December Newsletter for Mt. Hood Real Estate

In case you missed this:

HAPPY NEW YEAR!

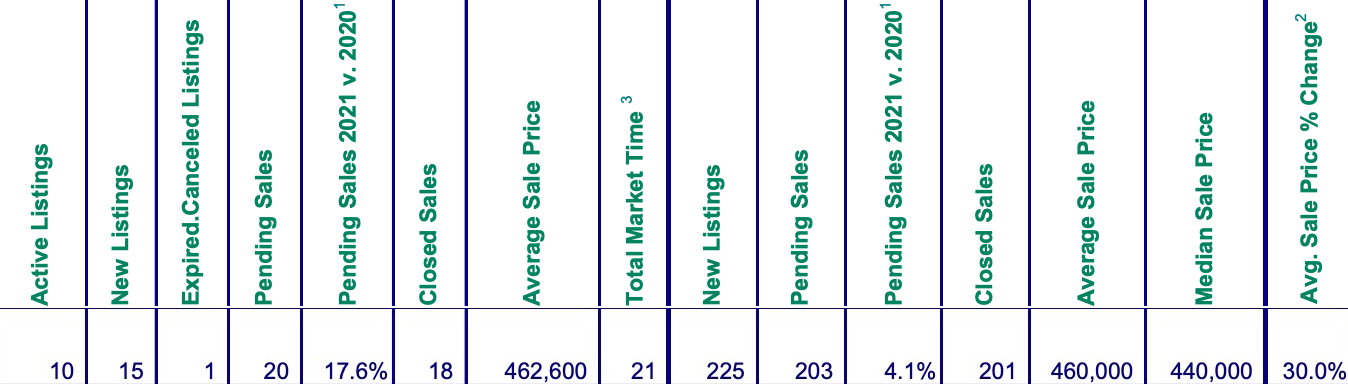

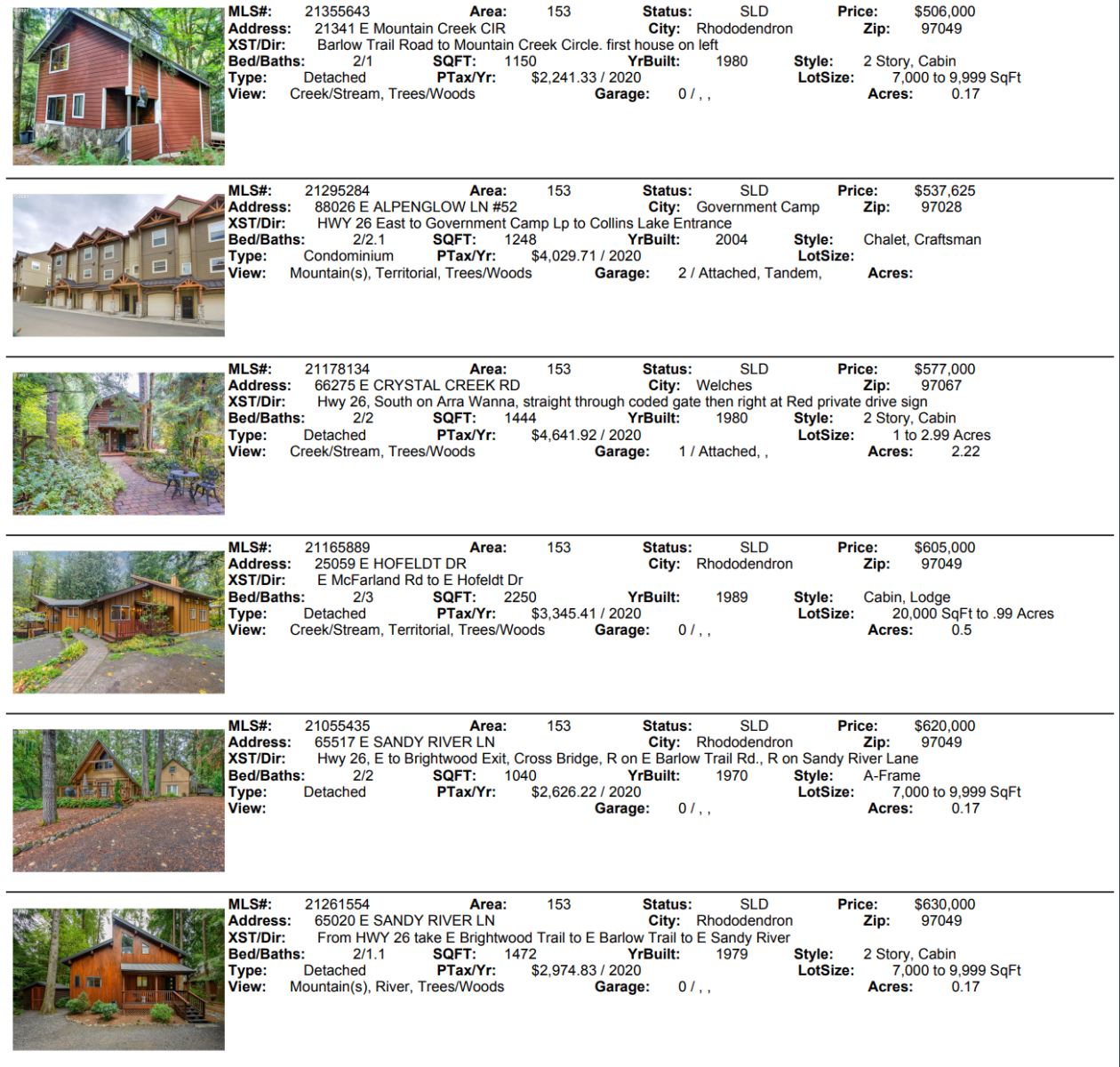

These are interesting times for Mt. Hood real estate as we head into 2022. After reviewing Novembers final sales we see a total of 18 closing with six sales under $400,000. Timberline Rim, one of the mountains most affordable subdivisions, saw five sales with three over a half a million dollars! November also produced the first $500,000 forest service cabin sale! More "off the chart" record breaking numbers were in Collins Lake at Government Camp. Three units have sold since July for $537,000, $557.000 and one at $606,000.

Needless to say, nearly every property that hits the market has five or more offers on the table making this the most amazing sellers market in Mt. Hood history. Two thousand twenty two will be very interesting if we don't get more inventory soon. Currently there are seven properties for sale and three are over a million dollars.

Recent snows may have slowed buyers down a little bit but the bottom line is once the current eleven pending sales close we will be down to nearly zero properties. Who knows what next year will look like at this point. This year we had a 30% increase in prices which was probably the greatest of all the areas tracked in our multiple listing. No doubt about it, Mt. Hood is the place to be!

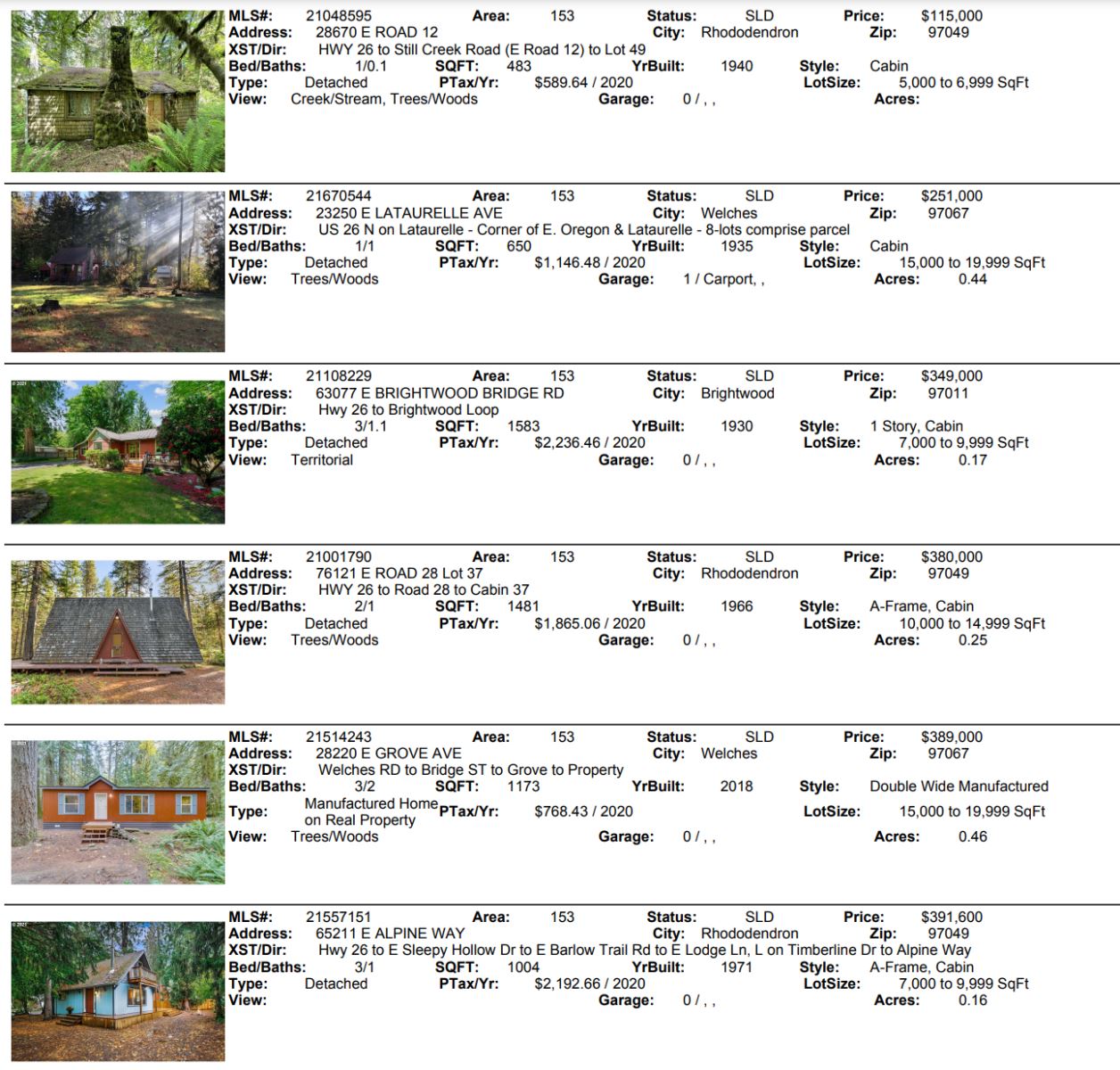

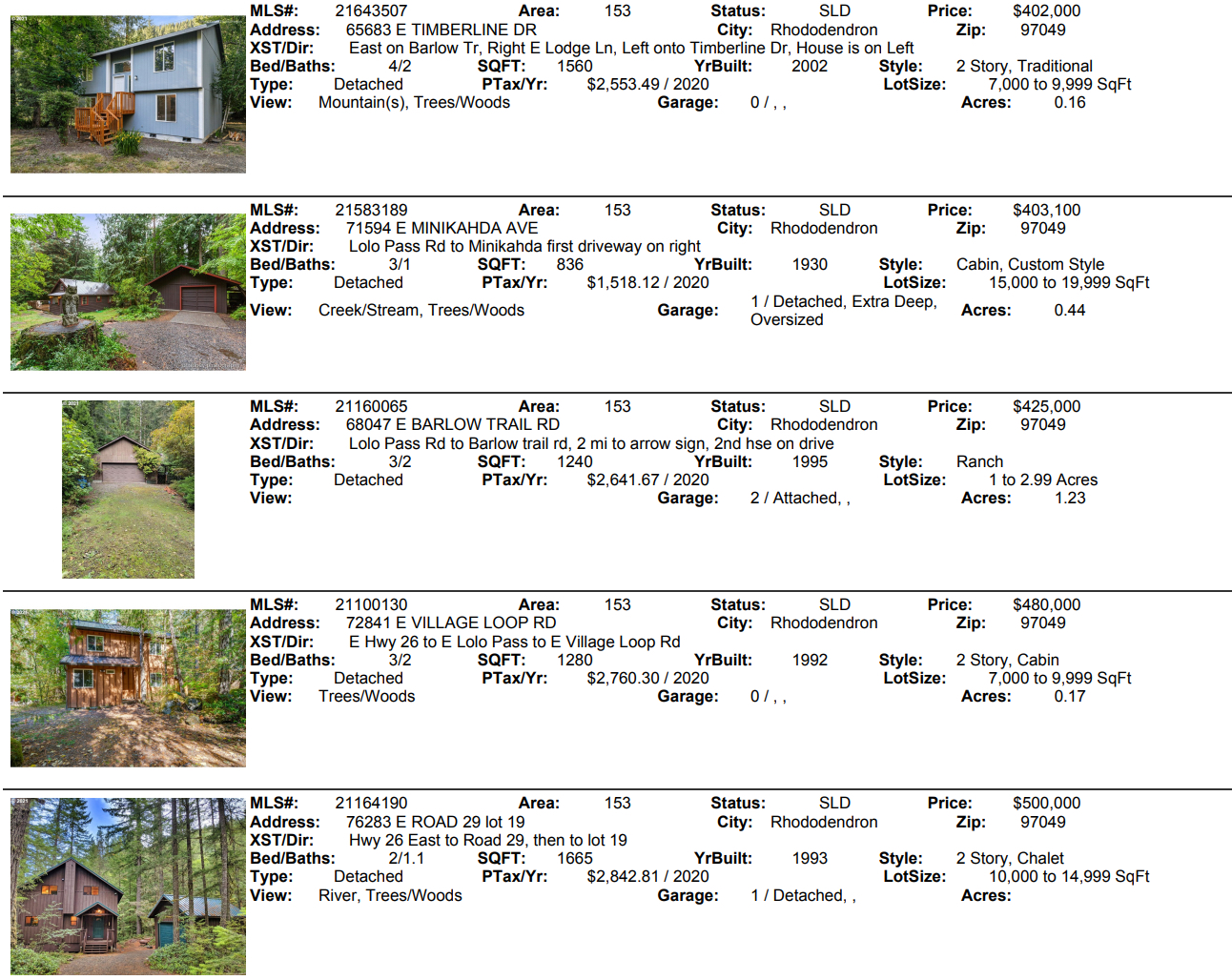

Listed below are Novembers closed sales in Brightwood, Welches, Rhododendron and Government Camp.

December National News

U.S. Real Estate Overview

Note: November 2021 data below are the most recent released by the National Association of Realtors.

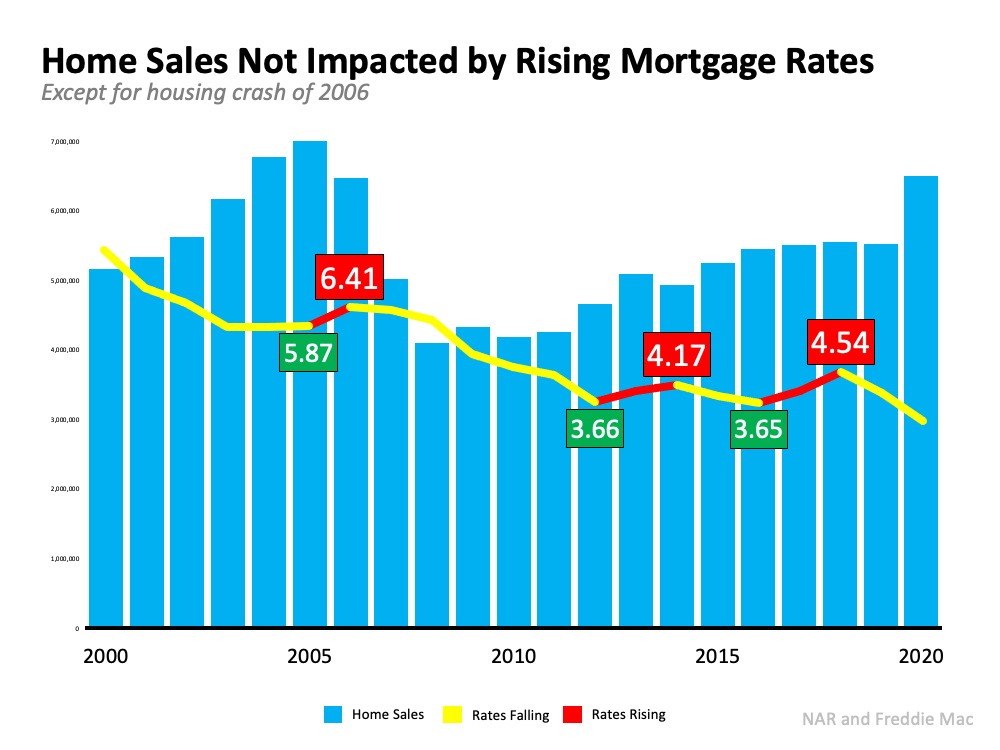

Existing-home sales rose in November, denoting three consecutive months of increases, according to the National Association of Realtors®. Three of the four major U.S. regions reported growth in monthly sales, while the fourth region held steady in November. From a year-over-year perspective, only one region experienced a rise in sales as the three others saw home sales decline.

Total existing-home sales (transactions that include single-family homes, townhomes, condominiums and co-ops) grew 1.9% from October to a seasonally adjusted annual rate of 6.46 million in November. Sales fell 2.0% from a year ago (6.59 million in November 2020).

Total housing inventory at the end of November amounted to 1.11 million units, down 9.8% from October and down 13.3% from one year ago (1.28 million). Unsold inventory sits at a 2.1-month supply at the current sales pace, a decline from both the prior month and from one year ago.

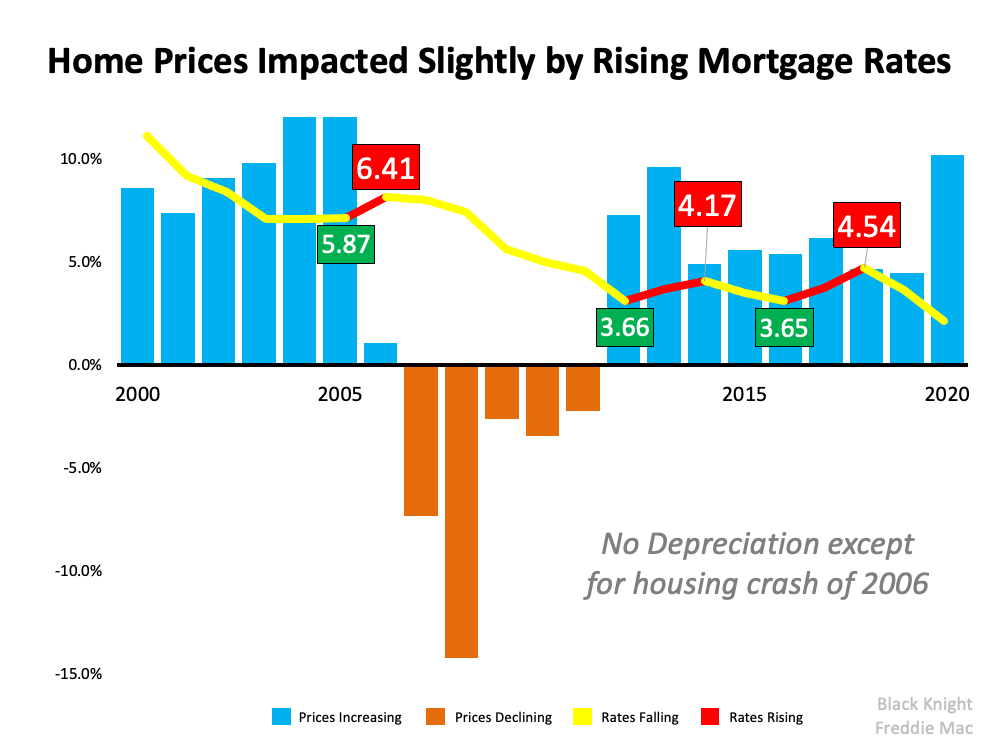

The median existing-home price for all housing types in November was $353,900, up 13.9% from November 2020 ($310,800), as prices increased in each region, with the highest pace of appreciation in the South region. This marks 117 straight months of year-over-year increases, the longest-running streak on record.

Properties typically remained on the market for 18 days in November, equal to October and down from 21 days in November 2020. Eighty-three percent of homes sold in November 2021 were on the market for less than a month.

In October, first-time buyers were responsible for 26% of sales in November, down from 29% in October and from 32% in November 2020. NAR's 2021 Profile of Home Buyers and Sellers – released earlier this month – reported that the annual share of first-time buyers was 34%.

Investing in Real Estate

Today's low interest rates and rising home prices have created some great investment opportunities!

Today's low interest rates and rising home prices have created some great investment opportunities!

Investing in real estate has unique advantages over other types of investments. Let's take a look at some of the reasons why real estate investment should be on the "short list" for many investors:

- Interest in mortgage loans are tax-deductible. Investors can lower their tax liability while increasing their equity.

- Renters pay down your mortgage loan. Investors reap the benefits of rental income, which offsets your mortgage cost and build equity.

- Real Estate values increase over the long term. Real Estate is limited and will always be in demand.

- 1031 exchanges are available to defer taxable income when you are ready to sell.

Many investors are taking advantage of these great market conditions. Have questions? Give us a call. We are happy to help!

Are bi-weekly payments right for you?

Many people ask about bi-weekly payment plans designed to reduce the interest paid out over the course of your loan. These programs help the borrower budget an extra payment a year, and over time this can knock years off the repayment schedule.

Many people ask about bi-weekly payment plans designed to reduce the interest paid out over the course of your loan. These programs help the borrower budget an extra payment a year, and over time this can knock years off the repayment schedule.

Many people are surprised to learn that they can do this themselves without any special programs, simply by submitting an extra principal payment as they are able. By submitting an extra payment, you get the advantages of an early payout, without the extra contractual obligation. Want more information on other mortgage options?

Contact us today for our list of preferred local mortgage experts who can help you position yourself for a great year in 2020!

It's Now Much Easier to Buy A Home

Why It Just Became Much Easier To Buy a Home

Since the pandemic began, Americans have reevaluated the meaning of the word home. That’s led some renters to realize the many benefits of homeownership, including the feelings of security and stability and the financial benefits that come with rising home equity. At the same time, many current homeowners have decided their house no longer meets their needs, so they moved into homes with more space inside and out, including a home office for remote work.

However, not every purchaser has been able to fulfill their desire for a new home. Here are two obstacles some homebuyers are facing:

- The ability to save for a down payment

- The ability to qualify for a mortgage at the current lending standards

This past week, both of those challenges have been mitigated to some degree for many purchasers. The FHFA (which handles mortgages by Freddie Mac, Fannie Mae, and the Federal Housing Administration) is raising its loan limit for prospective purchasers in 2022. The term used to describe the maximum loan amount they will entertain is the Conforming Loan Limit.

What Is the Difference Between a Conforming Loan and a Non-Conforming Loan?

Investopedia explains the difference in a recent post:

“Conforming loans are the only loans that meet the requirements to be acquired by Fannie Mae and Freddie Mac. Jumbo loans, which exceed the conforming limit, are the most common type of nonconforming loan.”

What Difference Does It Make to Me as a Home Buyer?

A Forbes article earlier this year explains the benefits of a conforming loan and why they exist:

“Since lenders can’t sell non-conforming loans to Fannie Mae or Freddie Mac to free up their cash, they’re a bit riskier for the lender. This is especially true for jumbo loans, which aren’t backed by any government guarantees. If you default on a jumbo loan, it’s a huge blow to the lender.

Thus, lenders generally charge higher interest rates to compensate, and they can have even more requirements. For example, lenders who give out jumbo loans often require that you make a down payment of at least 20% and show that you have at least six months’ worth of cash in reserve, if not more.”

What Happened Last Week?

The FHFA has significantly increased its Conforming Loan Limits for 2022. Sandra L. Thompson, FHFA Acting Director, explains in the press release that:

“Compared to previous years, the 2022 Conforming Loan Limits represent a significant increase due to the historic house price appreciation over the last year. While 95 percent of U.S. counties will be subject to the new baseline limit of $647,200, approximately 100 counties will have conforming loan limits approaching $1 million.”

This means that more homes now qualify for a conforming loan with lower down payment requirements and easier lending standards – the two challenges holding many buyers back over the last year.

The Federal Housing Administration (FHA) also increased its Conforming Loan Limits for 2022. That could also mean an easier path to homeownership for many prospective buyers. As the Forbes article explains:

“FHA loans can be very beneficial if you don’t have as much savings, or if your credit score could use some work.”

Bottom Line

Buying your first or your next home may have just gotten much easier (less stringent qualifying standards) and less expensive (possibly lower mortgage rate). Let’s connect to discuss how these changes may impact you.

![2022 Housing Market Forecast [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/12/15133953/20211217-MEM-1046x2117.png)