Keep Your Housing Perspective When Selling on Mt. Hood

Monday, October 31, 2022

Displaying blog entries 1-7 of 7

If you’re planning to buy a home, knowing what to budget for and how to save may sound scary at first. But it doesn’t have to be. One way to take the fear out of budgeting is understanding some of the costs you might encounter. And to do that, turn to trusted real estate professionals. They can help you plan your finances and prepare your budget.

Here are just a few costs experts say you can expect.

Saving for your down payment is likely top of mind as you set out to buy a home. But do you know how much you’ll need to save? While each situation is different, there’s a common misconception that putting 20% down toward your purchase is required. An article from the Mortgage Reports explains why that’s not always the case:

“The idea that you have to put 20% down on a house is a myth. . . . The right amount depends on your current savings and your home buying goals.”

To understand your options, partner with a trusted real estate professional to go over the various loan types, down payment assistance programs, and what each one requires.

Make sure you also budget for closing costs, which are a collection of fees and payments made to the various people involved in your transaction. Bankrate explains:

“Closing costs are the fees you pay when finalizing a real estate transaction, whether you’re refinancing a mortgage or buying a new home. These costs can amount to 2 to 5 percent of the mortgage so it’s important to be financially prepared for this expense.”

The best way to understand what you’ll need at the closing table is to work with a trusted lender. They can provide you with answers to the questions you might have.

If you want to cover all your bases, you can also consider saving for an earnest money deposit (EMD). An EMD is money you pay as a show of good faith when you make an offer on a house. According to realtor.com, it’s usually between 1% and 2% of the total home price.

This deposit works like a credit. It’s not an added expense – it’s paying a portion of your costs upfront. You’re using some of the money you already saved for your purchase to show the seller you’re committed and serious about their house. Realtor.com describes how it works as part of your sale:

“It tells the real estate seller you’re in earnest as a buyer, . . . . Assuming that all goes well and the buyer’s good-faith offer is accepted by the seller, the earnest money funds go toward the down payment and closing costs. In effect, earnest money is just paying more of the down payment and closing costs upfront.”

Keep in mind, an EMD isn’t required, and it doesn’t guarantee your offer will be accepted. It’s important to work with a real estate advisor to understand what’s best for your situation and any specific requirements in your area. They’ll help you determine what moves you should make in the homebuying process to have the greatest success.

Budgeting for your home purchase doesn’t have to be scary. Let’s connect so you’ll have an expert on your side to answer any questions you have along the way.

With all the headlines and talk in the media about the shift in the housing market, you might be thinking this is a housing bubble. It’s only natural for those thoughts to creep in that make you think it could be a repeat of what took place in 2008. But the good news is, there’s concrete data to show why this is nothing like the last time.

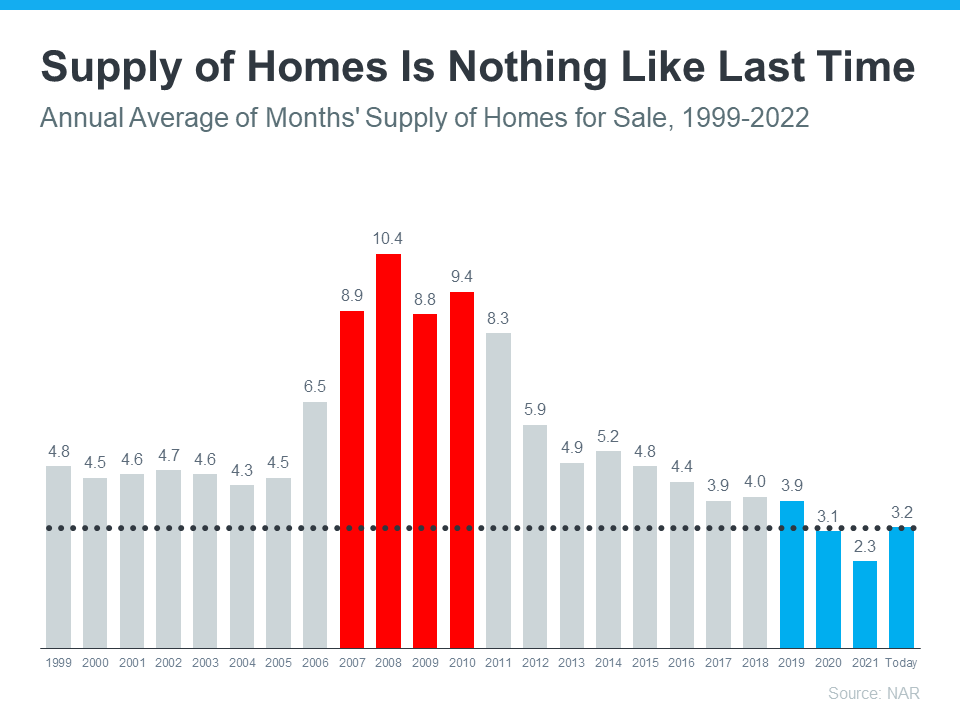

For historical context, there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), and that caused prices to fall dramatically. Supply has increased since the start of this year, but there’s still a shortage of inventory available overall, primarily due to almost 15 years of underbuilding homes.

The graph below uses data from the National Association of Realtors (NAR) to show how the months’ supply of homes available now compares to the crash. Today, unsold inventory sits at just a 3.2-months’ supply at the current sales pace, which is significantly lower than the last time. There just isn’t enough inventory on the market for home prices to come crashing down like they did last time, even though some overheated markets may experience slight declines.

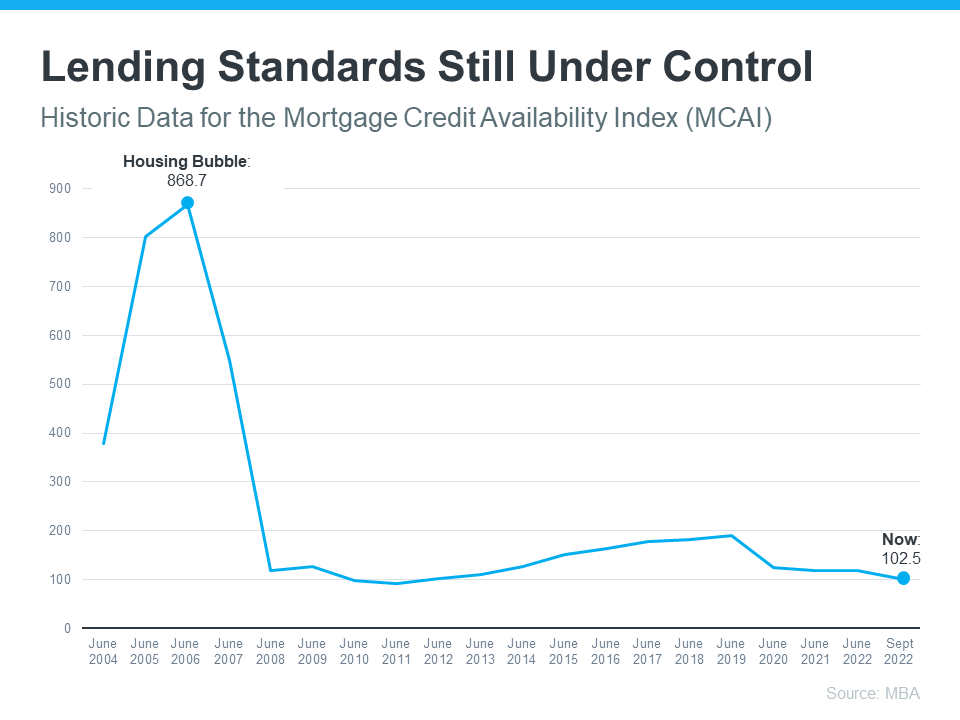

During the lead-up to the housing crisis, it was much easier to get a home loan than it is today. Running up to 2006, banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance their current home.

Back then, lending institutions took on much greater risk in both the person and the mortgage products offered. That led to mass defaults, foreclosures, and falling prices. Today, things are different, and purchasers face much higher standards from mortgage companies.

The graph below uses Mortgage Credit Availability Index (MCAI) data from the Mortgage Bankers Association (MBA) to help tell this story. In that index, the higher the number, the easier it is to get a mortgage. The lower the number, the harder it is. In the latest report, the index fell by 5.4%, indicating standards are tightening.

This graph also shows just how different things are today compared to the spike in credit availability leading up to the crash. Tighter lending standards over the past 14 years have helped prevent a scenario that would lead to a wave of foreclosures like the last time.

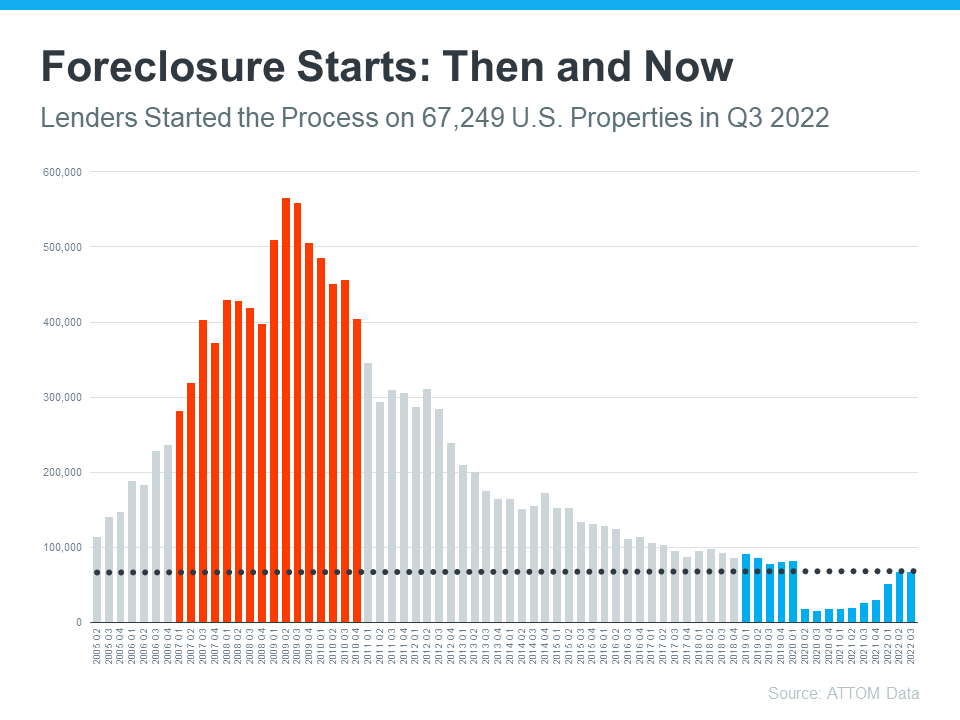

Another difference is the number of homeowners that were facing foreclosure after the housing bubble burst. Foreclosure activity has been lower since the crash, largely because buyers today are more qualified and less likely to default on their loans. The graph below uses data from ATTOM Data Solutions to help paint the picture of how different things are this time:

Not to mention, homeowners today have options they just didn’t have in the housing crisis when so many people owed more on their mortgages than their homes were worth. Today, many homeowners are equity rich. That equity comes, in large part, from the way home prices have appreciated over time. According to CoreLogic:

“The total average equity per borrower has now reached almost $300,000, the highest in the data series.”

Rick Sharga, Executive VP of Market Intelligence at ATTOM Data, explains the impact this has:

“Very few of the properties entering the foreclosure process have reverted to the lender at the end of the foreclosure. . . . We believe that this may be an indication that borrowers are leveraging their equity and selling their homes rather than risking the loss of their equity in a foreclosure auction.”

This goes to show homeowners are in a completely different position this time. For those facing challenges today, many have the option to use their equity to sell their house and avoid the foreclosure process.

If you’re concerned we’re making the same mistakes that led to the housing crash, the graphs above should help alleviate your fears. Concrete data and expert insights clearly show why this is nothing like the last time.

Hit the Brakes! Rapid River Retreat on the Sandy River is one of Mt. Hood's best vacation rentals for over ten years. Nearly two acres of waterfront with three bedroom, two bath home. Soaring ceilings and natural light. Great room with gourmet kitchen, granite counter tops and wet bar. Cozy wood stove insert to warm your toes after a day on the slopes or hiking in the Mt. Hood National Forest up the street. Hop out to the covered hot tub overlooking the river. Secluded location on private gated road. Turn key! Perfect full time or second home too, 1 hour to PDX!!

$949,000

.jpg)

.jpg)

.jpeg)

.jpeg)

.jpeg)

.JPG)

Does the latest news about the housing market have you questioning your plans to sell your house? If so, perspective is key. Here are some of the ways a trusted real estate professional can explain the shift that’s happening today and why it’s still a sellers’ market even during the cooldown.

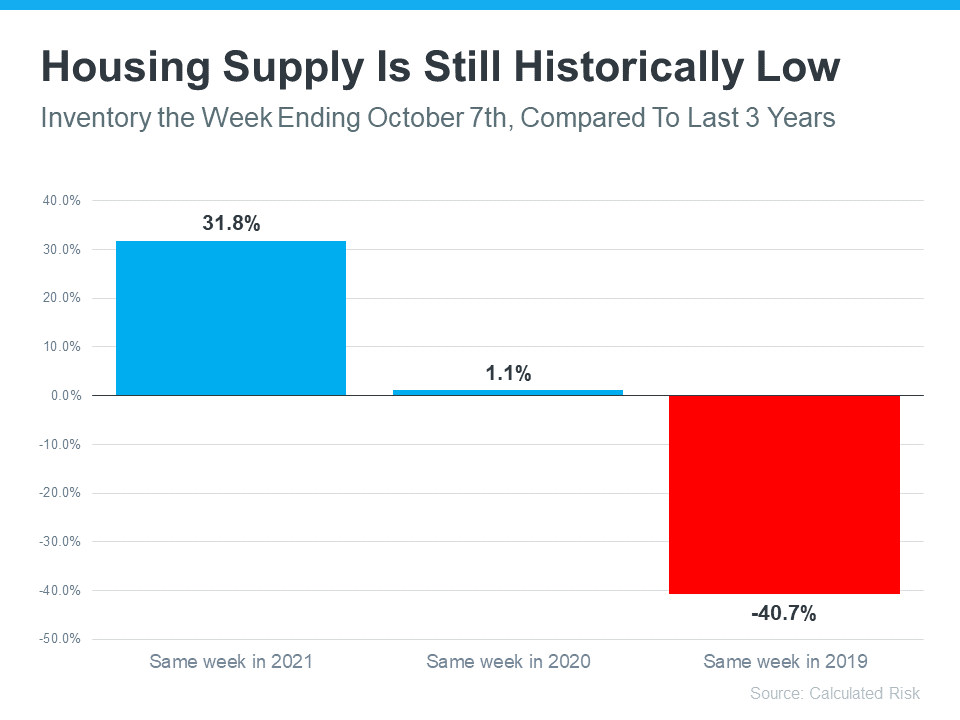

While the supply of homes available for sale has increased this year compared to last, we’re still nowhere near what’s considered a balanced market. A recent article from Calculated Risk helps put this year’s increased inventory into context (see graph below):

It shows supply this year has surpassed 2021 levels by over 30%. But the further back you look, the more you’ll understand the big picture. Compared to 2020, we’re just barely above the level of inventory we saw then. And if you go all the way back to 2019, the last normal year in real estate, we’re roughly 40% below the housing supply we had at that time.

Why does this matter to you? When inventory is low, there is still demand for your house because there just aren’t enough homes available for sale.

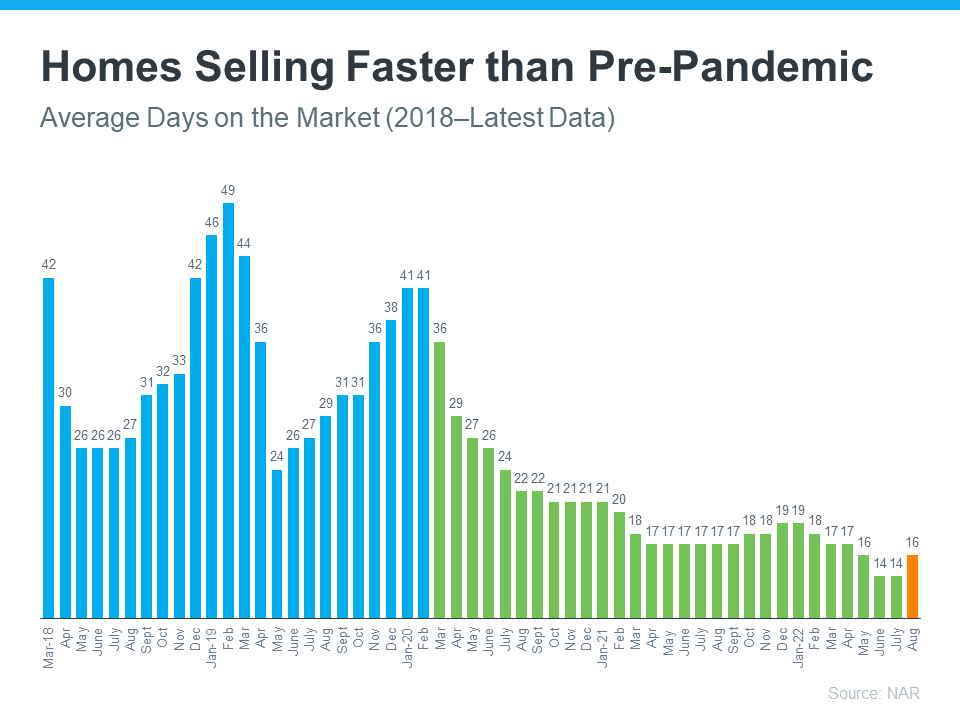

And while homes aren’t selling as quickly as they did a few months ago, the average number of days on the market is still well below pre-pandemic norms – in large part because inventory is so low. The graph below uses data from the Realtors’ Confidence Index by the National Association of Realtors (NAR) to illustrate this trend:

As the graph shows, the pre-pandemic numbers (shown in blue) are higher than the numbers we saw during the pandemic (shown in green). That’s because the average days on the market started to decrease as homes sold at record pace during the pandemic. Most recently, due to the cooldown in the housing market, the average days on the market have started to tick back up slightly (shown in orange) but are still far below the pre-pandemic norm.

What does this mean for you? While it may not be as fast as it was a couple of months ago, homes are still selling much faster than they did in more normal, pre-pandemic years. And if you price it right, your home could still go under contract quickly.

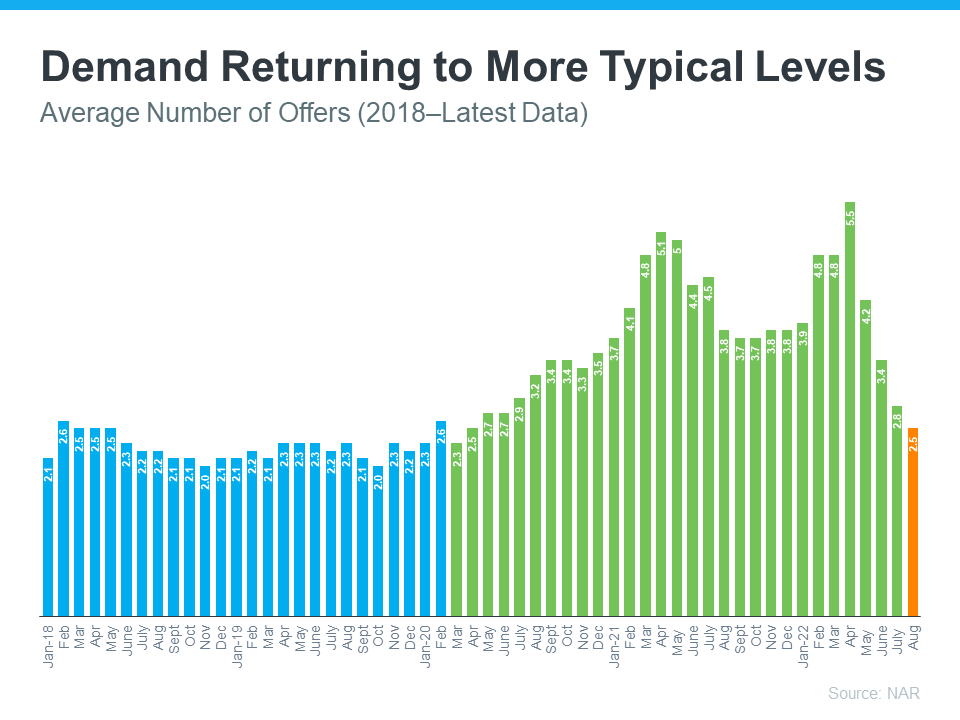

Buyer demand has softened this year in response to rising mortgage rates. But again, perspective is key. Getting 3-5 offers like sellers did during the pandemic isn’t the norm. The graph below uses data from NAR going back to 2018 to help tell the story of this shift over time (see graph below):

Prior to the pandemic, it was typical for homes sold to see roughly 2-2.5 offers (shown in blue). As the market heated up during the pandemic, the average number of offers skyrocketed as record-low mortgage rates drove up demand (shown in green). But most recently, the number of offers on homes sold today (shown in orange) has started to return to pre-pandemic levels as the market cools from the frenzy.

What’s the takeaway for you? Buyer demand has moderated from the pandemic peak, but it hasn’t disappeared. The buyers are still out there, and if you price your house at current market value, you’ll still be able sell your house today.

If you have questions about selling your house in today’s housing market, let’s connect. That way you have context around what’s happening now, so you’re up to date on what you can expect when you’re ready to move.

The housing market is rapidly changing from the peak frenzy it saw over the past two years. That means you probably have questions about what your best move is if you’re thinking of buying or selling this fall.

To help you make a confident decision, lean on the professionals for insights. Here are a few things experts are saying about the fall housing market.

A recent article from realtor.com:

“This fall, a more moderate pace of home selling, more listings to choose from, and softening price growth will provide some breathing room for buyers searching for a home during what is typically the best time to buy a home.”

Michael Lane, VP and General Manager, ShowingTime:

“Buyers will continue to see less competition for homes and have more time to tour homes they like and consider their options.”

Selma Hepp, Interim Lead of the Office of the Chief Economist, CoreLogic:

“. . . record equity continues to provide fuel for housing demand, particularly if households are relocating to more affordable areas.”

Danielle Hale, Chief Economist, realtor.com:

“For homeowners deciding whether to make a move this year, remember that listing prices – while lower than a few months ago – remain higher than in prior years, so you're still likely to find opportunities to cash-in on record-high levels of equity, particularly if you've owned your home for a longer period of time.”

Mortgage rates, home prices, and the supply of homes for sale are top of mind for buyers and sellers today. And if you want the latest information for our area, let’s connect today.

Displaying blog entries 1-7 of 7