The Best February for New Listings in 4 Years

Tuesday, March 31, 2026

Add Comment

Displaying blog entries 1-10 of 1996

There’s a lot of noise out there right now about investors in the housing market.

Some headlines make it sound like big Wall Street firms are buying up everything in sight. And if you’re trying to purchase a home yourself, that can make it feel like the odds are stacked against you.

But when you take a closer look at the data, a very different picture starts to come into focus.

For starters, when you hear the word investor, you probably picture big corporations. And that misconception is a large part of what’s feeding into the myth that they’re buying up all the homes.

Most investors aren’t big companies, at all.

They’re everyday people just like you.

They’re someone who owns a second home (like a vacation house at the river), a neighbor who has 1 or 2 rentals, or even a homeowner who tried to sell their home, didn’t get the price they wanted, and decided to rent it instead.

And when all of these groups are lumped together in the headlines, the number of investors sounds high – especially if you’re operating under the assumption all investors are big investors.

But here’s what the numbers really show when you drill down.

Large institutional investors, those big companies buying homes, actually make up a very small share of the overall housing market.

According to BatchData, the largest investors (those with 1,000+ homes) own just 0.4% of the 86 million single-family homes in the country. And their share of the market is actually shrinking.

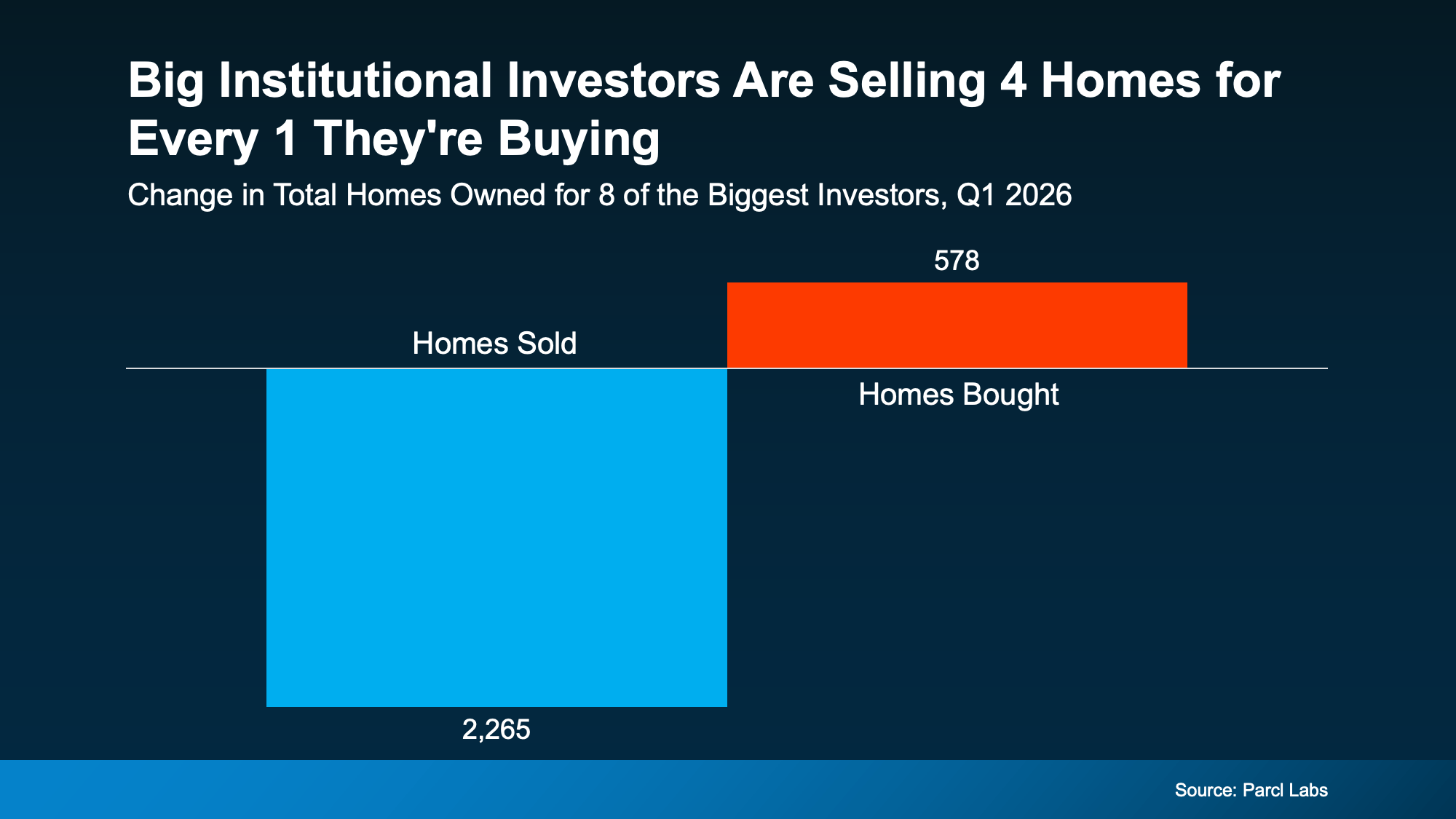

Data from Parcl Labs shows big investors are selling 4 homes for every 1 they’re buying right now (see visual below):

That means they’ve actually added almost 1.7k homes back into the market lately.

That means they’ve actually added almost 1.7k homes back into the market lately.

The story is clear. Instead of aggressively buying up homes, most of these companies are stepping back, which means less competition from them than you might expect. If you were someone who thought they were dominating the market, let that give you some peace of mind.

Most of the competition you’ll face is from other everyday buyers – people just like you. And with most large investors stepping back, there may be more opportunity in the market than you think.

It’s easy to assume big investors are taking over the housing market, but the data tells a different story. If you want an expert's opinion on what investor activity looks like in our area, let's talk.

Because odds are, it’s not as big a factor as you may think.

$695,000

Still Creek Cabin

| This turnkey Mt. Hood National Forest cedar log sided cabin on Still Creek comes along once in a blue moon. The mountain’s most popular waterfront location is a rare find. It comes fully furnished and completely updated to balance lodge like charm with modern amenities. Knotty cedar walls, vaulted ceilings, and wood beams in the great room highlight the river rock fireplace and walls of windows that showcase Still Creek views!The charming getaway has been remodeled and upgraded to perfection from the new metal roof, new flooring, new lighting, new windows, new electrical service and panels, new leather furniture, and new septic. Turn key and ready to go for summer and winter fun. Spread out and bring your friends. Plenty of parking too with two driveway entrances and half circular graveled driveway. There’s spacious room with three bedrooms, a hideaway kids loft plus two and a half baths. Bedrooms feature log beds with matching nightstands and new window treatments throughout. A huge deck off the great room is perfection for summer barbecues and stunning views of Still Creek and the forest. One big bonus is the easy access to the water for kid and dog friendly wading and swimming. The clearest waterway on the mountain makes watching the salmon spawn in the fall a treat. Comfort is guaranteed year-round with forced-air electric heat and a toe warming wood stove. Gas generator included in case the power happens to go out!Your Mt. Hood basecamp is the perfect spot to enjoy hiking, skiing and mountain biking. Only 15 minutes to the slopes. Mountain bike to Trillium Lake out your front door along with hiking trails too. Keep your mountain toys in the log sided outbuilding for easy storage. This super convenient location has two access roads off Highway 26 and is close to stores, coffee shops and restaurants. It’s a quick hour from Portland yet you feel a million miles away. |

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

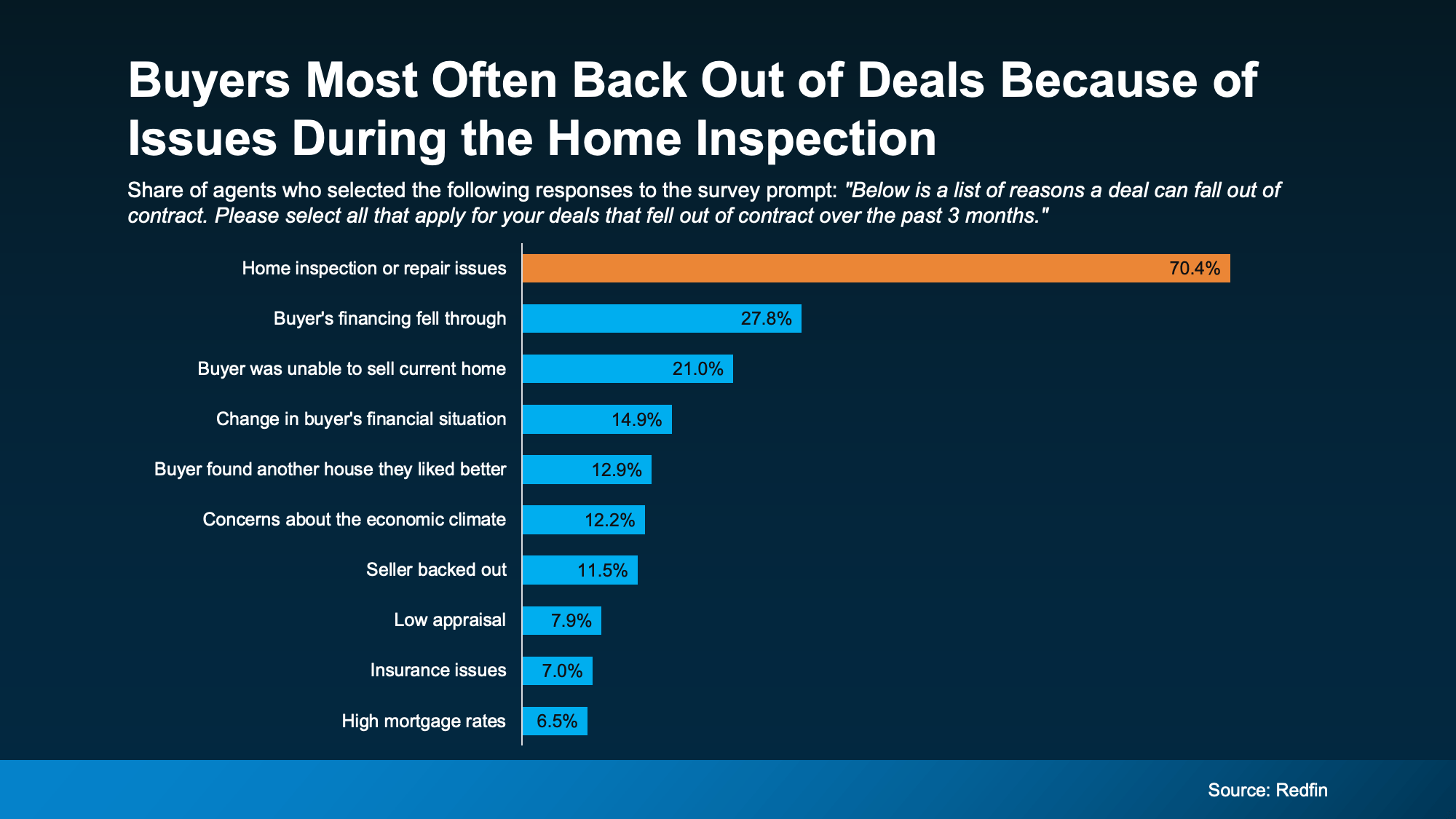

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They'll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

But remember, you don't have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, let's connect so we can keep your sale on track from day one.

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They'll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

But remember, you don't have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, let's connect so we can keep your sale on track from day one.

Homeowners looking to sell usually want three things: plenty of interested buyers, strong offers, and a short timeline. Spring is the season that most often delivers all three.

So, if a move has been on your mind this year, this is the window where momentum tends to work in your favor. Here’s what makes this season so powerful for sellers.

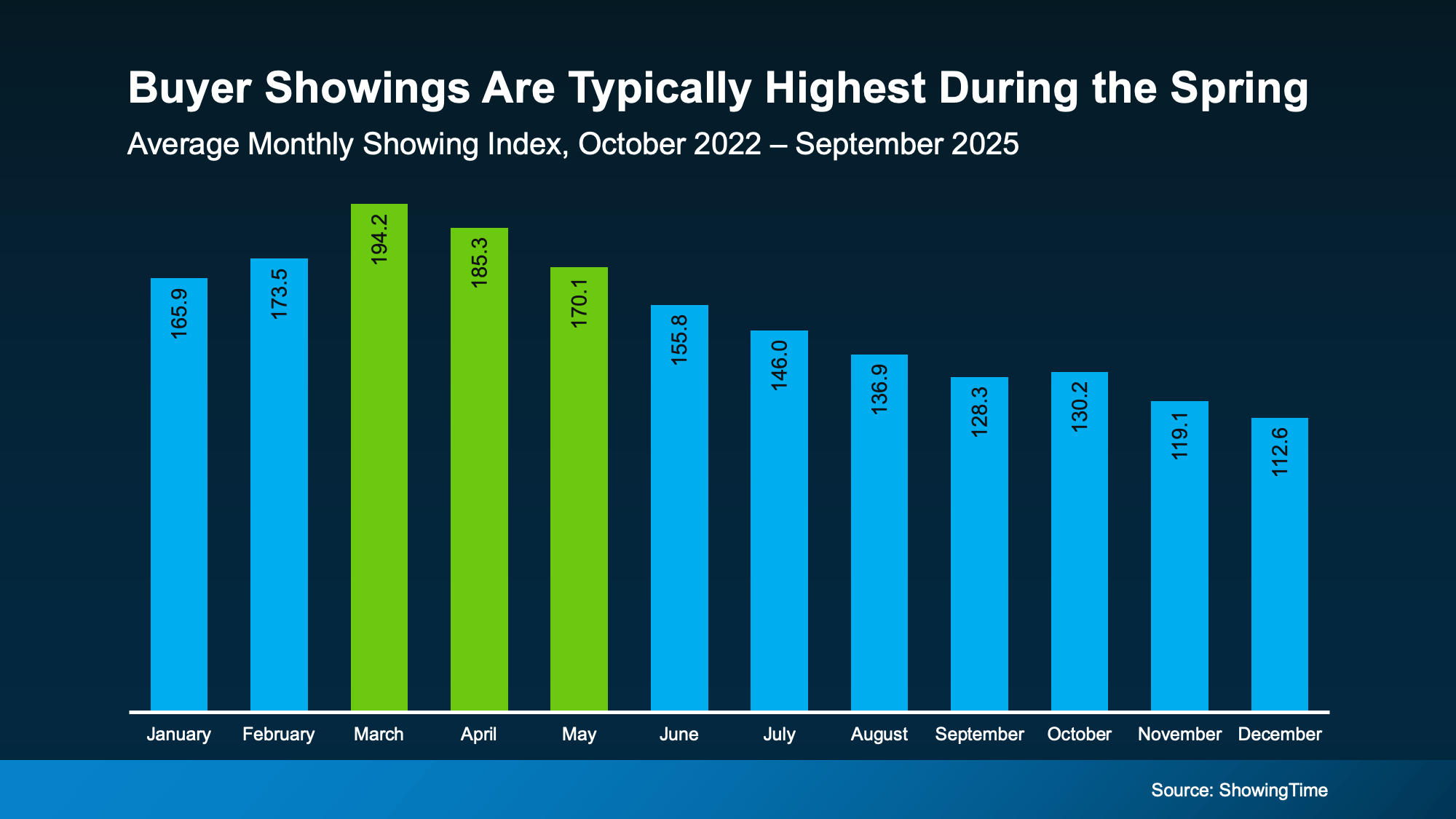

Typically speaking, in the housing market, there’s no more popular time to move than the Spring. Historically, data coming out of ShowingTime proves that’s when buyer activity peaks each year. Take a look for yourself (see graph below):

And this year, there’s more than just the seasonal trend working in your favor. Mortgage rates are also sitting near 3-year lows – and that combination matters.

And this year, there’s more than just the seasonal trend working in your favor. Mortgage rates are also sitting near 3-year lows – and that combination matters.

More buyers + improving affordability = more eyes on your house.

That doesn’t mean the market will return to the frenzy of the pandemic – far from it. But it does mean more buyers will be ready to re-enter the market. And that’s good for you. As Redfin says:

“Homebuying demand is improving . . . and mortgage-purchase applications are sitting near their highest level in three years. . ."

You should make sure your house is listed so you can take advantage of the uptick in demand. Because more activity means one thing: more opportunity to get a deal done.

With more buyer demand, it makes sense that you may get more offers on your house. And history shows that’s usually true.

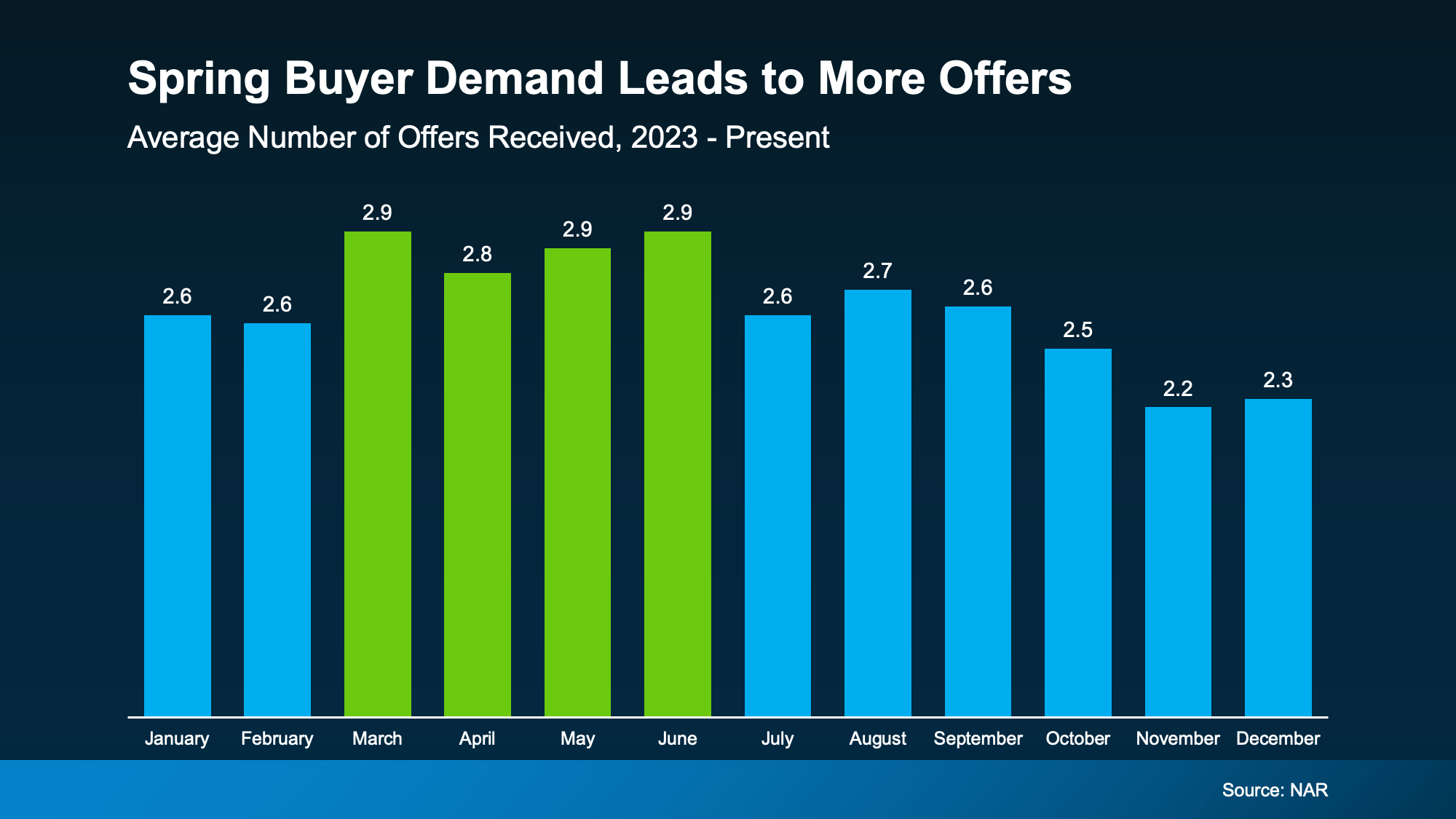

If we look at the data for the last three years from the National Association of Realtors (NAR), and take the averages for each month, it’s clear sellers in the Spring get more offers (see graph below):

Now, don’t expect the excessive bidding wars that were so famous in 2020 and 2021. But it does mean, seasonality could help you out this Spring. As Realtor.com explains:

Now, don’t expect the excessive bidding wars that were so famous in 2020 and 2021. But it does mean, seasonality could help you out this Spring. As Realtor.com explains:

“Spring typically brings out more buyers who are ready to make a move before summer. Listings see more views, showings, and offers during this season.”

And that could be really good for your bottom line.

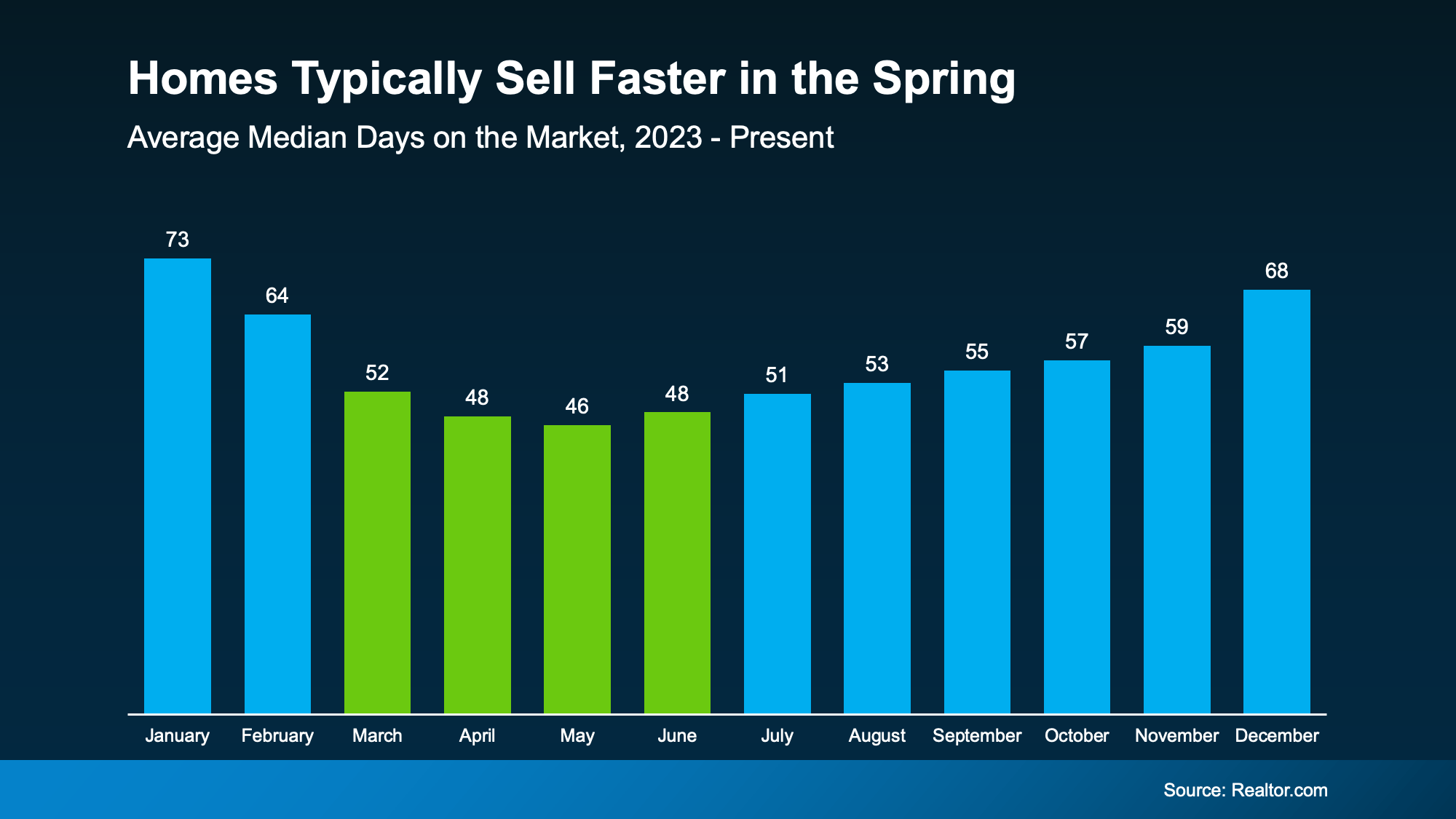

There’s one more predictable pattern that happens pretty much every Spring based on research from Realtor.com. Homes sell faster (see graph below):

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that's a difference you can feel.

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that's a difference you can feel.

Since homes have been taking longer to sell lately, listing your house during what’s usually the most active time of the year means you’re setting yourself up to move as quickly as possible. And isn’t that what sellers really want?

The faster your home sells, the earlier you can move on to what’s next for you.

If you’re eager to go on to your next chapter, need to downsize, or you’ve run out of space, Spring may be your best time to sell.

Spring doesn’t guarantee a sale. Strategy still matters. But this season gives you something valuable: momentum.

More buyers. More activity. More opportunity.

The real question is: if you’re going to sell this year, why not do it when the odds are in your favor?

Let’s talk about what selling this season could mean for your house and your timeline.

You’ve probably seen posts on social media talking about how “home prices are falling.” And when you see something like that, it’s normal to wonder:

Is this the start of a crash?

What does this mean for my house?

Let’s clear this up right away. This is not a crash. And your home is not suddenly losing a lot of value.

Here’s what often gets left out of what you’re seeing online. While some markets are experiencing slight declines, they’re the minority. Most places are still seeing prices rise or at the very least, hold steady.

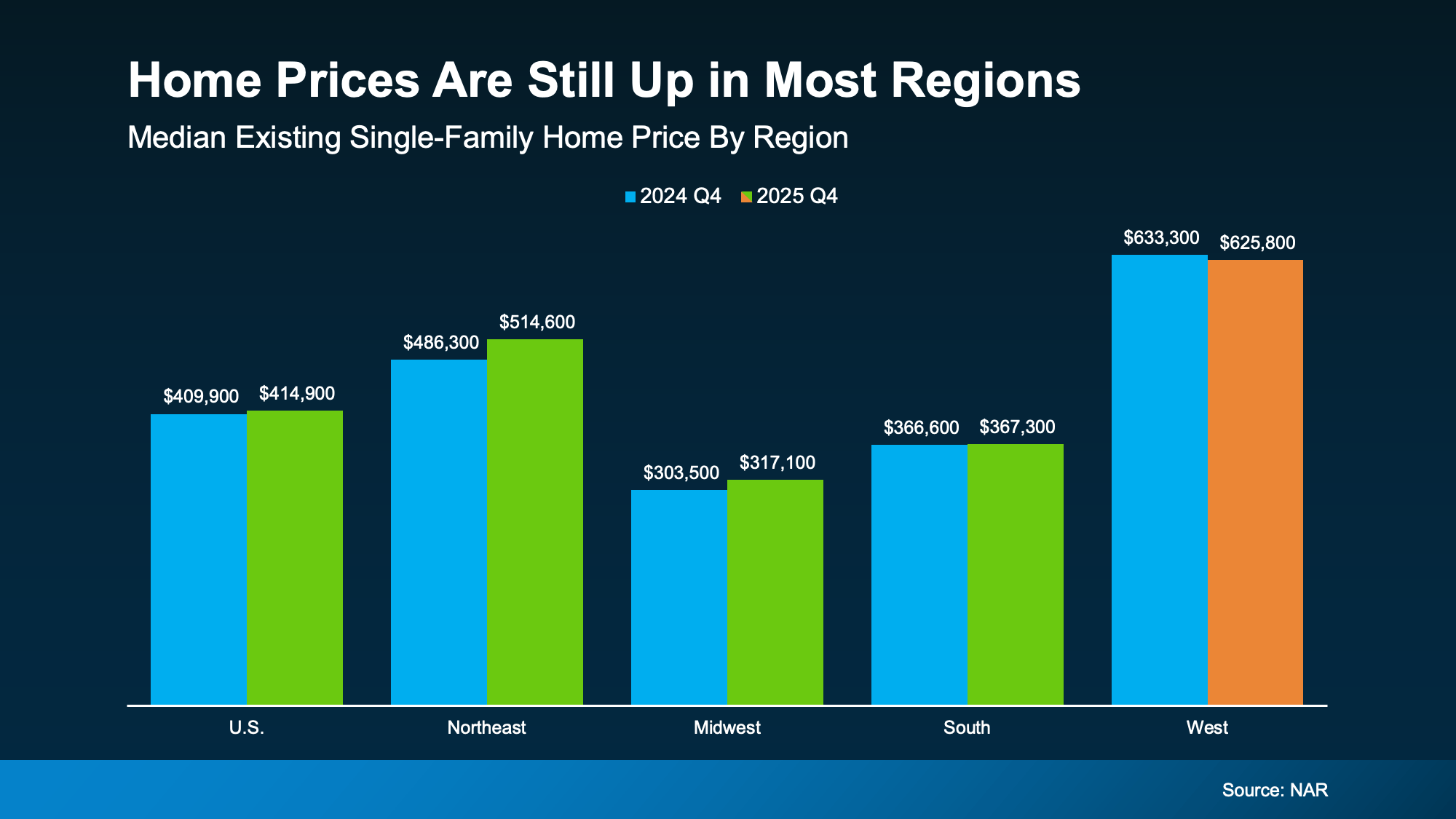

That’s why, at the national level, home prices are still rising, just at a slower pace. According to the National Association of Realtors (NAR):

“Home prices continued to rise in the fourth quarter of 2025. National median prices rose 1.2% year over year to $414,900.”

That’s not the rapid growth of a few years ago, but it’s not a downturn either. And just to really drive this home, here’s a look at the data from NAR at a regional level, so you can see that the negative narrative spun up online isn’t the whole truth (see graph below):

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

There is no wave of falling prices across the country. Instead, there are just a few pockets adjusting after several years of what’s typically considered unsustainable or exponential growth.

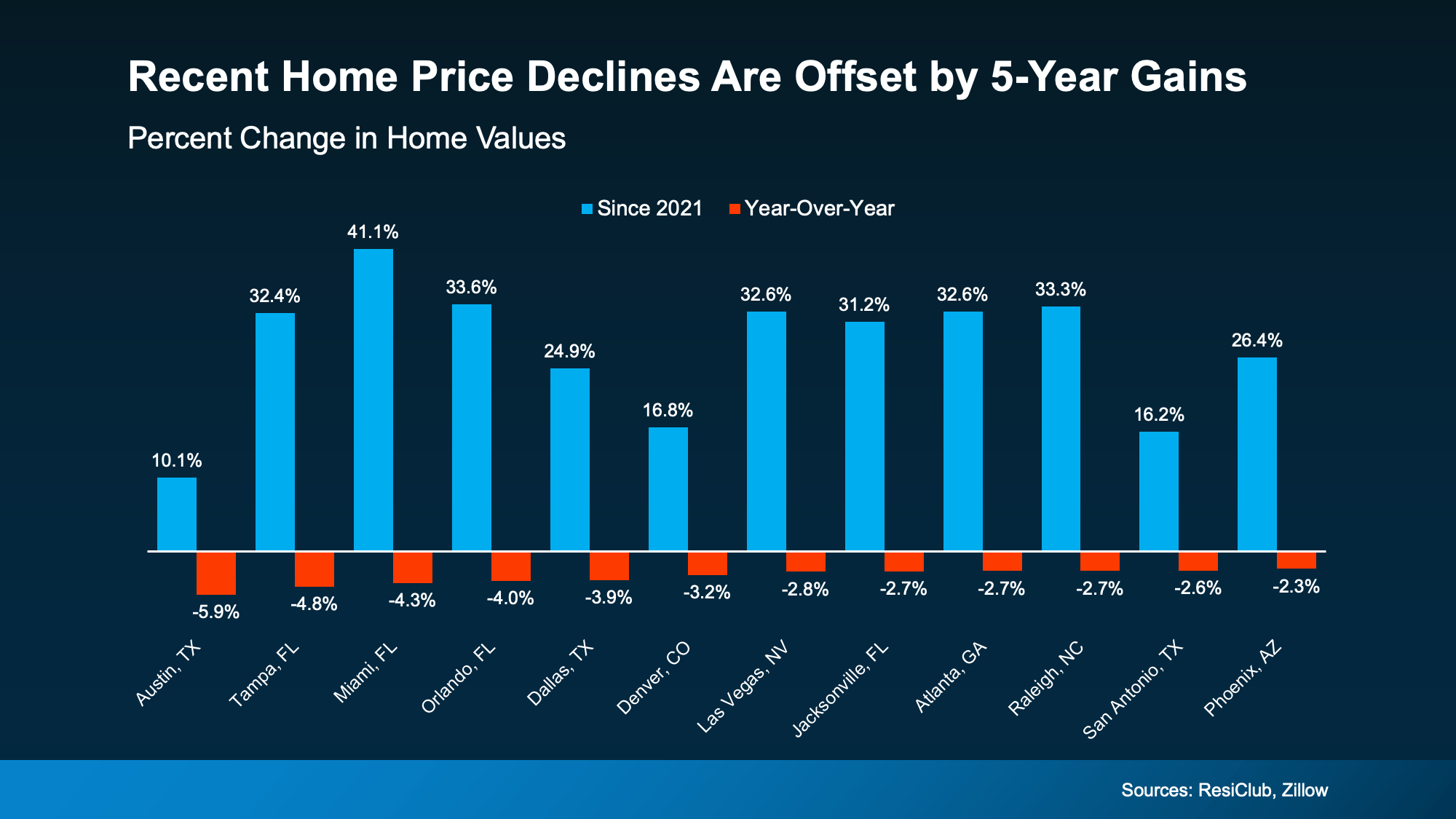

Okay, but what about the places where prices have declined? According to ResiClub and Zillow, that’s not a cause for major concern. When you zoom out and look at those same markets over the past five years, the story changes (see graph below):

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

Online chatter tends to shine a spotlight on the few areas that are down. But the bigger picture shows most homeowners are still in a very strong position.

Of course, every market, and every home, is different. But broadly speaking, home values are holding steady. And this isn’t a sign of widespread trouble in the market.

Despite what you may be seeing online, home prices are rising or holding steady in most parts of the country.

If you’re curious what your home is worth today, let’s take a look at the numbers together. Because context, and local expertise, matter more than what you’re seeing online.

There’s one number that decides how your sale goes before buyers ever step inside your home – and that’s your asking price.

Set it too high, and your house sits while buyers scroll past it.

But set it too low and you’ll leave real money on the table.

Here’s the problem. A lot of homeowners are basing their number on an online home value tool. And that’s where things can go sideways.

Displaying blog entries 1-10 of 1996