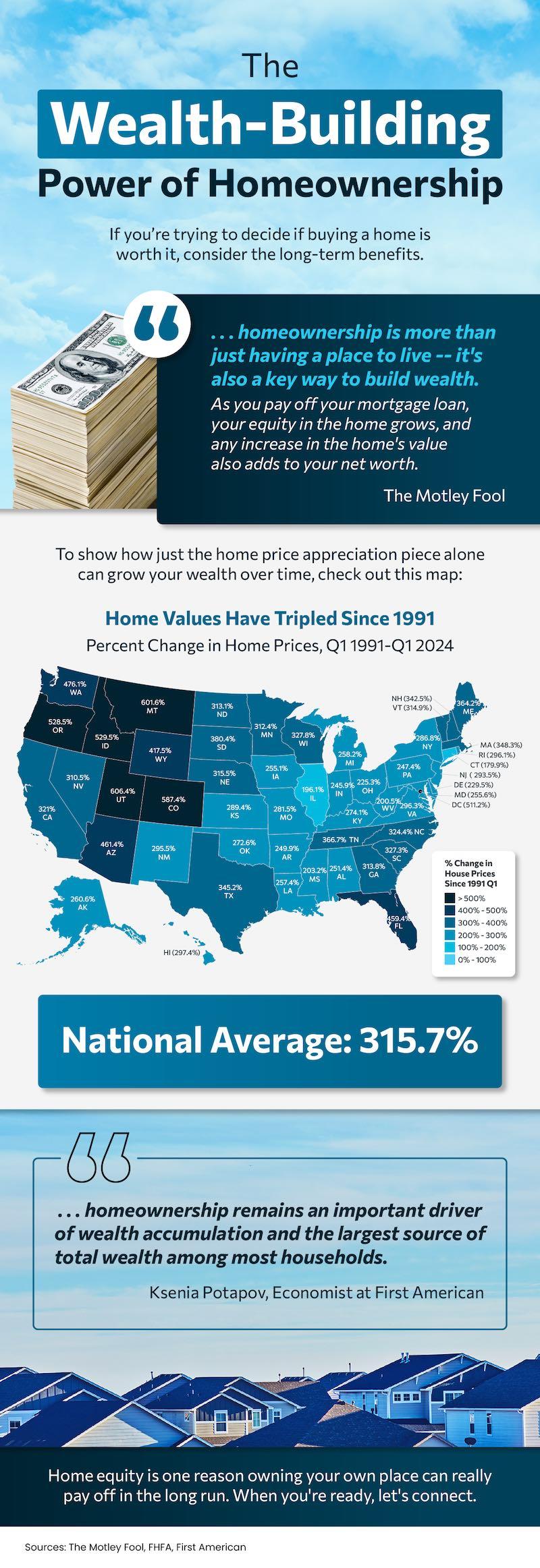

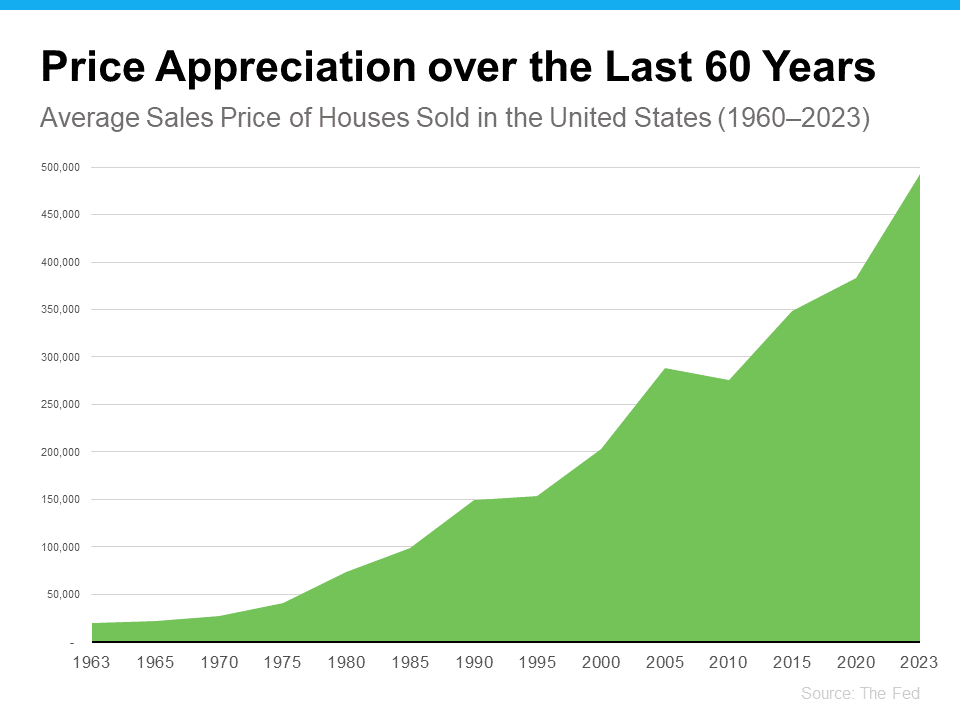

There’s been some confusion over the past year or so about which way home prices are headed. Make no mistake, nationally they’re still going up. In fact, over the long-term, home prices almost always go up (see graph below):

Using data from the Federal Reserve (the Fed), you can see the overall trend is home prices have climbed steadily for the past 60 years. There was an exception during the 2008 housing crash when prices didn't follow the normal pattern, but generally, home values kept rising.

This is a big reason why buying a home can be better than renting. As prices go up and you pay down your mortgage, you build equity. Over time, this growing equity can really increase your net worth. The Urban Institute says:

“Homeownership is critical for wealth building and financial stability.”

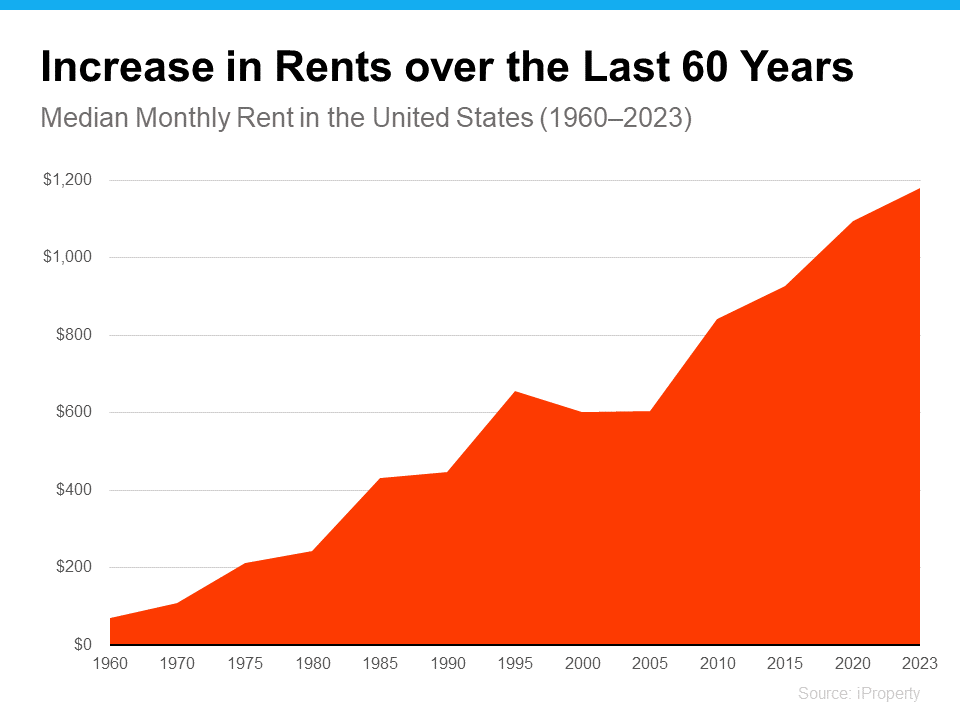

Here’s another reason you may want to think about buying a home instead of renting – rent just keeps going up over the years. Sure, it might be cheaper to rent right now in some areas, but every time you renew your lease or sign a new one, you’re likely to feel the squeeze of your rent getting higher. According to data from iProperty Management, rent has been going up pretty consistently for the last 60 years, too (see graph below):

So how do you escape the cycle of rising rents? Buying a home with a fixed-rate mortgage helps you stabilize your housing costs and say goodbye to those annoying rent increases. That kind of stability is a big deal.

Your housing payments are like an investment, and you've got a decision to make. Do you want to invest in yourself or keep paying your landlord?

When you own your home, you're investing in your own future. And even when renting is cheaper, that money you pay every month is gone for good.

As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), says:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

If you're tired of your rent going up and want to explore the many benefits of homeownership, let’s talk to explore your options.

If you’ve been a homeowner for at least a couple of years, keep reading.

Because that means you may be sitting on a solid amount of equity. And if so, there are a few different ways you can use it to fuel your next move.

Want to know what your equity might unlock for you?

If you’re thinking about buying a home, chances are you’ve got mortgage rates on your mind. You’ve heard about how they impact how much you can afford in your monthly mortgage payment, and you want to make sure you’re factoring that in as you plan your move.

The problem is, with all the headlines in the news about rates lately, it can be a bit overwhelming to sort through. Here’s a quick rundown of what you really need to know.

Rates have been volatile – that means they’re bouncing around a bit. And, you may be wondering, why? The answer is complicated because rates are affected by so many factors.

Things like what’s happening in the broader economy and the job market, the current inflation rate, decisions made by the Federal Reserve, and a whole lot more have an impact. Lately, all of those factors have come into play, and it’s caused the volatility we’ve seen. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

While you could drill down into each of those things to really understand how they impact mortgage rates, that would be a lot of work. And when you’re already busy planning a move, taking on that much reading and research may feel a little overwhelming. Instead of spending your time on that, lean on the pros.

They coach people through market conditions all the time. They’ll focus on giving you a quick summary of any broader trends up or down, what experts say lies ahead, and how all of that impacts you.

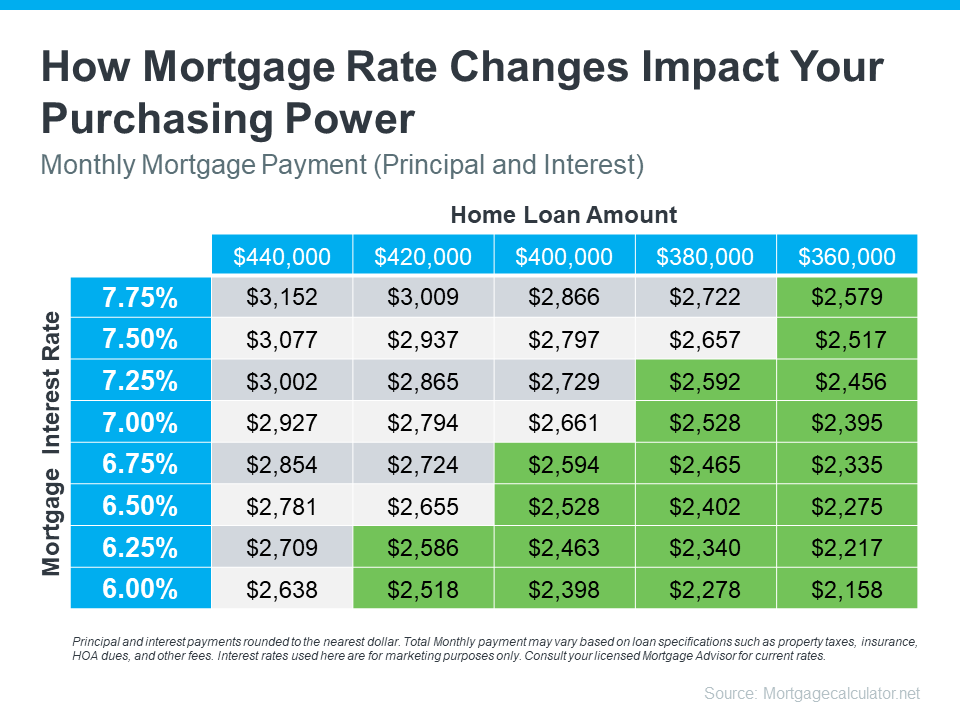

Take this chart as an example. It gives you an idea of how mortgage rates impact your monthly payment when you buy a home. Imagine being able to make a payment between $2,500 and $2,600 work for your budget (principal and interest only). The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

As you can see, even a small shift in rates can impact the loan amount you can afford if you want to stay within that target budget.

It’s tools and visuals like these that take everything that’s happening and show what it actually means for you. And only a pro has the knowledge and expertise needed to guide you through them.

You don’t need to be an expert on real estate or mortgage rates, you just need to have someone who is, by your side.

Have questions about what’s going on in the housing market? Let’s connect so we can take what’s happening right now and figure out what it really means for you.

Displaying blog entries 131-140 of 875